Proposals to introduce a new Risk Mitigation Accounting (RMA) model in IFRS 9 Financial Instruments aim to better align the financial statements with risk management activities. The RMA model would allow entities that apply a holistic and dynamic approach in managing their interest rate repricing risk to:

- better reflect dynamic risk management activities that arise from an open portfolio of changing assets and liabilities in the financial statements; and

- reduce operational complexities with the current macro hedge accounting requirements.

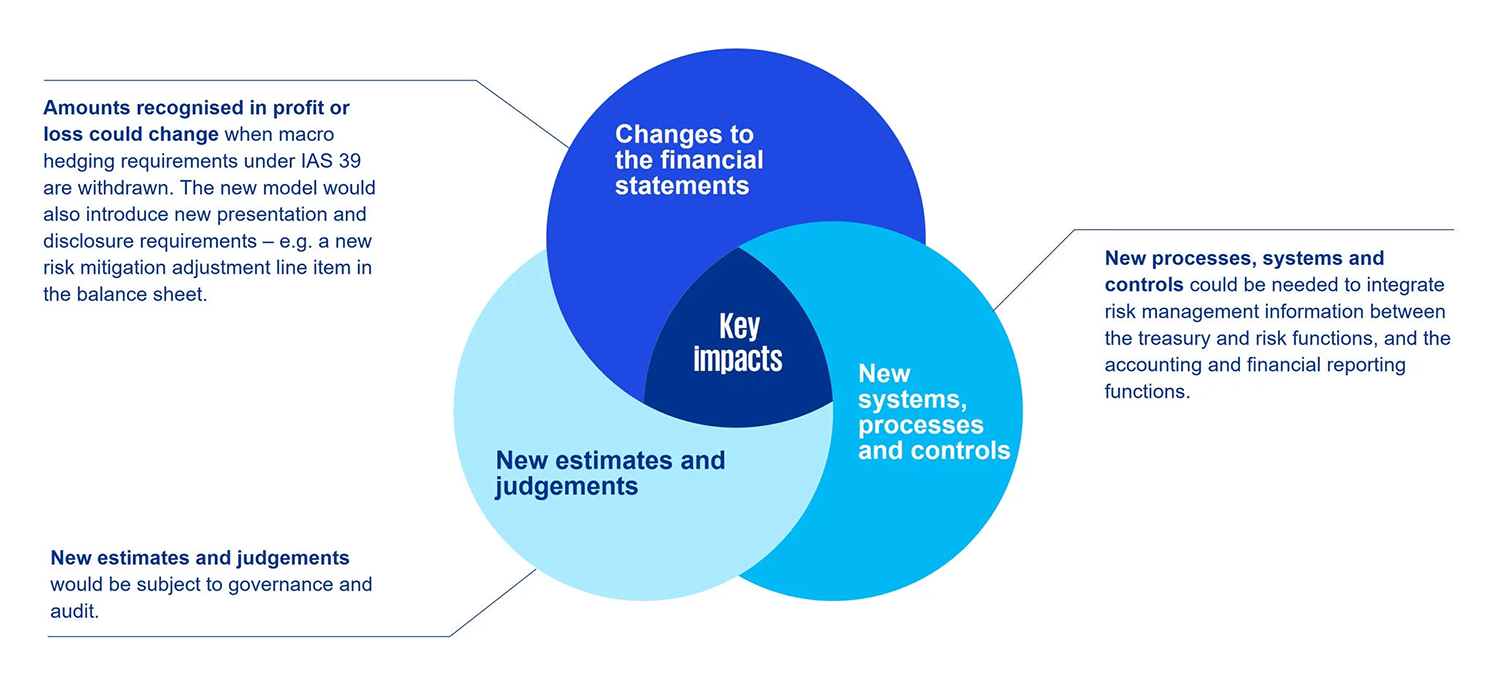

This would be a significant change for banks and insurers that manage their exposure to repricing risk that arises from financial assets and financial liabilities that change continually.

The new model1 would be optional. However, entities would no longer be able to hedge account under IAS 39 Financial Instruments: Recognition and Measurement, because these requirements would be withdrawn once the proposals are finalised. Instead, entities could apply the RMA model and/or the general hedge accounting requirements under IFRS 9 or cease hedge accounting altogether.