Capital Gains Tax (CGT) Prakas

(Prakas No. 496 MEF. PrK, dated 18 July 2025)

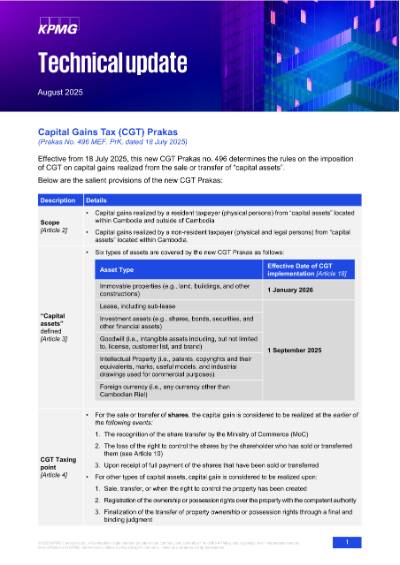

Effective from 18 July 2025, this new CGT Prakas no. 496 determines the rules on the imposition of CGT on capital gains realized from the sale or transfer of “capital assets”.

Below are the salient provisions of the new CGT Prakas:

| Description | Details | |

| Scope [Article 2] | •Capital gains realized by a resident taxpayer (physical persons) from “capital assets” located within Cambodia and outside of Cambodia •Capital gains realized by a non-resident taxpayer (physical and legal persons) from “capital assets” located within Cambodia. |

|

“Capital assets” defined [Article 3] |

•Six types of assets are covered by the new CGT Prakas as follows: | |

| Asset Type | Effective Date of CGT implementation [Article 18] | |

| Immovable properties (e.g., land, buildings, and other constructions) | 1 January 2026 | |

| Lease, including sub-lease |

1 September 2025 |

|

| Investment assets (e.g., shares, bonds, securities, and other financial assets) | ||

| Goodwill (i.e., intangible assets including, but not limited to, license, customer list, and brand) | ||

| Intellectual Property (i.e., patents, copyrights and their equivalents, marks, useful models, and industrial drawings used for commercial purposes) | ||

| Foreign currency (i.e., any currency other than Cambodian Riel) | ||

| CGT Taxing point [Article 4] | •For the sale or transfer of shares, the capital gain is considered to be realized at the earlier of the following events: 1.The recognition of the share transfer by the Ministry of Commerce (MoC) 2.The loss of the right to control the shares by the shareholder who has sold or transferred them (see Article 10) 3.Upon receipt of full payment of the shares that have been sold or transferred •For other types of capital assets, capital gain is considered to be realized upon: 1.Sale, transfer, or when the right to control the property has been created 2.Registration of the ownership or possession rights over the property with the competent authority 3.Finalization of the transfer of property ownership or possession rights through a final and binding judgment |

|

| Tax rate [Article 5] | •20% CGT is imposed on the capital gains (i.e., selling price less deductible expenses) | |

| Tax exemptions [Article 6] | •CGT shall not be imposed on the sale or transfer of: −Agricultural land, owned by citizens, and used actively for cultivating crops −“Primary” residence of the taxpayer, held for at least five years. Where the taxpayer (or their spouse) has more than one residence, only one residence shall be allowed as the “primary” residence −Immovable properties, through “succession”, within relatives (for the purpose of establishing common property) −Immovable properties, through first-time “donation”, within relatives (for the purpose of establishing common property) −Properties owned by the State and State institutions −Property owned by foreign diplomatic or consular missions, international organizations, or technical cooperation agencies of other governments −Properties used for public interest, in accordance with the Law on Expropriation •The issuance of new shares for the purpose of increasing the capital or injecting new investment into the company shall not be considered as the sale or transfer of shares. •In case of transfer of shares (wholly or partly) of an enterprise by a non-resident that has Retained Earnings (RE), the transaction shall be subject to CGT but will be exempted from the imposition of WHT on “deemed dividends”. •Realized capital gains, which are subject to CGT, shall be exempt from the WHT imposed on Cambodian-sourced income as stated in Article 33 of the Law on Taxation. |

|

| Deductible expenses[Article 7, 8,9, & 10] | •For immovable properties, the taxpayer is allowed to choose one of the two methods: a.Lump-sum deduction method: Eighty percent (80%) of the income received from the sale or transfer of the immovable property shall be allowed as a deduction. b.Actual deduction method: “Deductible expenses” actually incurred shall be allowed as a deduction, subject to the rules and criteria for claiming deductible expenses as per Articles 7, 9, and 10 of the CGT Prakas. •For all other types of capital assets, the actual deduction method shall be applied. −In cases where the actual expenses exceed the income from the sale of transfer of property (i.e., effectively resulting in a “capital loss”), the “capital loss” shall not be eligible for refund or deduction against “capital gains” derived from other properties. |

|

| Selling Price of “capital assets” other than shares [Article 9] | •The selling price of the asset shall be based on the transfer value as stated in the Sale and Purchase Agreement (SPA), and other relevant documents. The GDT has the right to reassess the selling price to determine the real value of the property in accordance with the rules on determining the tax base for Stamp Duty (SD) or based on the value determined by the Property Evaluation Committee for CGT. | |

| Selling Price of shares [Article 10] | •The selling price of the shares shall be based on the transfer value as stated in the SPA and other relevant documents. •A sale or transfer of shares may also occur in any transaction or event that results in the taxpayer losing the right over, the control of, or the management of the shares (wholly or partly). Such events include sale or transfer, seizure by law, exchanges, donation, withdrawal, and dissolution of the business. In this case, transactions or events (e.g., donation, withdrawal, dissolution) which are treated as sales or transfers but are not backed by contract shall be based on the fair market value. |

|

| CGT declaration and payment [Article 11] | •Taxpayers shall file a CGT declaration determined by the GDT and pay the CGT (for each transaction) within three months of when the capital gains were realized as per Article 4. •For “capital assets”, other than shares, located in Phnom Penh, the CGT shall be declared and paid at the GDT. Otherwise, the CGT shall be declared and paid at the provincial tax branch where the asset is located, or at the GDT (upon the taxpayer’s request). •For the transfer of shares, the enterprise, whose shares are being transferred, is obligated to withhold, declare, and pay the CGT realized by the shareholders. •For sale or transfer of investment assets listed in the Cambodia Securities Exchange, the payment agent is obligated to withhold, declare, and pay the CGT. •For foreign exchange trading and other financial asset transactions made by a person through enterprises licensed by the Securities and Exchange Regulator of Cambodia, the payment agent is obligated to withhold, declare, and pay the CGT. |

|

| CGT on assets located outside of Cambodia [Article 12] | •Where a resident (physical) taxpayer realized capital gains from assets located outside of Cambodia, and the capital gain was subjected to capital gains tax under foreign tax law, if the tax paid in the foreign country is less than the CGT payable calculated under Article 9 or 10 of this Prakas, the taxpayer will only need to pay the additional tax on the difference. | |

| Tax Audit [Article 14] | •GDT has the power to conduct tax audits to reassess the tax base and the tax payable in accordance with the applicable laws and regulations. | |

| Validity of the Transfer of Capital [Article 15] | •Any transfer of ownership or possession rights over the capital is not legally valid where CGT has not been paid | |

| Capital gains realized by a registered taxpayer [Article 16] | •Capital gains realized by a taxpayer under the self-assessment regime (i.e., VAT-registered) shall be covered by the provisions on Tax on Income (ToI). | |

| Double Taxation Agreements (DTA) [Article 17] | •A person who is a resident of a DTA-partner State of Cambodia shall apply the provisions in the DTA related to capital gains, as well as the rules and procedures on the implementation of the DTA. | |

| Indirect sale or transfer of shares [Article 18] | •CGT arising from the indirect sale or transfer of shares is not covered by this Prakas and shall be governed under separate provisions. | |

Any provisions contrary to this Prakas shall be abrogated.

Our comment:

The issuance of the new CGT Prakas represents a landmark regulation for Cambodia, addressing implementation of a regulated CGT regime and minimizing overall tax leakage. Under this regulation, capital gains transactions realized by resident (individual) taxpayers and non-resident taxpayers holding Cambodian assets will now be subject to a 20% CGT in Cambodia. Effectively, capital gains realized by resident taxpayers who are registered for VAT will be subject to a 20% tax rate under the ToI regime. In contrast, capital gains realized by non-VAT registered taxpayers, whether resident or non-resident, will be subject to a 20% CGT under the new CGT regime.

This new CGT Prakas clarifies several "grey areas" and concerns that arose when the initial CGT Prakas 346 was released in 2020, and the subsequent Prakas no. 228 released in 2022. Key highlights include:

•The new CGT regulation clarifies that the issuance of new shares for the purpose of increasing the capital or injecting new investment shall not be considered as a sale or transfer of shares; hence, it is not subject to CGT.

•Capital gains subjected to 20% CGT on the sale or transfer of shares held by non-residents is exempted from the 14% WHT imposed on capital gains from Cambodian-sourced income, as well as exempted from the 14% WHT imposed on the RE as “deemed dividends”. This clarifies the potential concern over “double taxation”.

•Prakas no. 496 further clarifies the basis of the selling price and the allowable deductible expenses for the purpose of calculating the capital gains. It also provides guidance on the CGT taxing points or the taxable events to assess when the capital gains are considered as “realized”.

Notwithstanding the above, there remain some points that are not addressed but are generally accepted principles in the application of a capital gains tax regime. For instance, the mechanism for calculating the net capital gains disregards “asset indexation” rules, which could potentially lead to some future valuation concerns on subsequent sale/transfer transactions: there is no provision to roll over a gain on the replacement of a similar asset, and there are no provisions to shelter gains on intragroup restructures.

In addition, although it is clarified that indirect share transfers are not covered by this Prakas, it remains to be seen whether Cambodia intends to impose tax on indirect transfers under a separate tax regulation and how the provisions of the new CGT regulations interact with the provisions under the existing DTAs with Cambodia regarding capital gains transactions.

Another concern noted is the administration and implementation of the CGT declaration process. As noted, under specific circumstances, the burden of the tax declaration and payment is shifted to the Cambodian investee or the payment agents. There is a question as to whether these entities are privy to the information necessary to calculate the taxable gain (or loss) arising from the transaction. There is also a concern as to how these entities will “withhold” or recover the tax paid to the GDT from the actual income recipients, especially non-residents.

However, the steps taken through the issue of this regulation are welcomed as further evidence of the momentum the GDT have shown in the clarification and implementation of the Cambodian tax regulations with a view to supporting investment decisions.

This new CGT regulation emphasizes the importance of having a properly documented SPA, the basis of the selling price applied per SPA, as well as the relevant records and documentation on the costs and direct expenses incurred on the sale/transfer transaction. In this case, lawyers, bookkeepers, accountants, and/or tax professionals will play vital roles in ensuring that the SPA, the tax declaration, and the tax payments are made in accordance with the tax laws and regulations.

Given the limited time before the 20% CGT is fully implemented, impacted taxpayers are highly encouraged to seek expert advice to navigate the impact of these changes to their portfolio, or any restructuring plans.

As committed tax advisors to our clients, we welcome any opportunities to discuss the relevance of the above matters to your business.

Connect with us

- Find office locations kpmg.findOfficeLocations

- kpmg.emailUs

- Social media @ KPMG kpmg.socialMedia