Amendments to the Tax and Social Security Procedure Code (TSSPC), which introduce the mandatory SAF-T reporting in Bulgaria were promulgated in the special issue 26 of the State Gazette of 27 March 2025.

Basic requirements

Standard audit file for tax purposes

The Standard Audit File for Tax Purposes (SAF-T report) is an international standard for the submission of accounting data in a uniform format by taxpayers to the revenue administration, developed by the Organization for Economic Co-operation and Development (OECD).

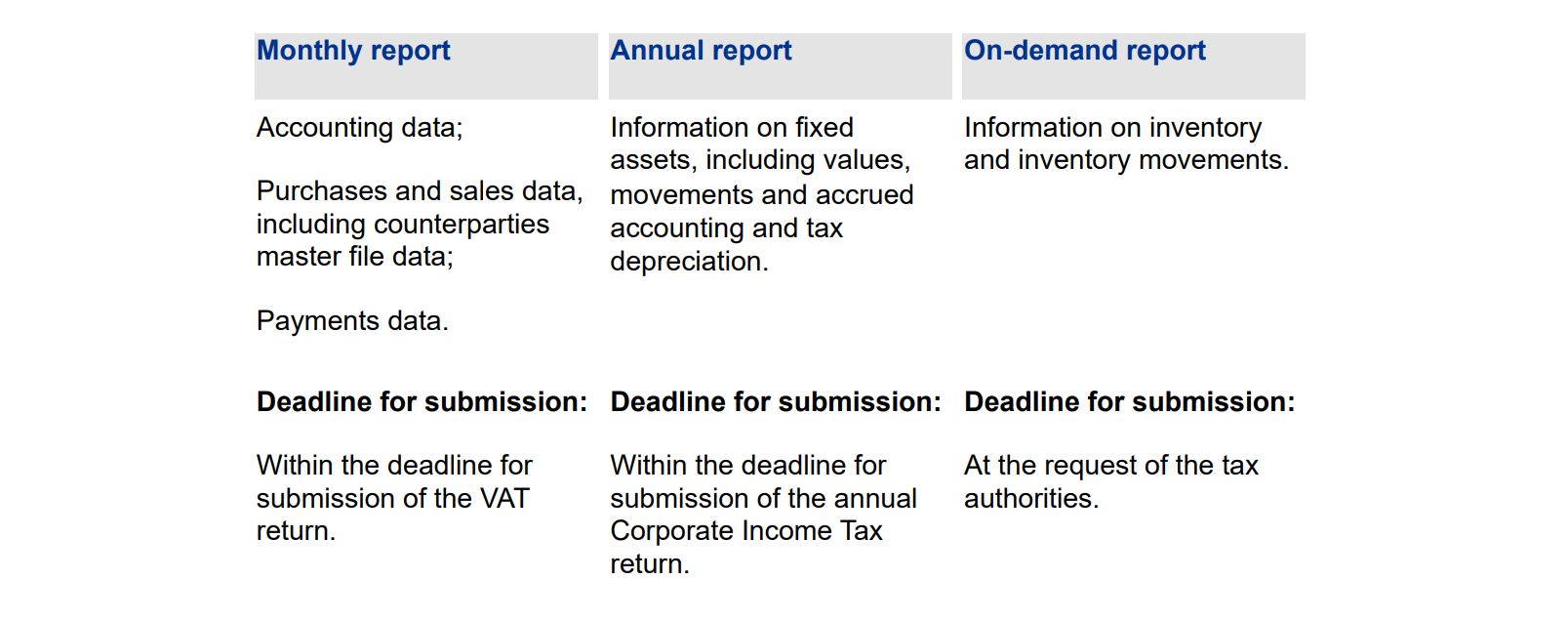

The Bulgarian SAF-T report will contain business and accounting data, which should be submitted in a standardized format on a monthly basis, annual basis or upon request as follows:

Phased introduction of mandatory SAF-T filings

The obligation to submit SAF-T reports is introduced in stages over a five-year period. The first stage will affect the largest enterprises for which reporting becomes mandatory as early as 2026:

- First reporting period January 2026;

- Deadline for submission of the monthly SAF-T report for January 2026 – 14 February 2026;

- Deadline for submission of the annual SAF-T report for 2026 – 30 June 2027.

The process will be completed in 2030 with the onboarding of micro-enterprises registered under the VAT Act.

The criteria which determine when SAF-T becomes mandatory for a given taxpayer are twofold and cumulative: (1) the classification of the entity as per the Accounting Act – large, medium, small or micro-enterprise and (2) some specific criteria regarding the business activity’s volume provided for in the TSSPC.

The first wave will include companies which as of 31 December 2023 (1) fall into the category of "large enterprise" within the meaning of the Accounting Act and at the same time (2) have net sales revenues of more than BGN 300,000,000 or have paid taxes and social security contributions of more than BGN 3,500,000.

Corrections in submitted reports and penalties

Companies will be allowed to make corrections in already submitted SAF-T reports only if these relate to the first six reporting periods (months).

Failure to submit a SAF-T report on time will be subject to an administrative sanction in the range of BGN 5,000 - BGN 15,000. In cases of repeated violation, the amount will be doubled, i.e. BGN 10,000 - BGN 30,000.

Additional information

The obligation to submit a SAF-T report is introduced with the amendments to the TSSPC adopted with the State Budget Act for 2025. In addition, an order of the Executive Director of the NRA should be published, which would regulate the new report’s format and submission procedure. The nomenclatures for standardizing the reportable information, as well as the related validation rules will also be provided for in the expected order.

KPMG’s Assistance

KPMG has a solution for assistance at every stage of the SAF-T implementation process:

- Data mapping – comparing and mapping the data available in the entity’s IT system against the legal requirements.

- Coding of algorithms for extracting data from the company's IT system and converting them into the legally prescribed format.

- A technological solution for generating a valid SAF-T report, developed and maintained by KPMG.

- Outsourced SAF-T compliance, where the obligation to prepare, sign and submit SAF-T reports is assigned to KPMG.

Contact us for more information and request an offer for assistance which will be tailored according to your needs.

For information

Ivan Vargoulev

Associate Partner, Tax

Tel: +359 (2) 9697 700

Antoaneta Krasteva

Senior Manager, Tax

Tel: +359 (2) 9697 700