CSDDD: Background and Scope

The Corporate Sustainability Due Diligence Directive (also known as CSDDD or CS3D) sets out a corporate due diligence duty for large companies to identify and address adverse human rights impacts (such as child labour) and environmental impacts (such as pollution). These duties are in effect for the company’s own operations, but also those of their subsidiaries and in the company’s “chain(s) of activities” [1]. The CSDDD was adopted by the EU Parliament in April 2024 after extensive political negotiations and compromises which narrowed its initial scope [2].

The CSDDD, often referred to as a “sister” directive of the Corporate Sustainability Reporting Directive (CSRD), forms part of a broad package of legal instruments under the EU Green Deal. These directives present several positive synergies despite differing in scope, timeline and obligations (see this article for more details). One example is that companies in scope of both directives will be mandated to develop a climate transition plan by the CSDDD and disclose such plan in the sustainability statement under the CSRD.

The current scope of the CSDDD is limited to the following categories of large companies:

- EU companies having both >1,000 employees and an annual turnover >€450 million

- Non-EU companies with an annual turnover in the EU >€450 million

- Franchising or licensing agreements

a. EU franchised companies having both >1,000 employees and an annual turnover >€80 million, and €22.5 million in royalties

b. Non-EU franchised companies with an annual turnover >€80 million, and €22.5 million in royalties in the EU

Activities in scope will cover the upstream value chain and own operations, as well as distribution, transport and storage of the products.

How will Maltese companies be affected by the CSDDD?

As the European Union continues to push forward with its ambitious sustainability agenda across the whole territory, large Maltese companies will be impacted by the obligations of the CSDDD, which marks a significant milestone for fostering responsible business conduct.

Companies in scope will be held accountable for environmental damage or human rights violations throughout their own operations and value chain. Requirements include integrating due diligence into organisational policies and risk management systems, preventing and mitigating adverse impacts, publicly communicating due diligence, and adopting a climate transition plan in line with the Paris agreement. The number of Maltese companies which are directly impacted by the CSDDD is expected to be limited, however, smaller companies which operate in the supply chains of those in scope of the CSDDD could be indirectly impacted as they will likely be asked for certain environmental and/or social credentials.

Companies that are already engaged in evaluating the sustainability of their supply chain, such as by calculating scope 3 (value chain) emissions and setting science-based targets for their reduction, will likely have a higher level of readiness for the CSDDD. This will be the case regardless of whether they are impacted directly or indirectly by the CSDDD.

Timelines, challenges, and opportunities

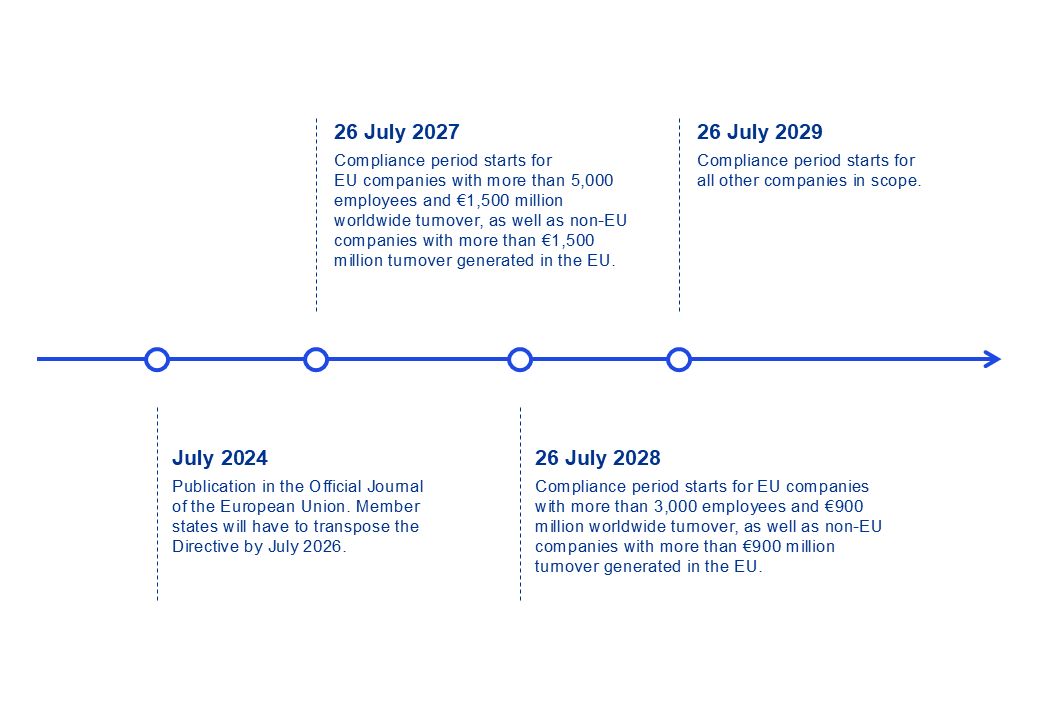

The compliance period for the CSDDD will differ based on the company size and turnover:

In Malta, the Directive is expected to be transposed into domestic legislation within two years from its entry into force, i.e. by July 2026. Compliance requirements are staggered depending on the size of the company, starting in 2027.

While the CSDDD presents several challenges, including the need for comprehensive due diligence systems and potential increased expenses, it may also present opportunities. By prioritising sustainability, companies can enhance their reputations, build stronger relationships with stakeholders, and contribute to a more sustainable future. Companies that proactively embrace these changes will likely find themselves better prepared for future regulatory developments and market demands.

Are you ready to embrace the changes the CSDDD will (directly or indirectly) bring to your company?

Liaise with us to learn more about the new CSDDD reporting requirements and what you can do to be prepared.