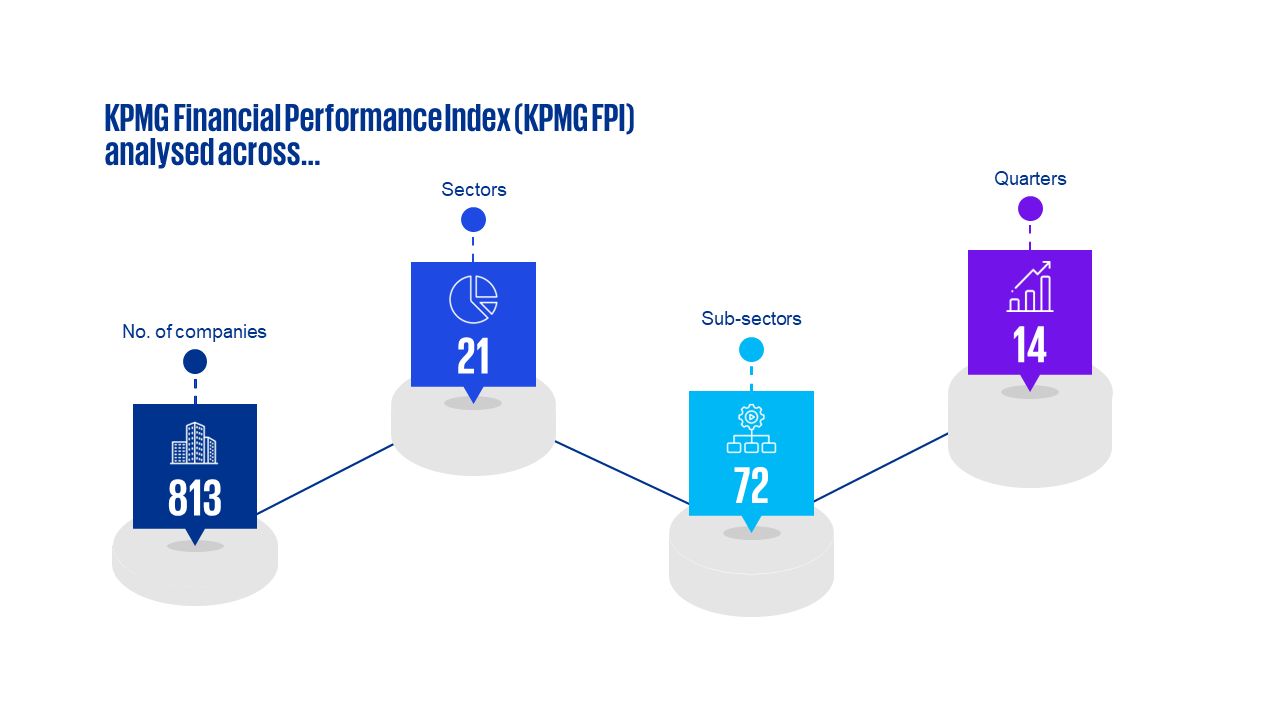

An indicator of corporate health for companies across the Indonesian economy

We are pleased to share with you the third edition of our quarterly KPMG Financial Performance Index (FPI) publication. We provide our insights into the changing state of corporate health across all Indonesian markets and sectors, following the end of the reporting season for the three months to September 2023. KPMG FPI data is refreshed on a quarterly basis. For more information, visit the KPMG FPI page.

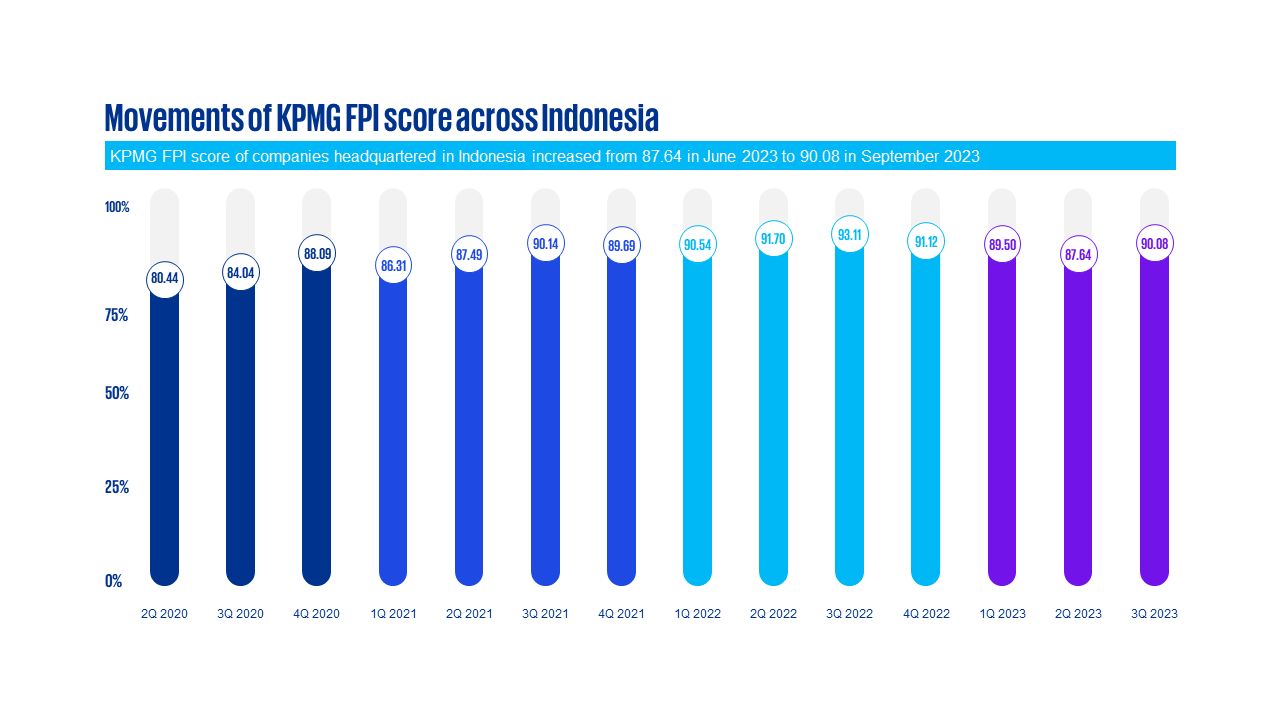

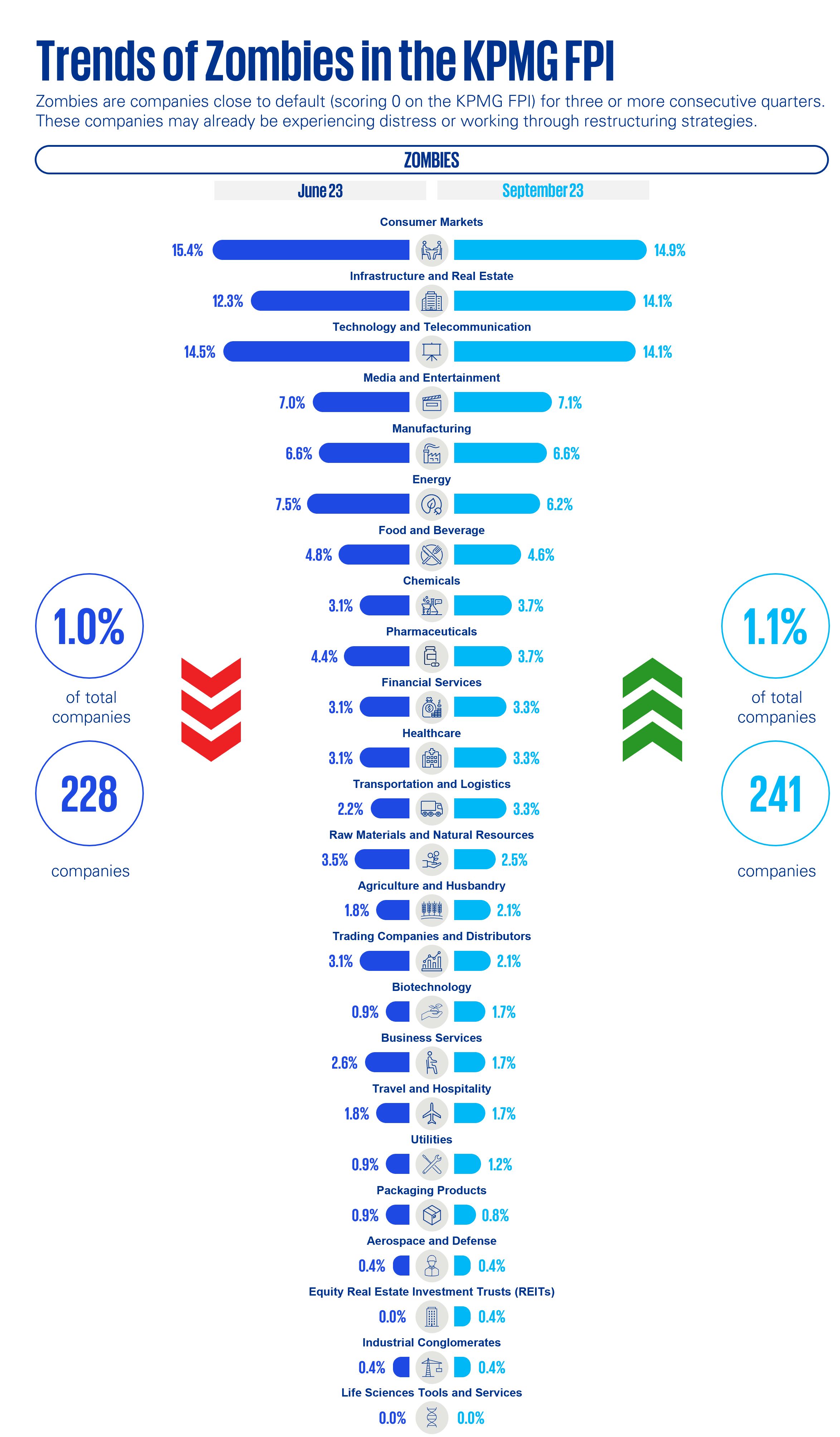

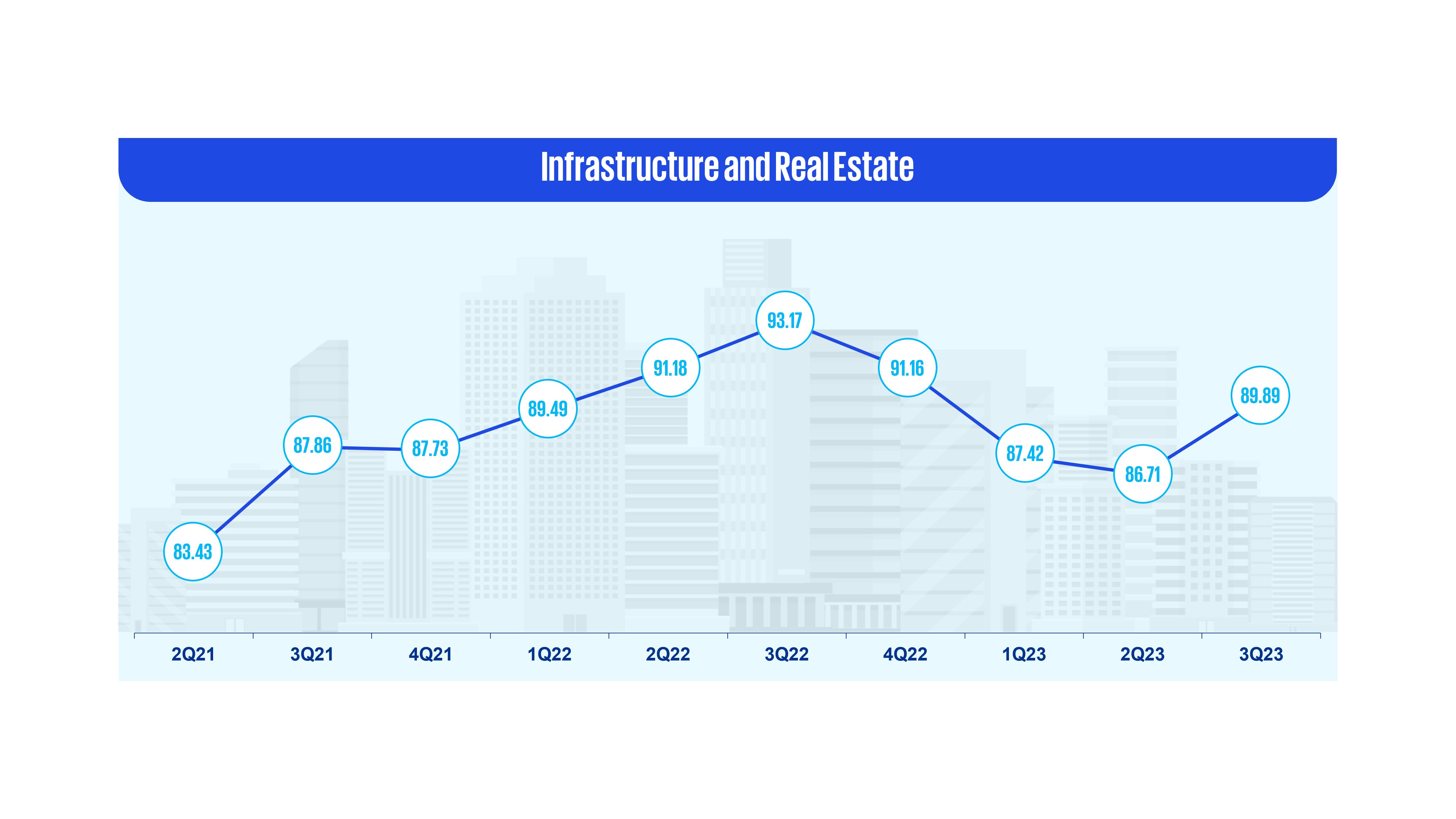

Between June 2023 and September 2023, we observed an increase in the Indonesian KPMG FPI from 87.93 to 90.08. This denotes an increase in the financial corporate health of companies headquartered in Indonesia, including an increase in FPI scores in all 18 sectors analyzed. However, we note that the number of Zombie companies are also up overall, driven primarily by infrastructure and real estate.

Key highlights:

- After its post-Covid growth to 93 in the third quarter (Q3) of 2022, the Indonesian aggregate corporate FPI score had steadily declined to 88 at the end of the second quarter (Q2) of 2023.

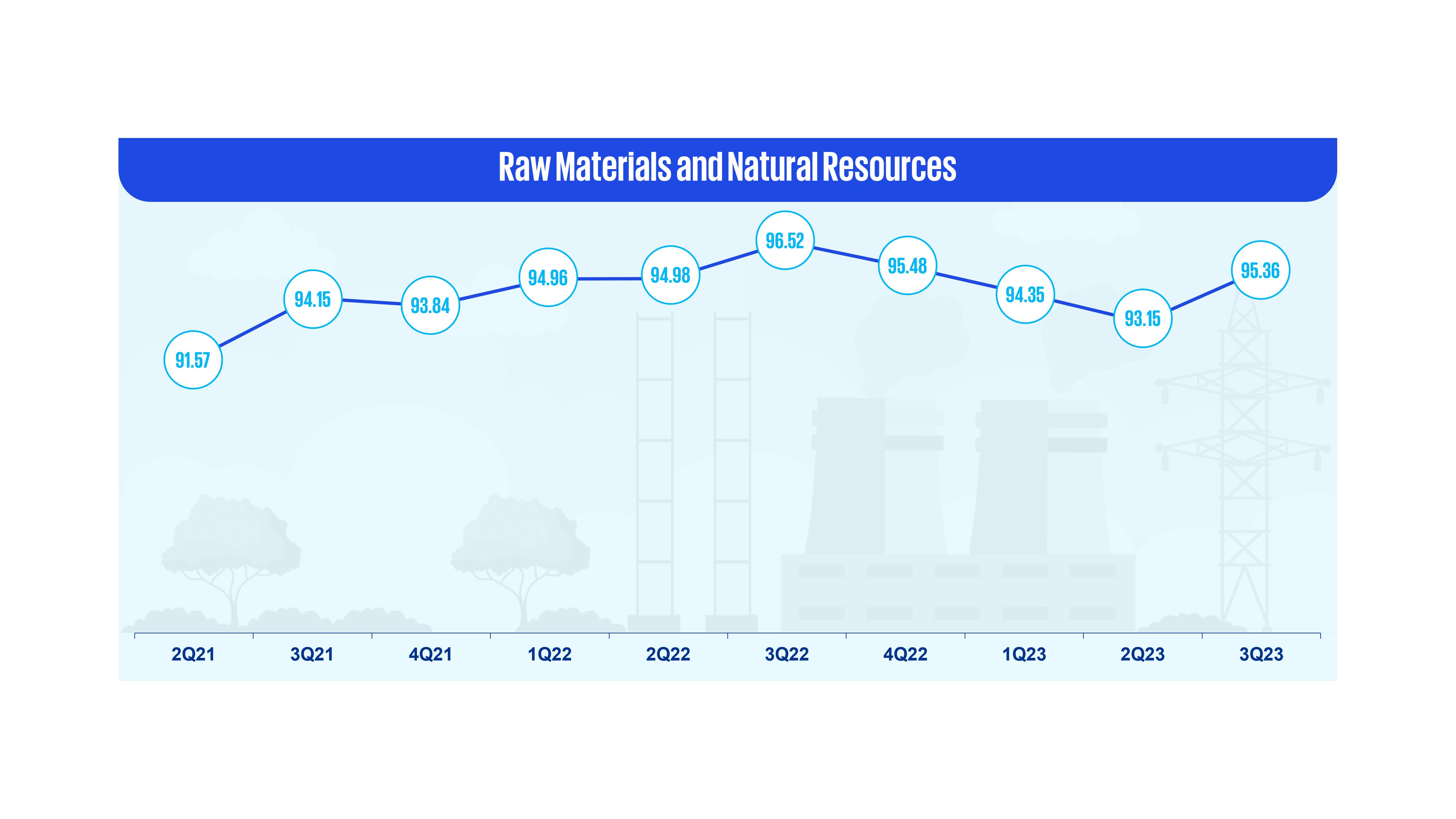

- However, it has bounced back to 90 in Q3 2023. This is mainly driven by overall improvement in the economy, as seen by the overall higher FPI scores across all sectors compared to Q2 2023.

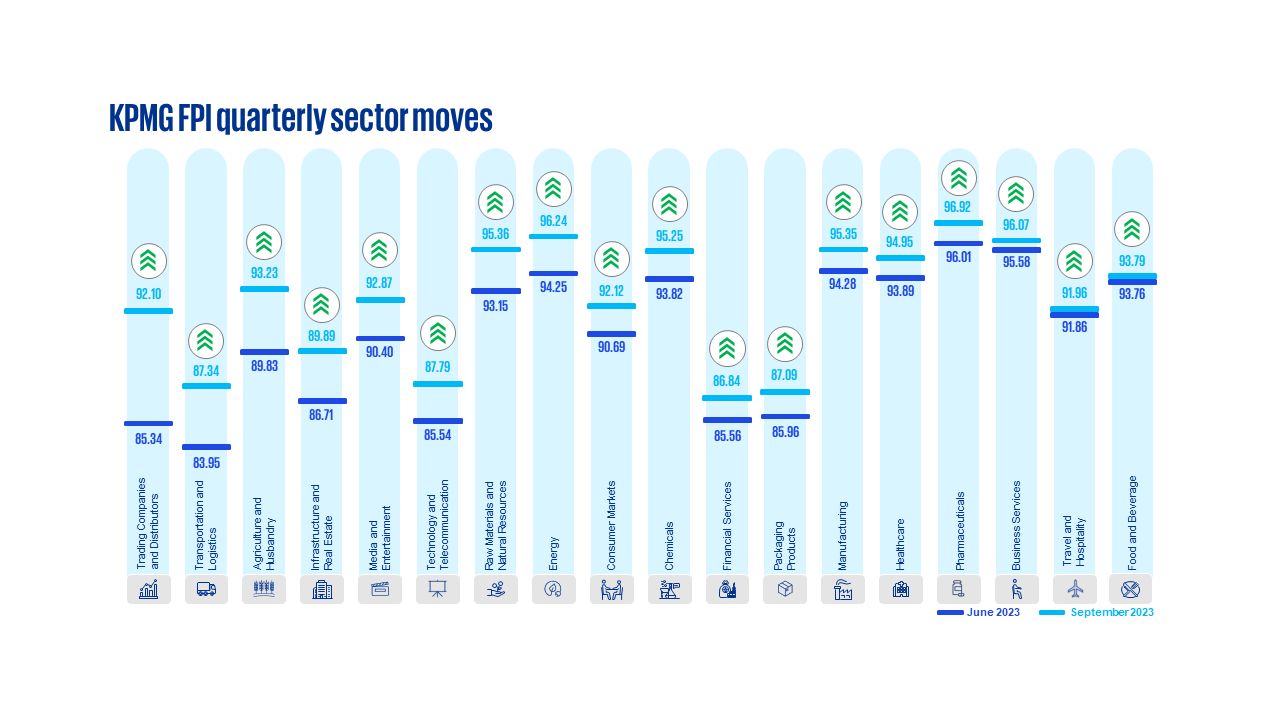

Sector movers:

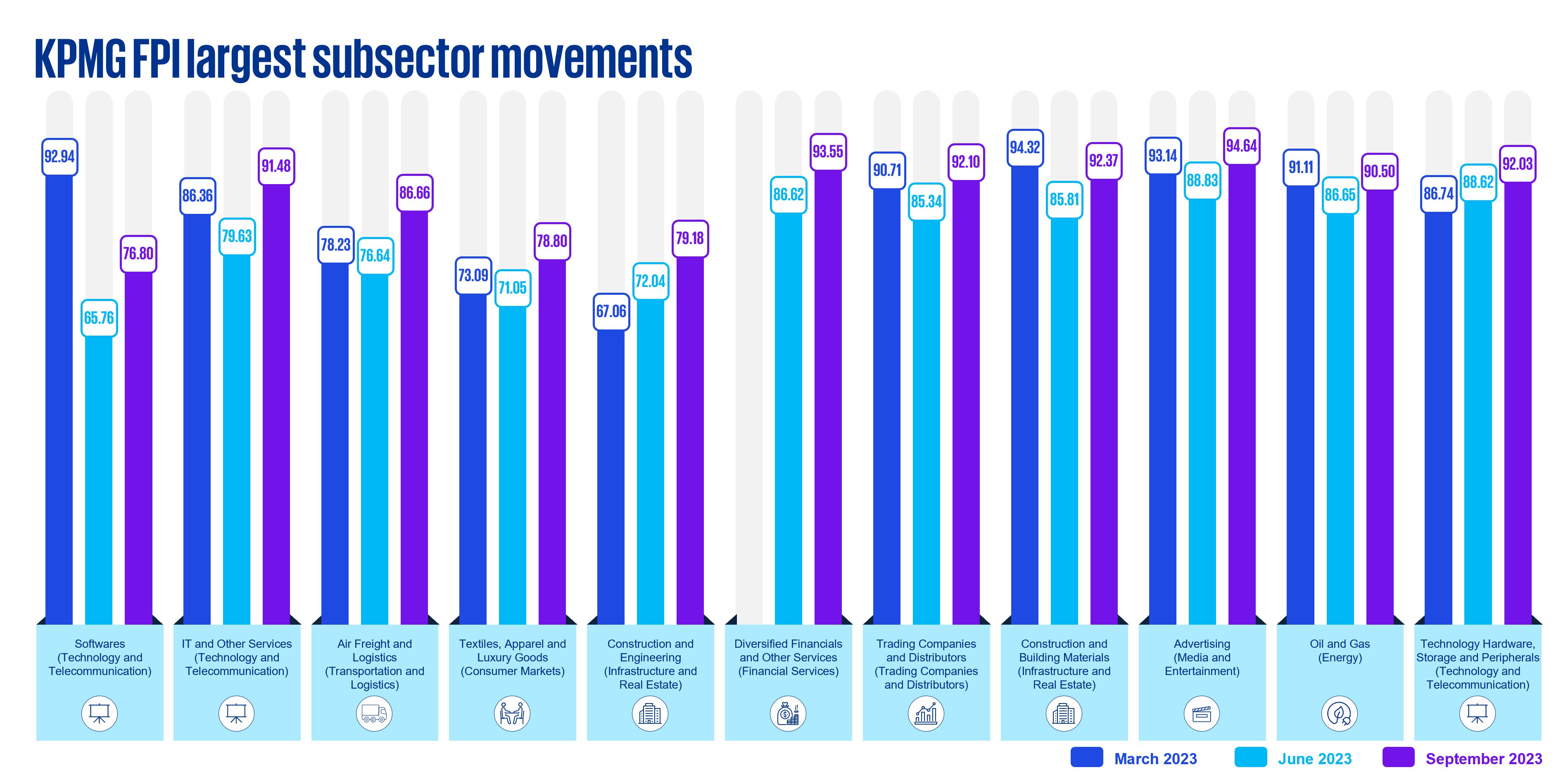

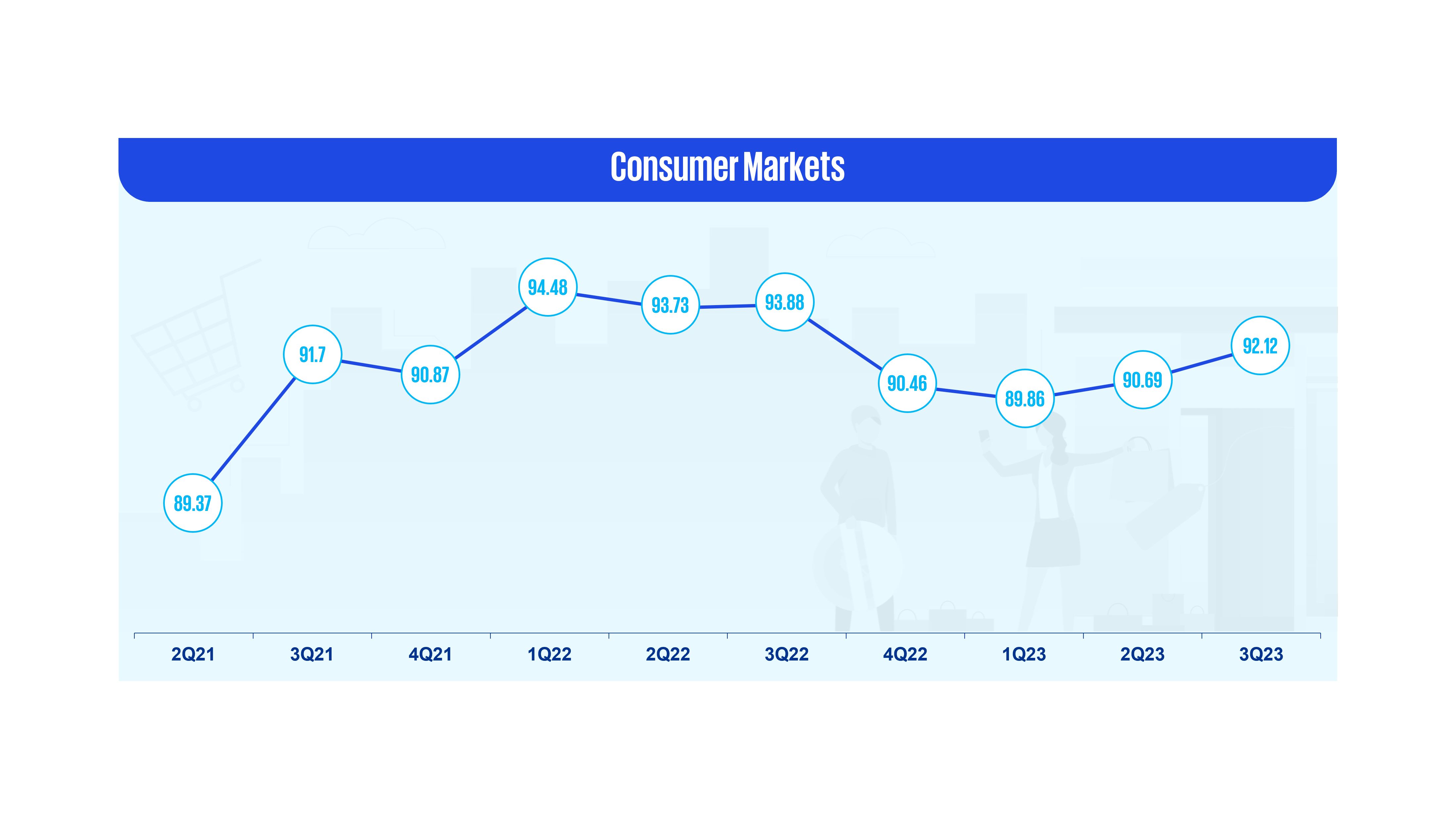

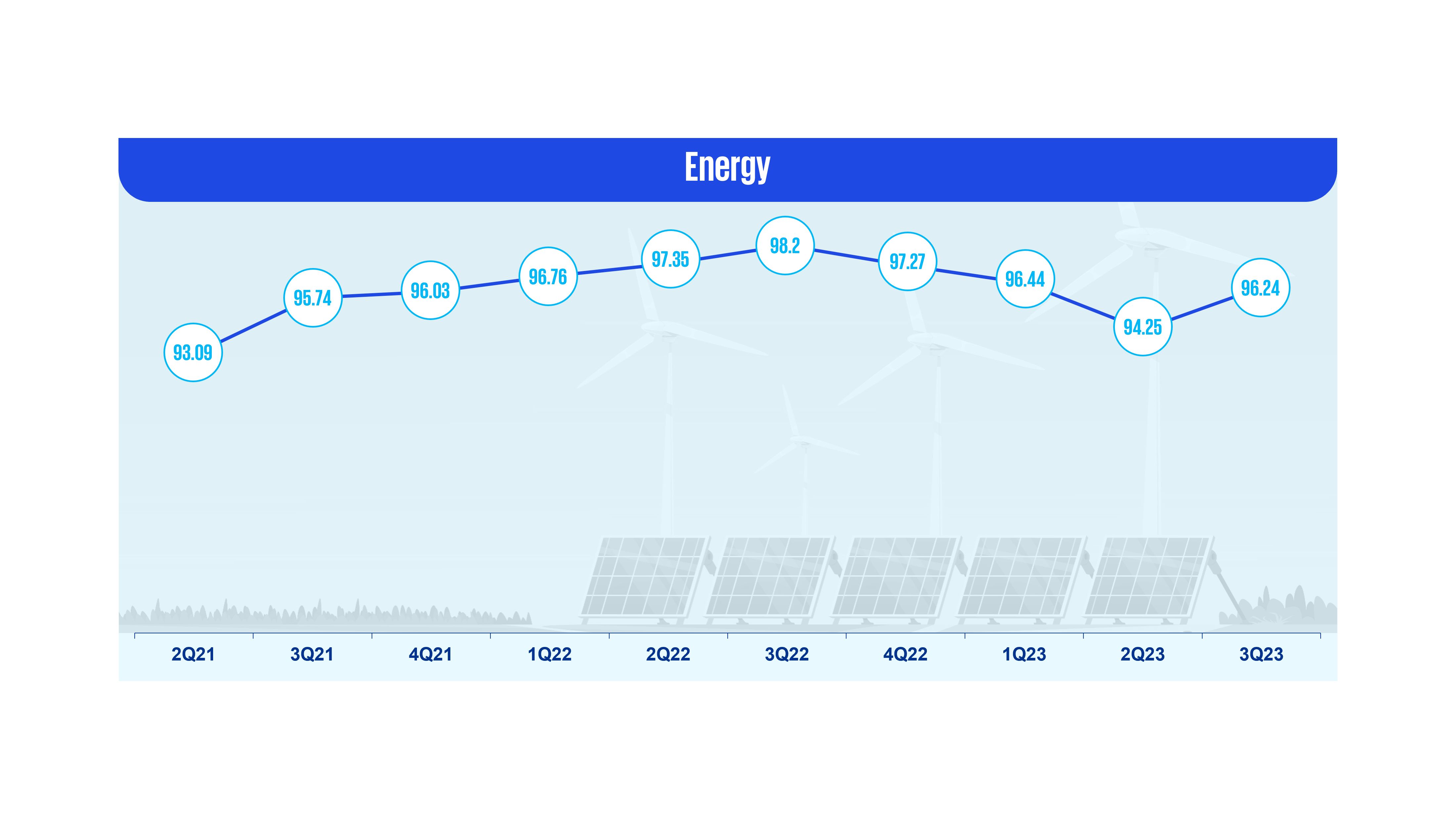

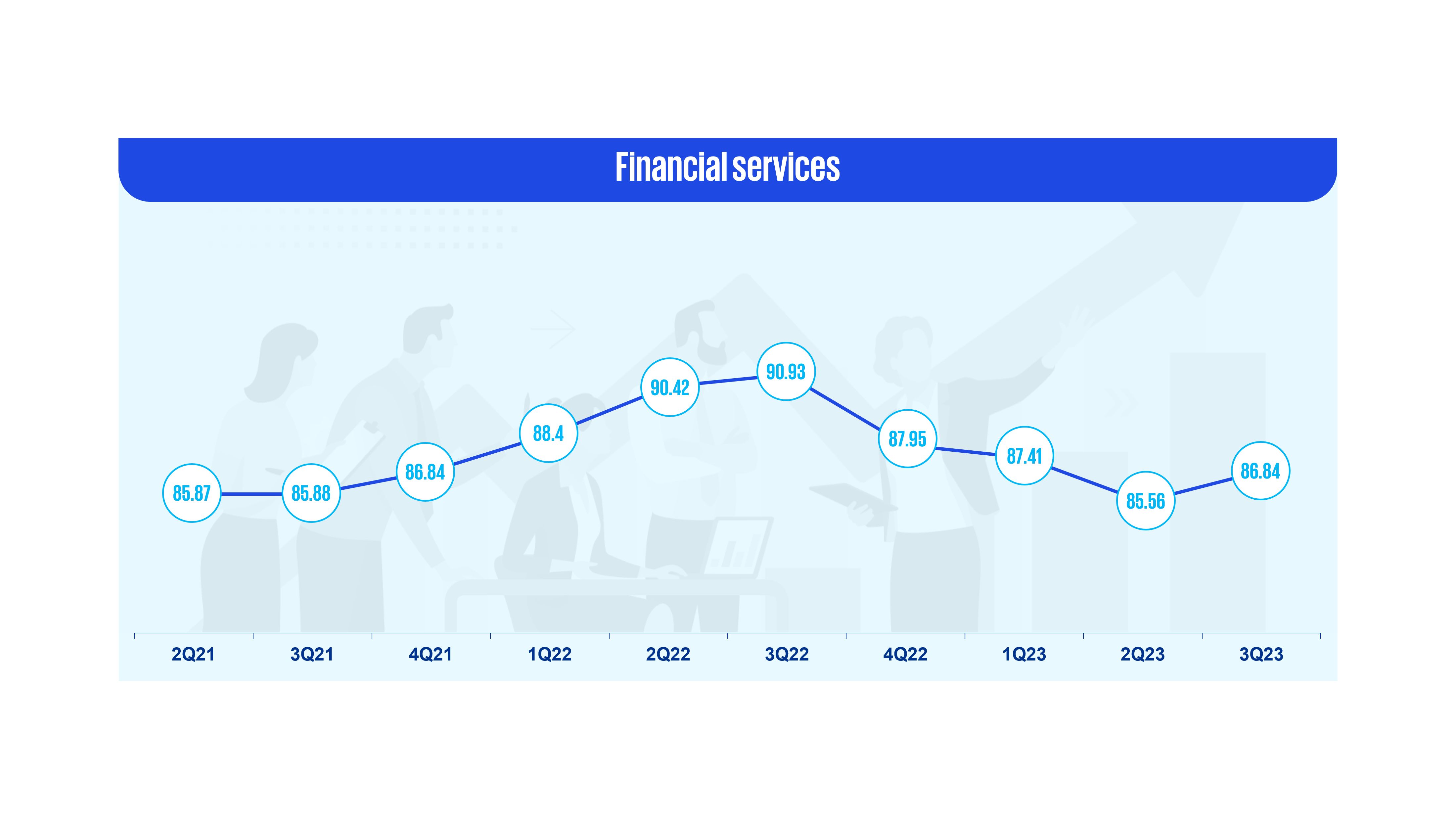

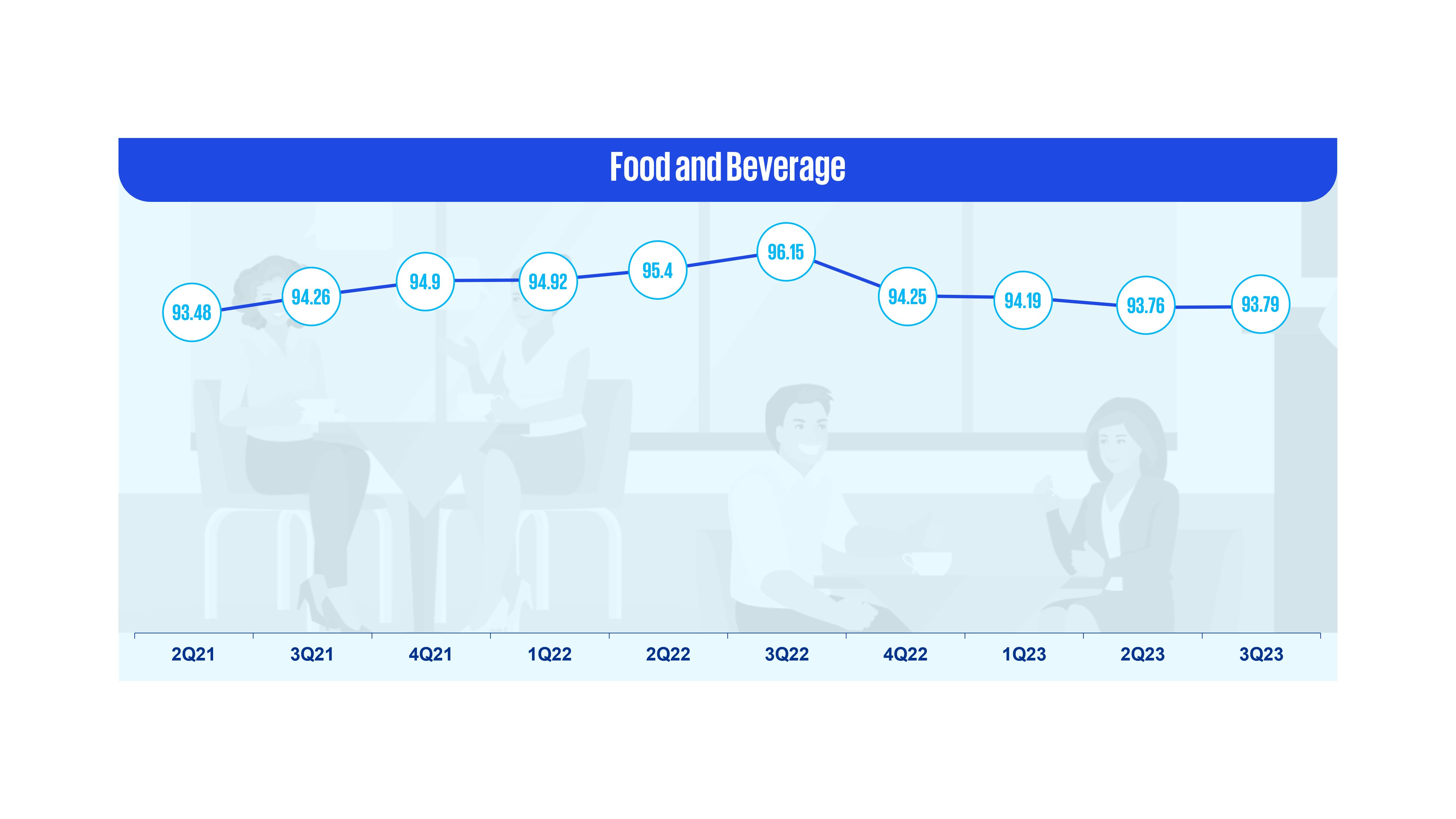

- The overall higher FPI score compared to the previous quarter is also reflected in individual sector scores, as all sectors scored higher compared to Q2 2023.

- Pharmaceuticals, energy, and business services were the best performing sectors in Q3 2023.

- Trading companies and distributors improved the most, mainly driven by increasing household consumption and investment.

- Financial services, packaging products and transportation and logistics were the worst performing FPI sector scores in Q3 2023, all of which ended with FPI scores of 87.

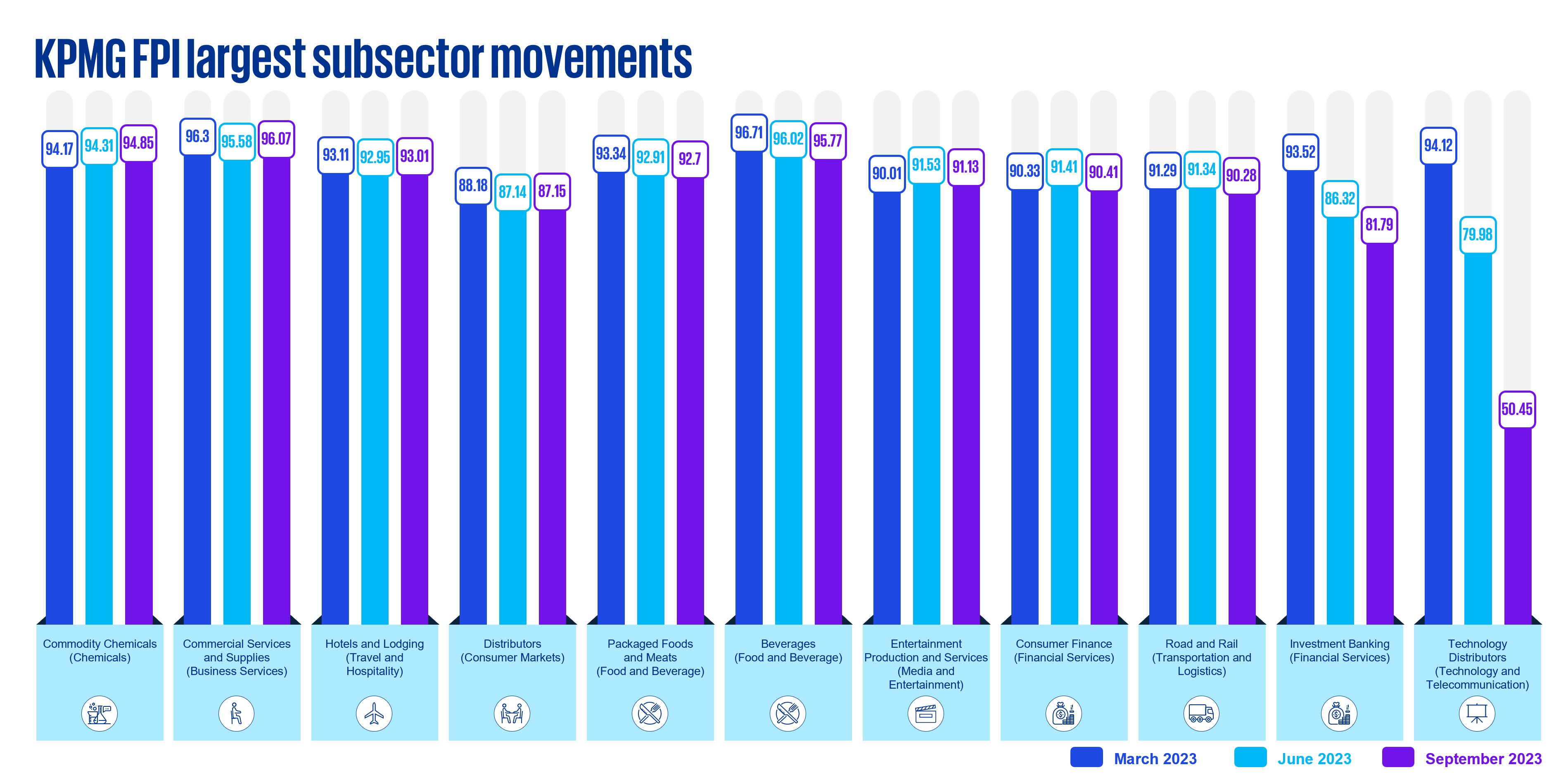

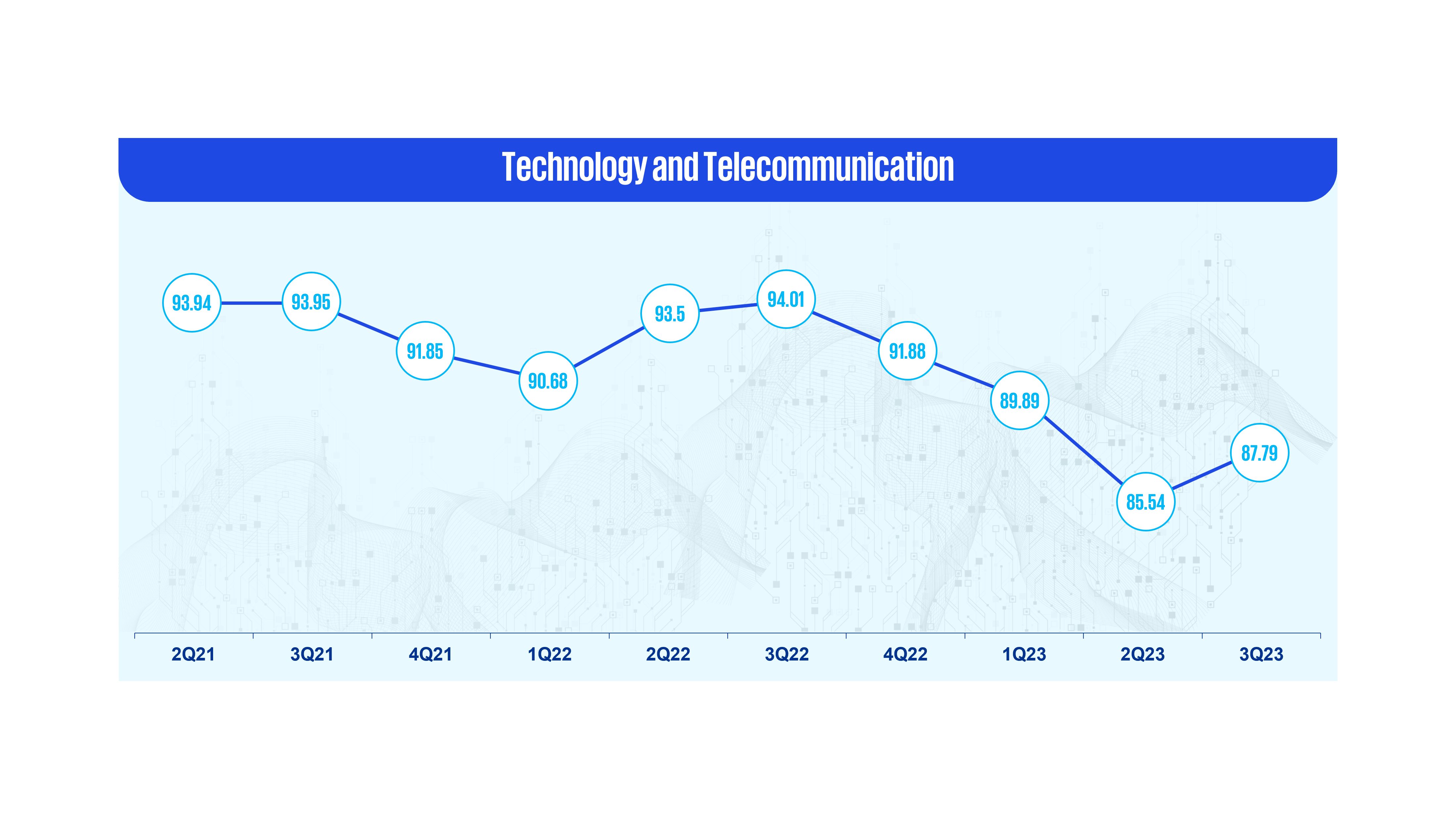

- Amongst sub-sectors, technology distributors (included in the technology and telecommunication sector) was the worst hit, as its score had decreased by 37 percent.

- Investment banking, driven by lower deal volumes, also saw significant decreases in third quarter of the year, continuing the trend observed in the first half of the year.

Indonesian economy:

- Of the nine largest sectors by market cap, all had a FPI score greater than 90, except for technology and telecommunications (88) and financial services (87).

- The Indonesian economy is expected to slow down ahead of the February 2024 elections, primarily as a result of decreasing investment, with rising interest rates and a falling Rupiah contributing to an expected slow-down.

- This slowdown is expected to be temporary, with growth in 2024 expected to continue to be strong after the elections, which will provide greater certainty on the future of Indonesia’s economy.

- In October, Bank Indonesia (BI) raised its benchmark rate (BI 7-day (Reverse) Repo Rate) 25 basis points to 6 percent, its highest since June 2019. The increase is expected to help the Indonesian government meet its target inflation rate of 3±1 percent. The higher rate is expected to help stabilize the Rupiah amid pressure driven by the Federal Reserve’s interest rates hikes and rising geopolitical risks.

KPMG FPI largest subsectors movements

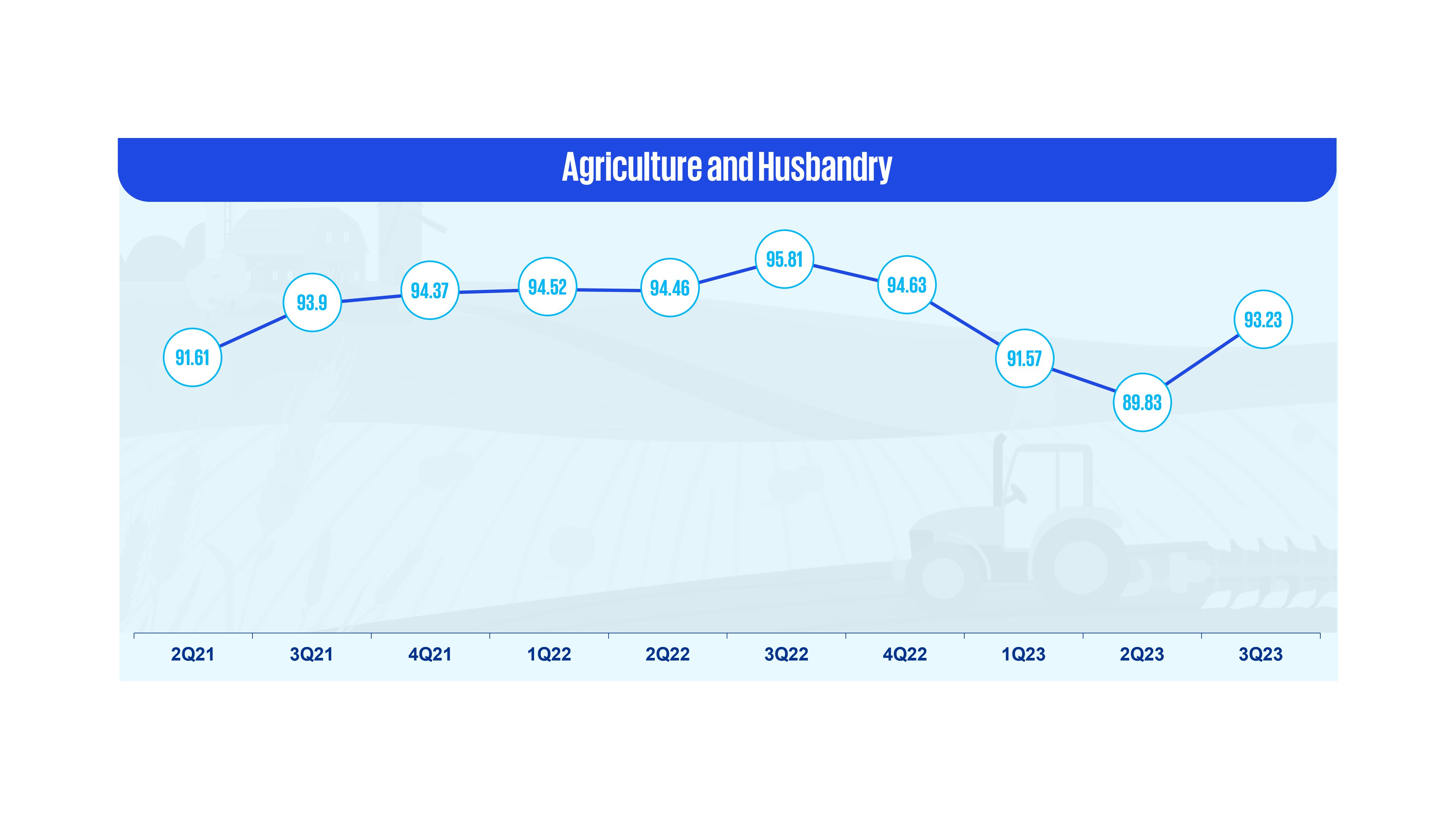

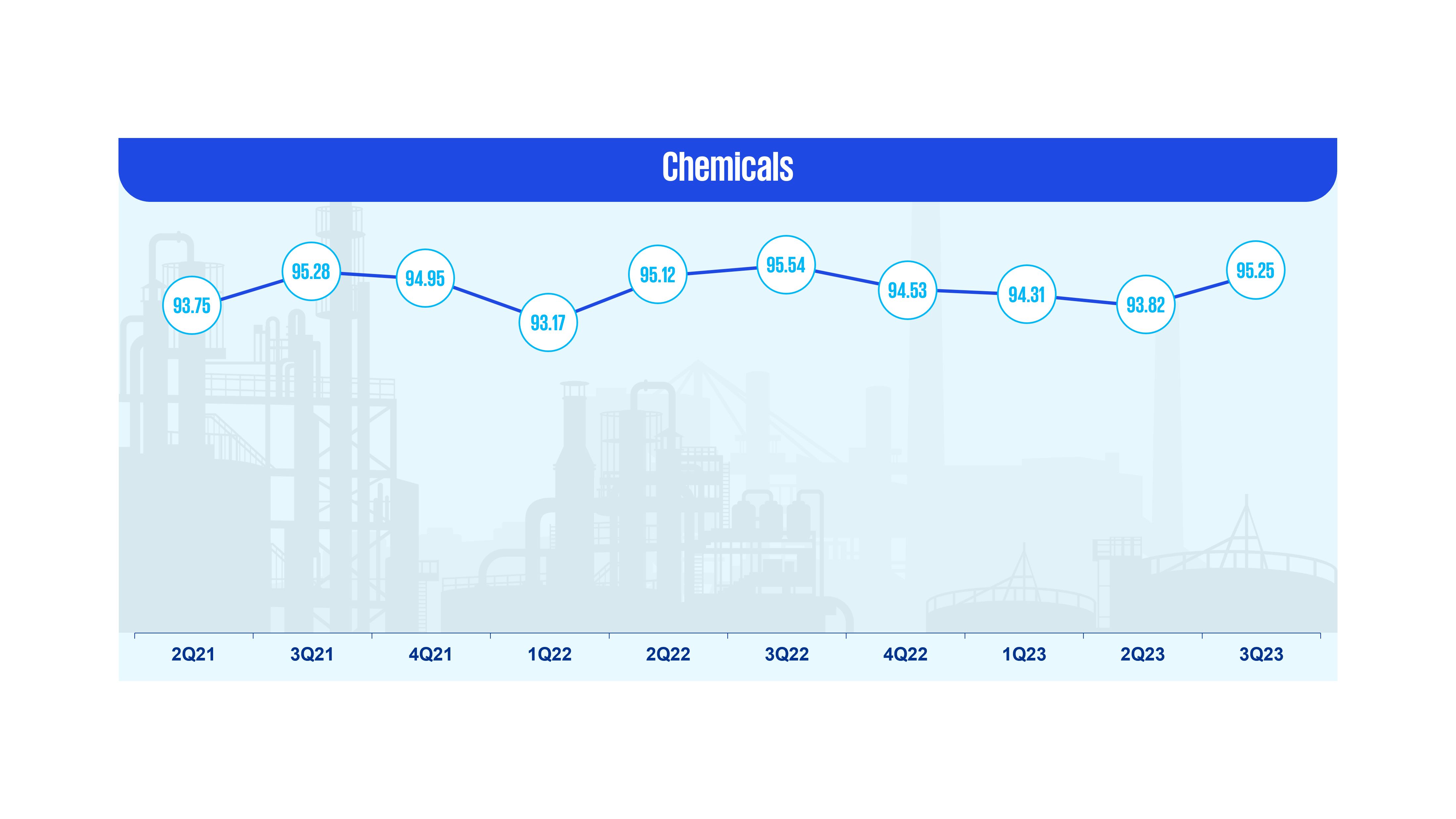

KPMG FPI trends across key industries for the Indonesian economy

About KPMG FPI:

The KPMG FPI is a metric used to measure a company’s financial health by its ‘probability to default’. The analysis has been prepared using John Y. Campbell, Jens Hilscher, and Jan Szilagyi’s probability to default formula which takes into account financial information and market data. The KPMG FPI score ranges from 0 - 100. The lower the KPMG FPI score, the more likely a company is to default. In contrast, the higher the score, the less likely it is to default. In this analysis, released every three months, we analyze the KPMG FPI score movements of publicly listed companies in Indonesia (following the reporting season of full year and half year results) to draw insights into corporate health across the Indonesian economy.

KPMG FPI combines both market and financial information to determine a company’s relative financial distress levels. KPMG believes that combining the two types of information detects deteriorating corporate health more effectively than either source alone.

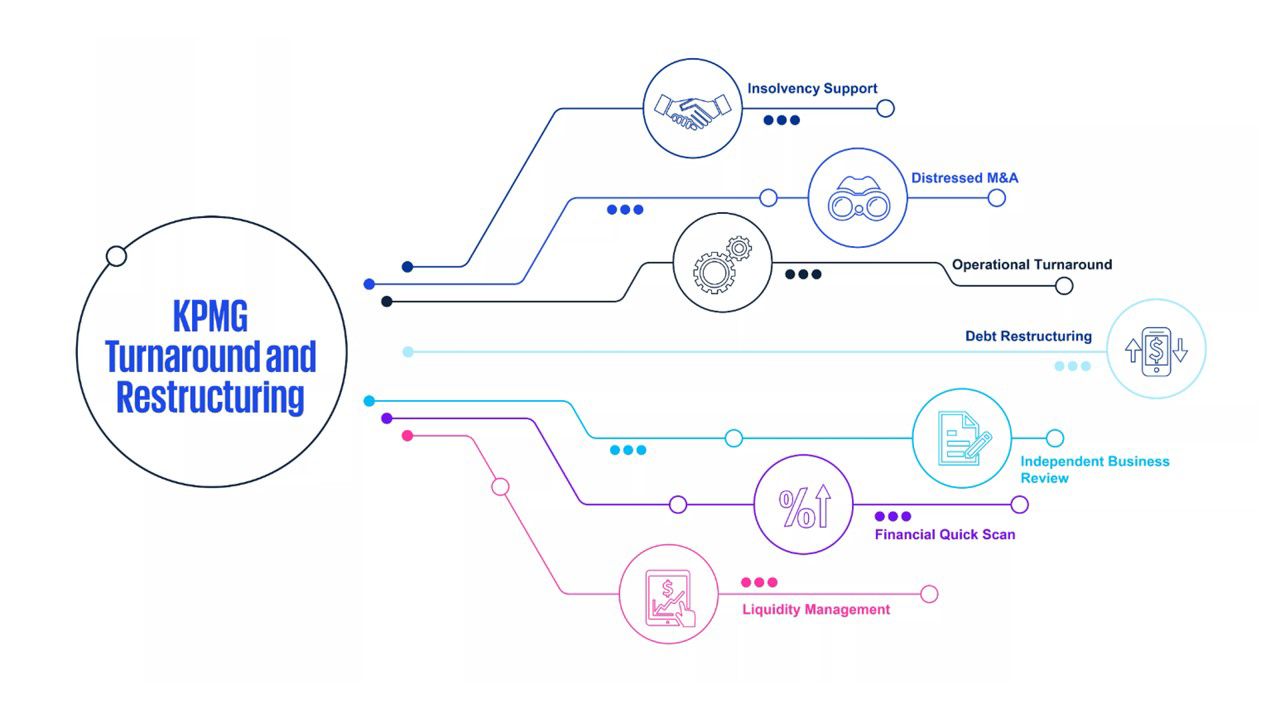

How can we help?

The information contained in this document is of a general nature and is not intended to address the objectives, financial situation or needs of any particular individual or entity. It is provided for information purposes only and does not constitute, nor should it be regarded in any manner whatsoever, as advice and is not intended to influence a person in making a decision, including, if applicable, in relation to any financial product or an interest in a financial product. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation. To the extent permissible by law, KPMG and its associated entities shall not be liable for any errors, omissions, defects or misrepresentations in the information or for any loss or damage suffered by persons who use or rely on such information (including for reasons of negligence, negligent misstatement or otherwise).