Future of telco

Insights on four future telecoms business models and practical steps to help telecoms leaders envision and create the future.

Insights on four future telecoms business models and practical steps to help telecoms ....

EN | TH

Today’s market conditions are creating challenging times for telco players. Even though consumer revenue has been historically high, margins are being squeezed because of the massive infrastructure investment telcos made in 5G to meet the COVID-19 spike in broadband demand and the anticipated explosion in demand driven by various 5G use cases. Competition has been heating up from both traditional and non-traditional players. Customer expectations and the market have been shifting, and a looming recession and regulatory pressures have created uncertainty.

In the latest report, Future of telco, KPMG International spoke with over 300 customer-centric strategy decision-makers at telecommunication organizations across the globe to identify key signals of change taking place across the industry, alongside what KPMG professionals believe will be the four dominant future business models for telecommunication organizations. To survive and grow in this new reality, organizations should consider how a connected approach, underpinned by technology to support the front, middle, and back office, will enable true value from digital transformation.

Signals of change

While change is constant in the telco business, the factors driving change are constantly shifting. KPMG identifies and drills down into some of the most significant market factors that should currently be on telco leaders’ minds:

- Traditional business models are being challenged

- Escalating customer expectations

- Hyper-competitive hyperscalers

- A possible global recession

- Technology can create new opportunities - and threats

- Fulfilling the ESG agenda

- Telcos likely can’t avoid stricter regulations indefinitely

Strategic imperative: the future telecoms business models

As the signals of change put pressure on traditional telco business models, we see various strategic imperatives emerging related to each one. One of the telco leaders’ primary challenges is deciding how they will address the changes to enhance their future growth potential.

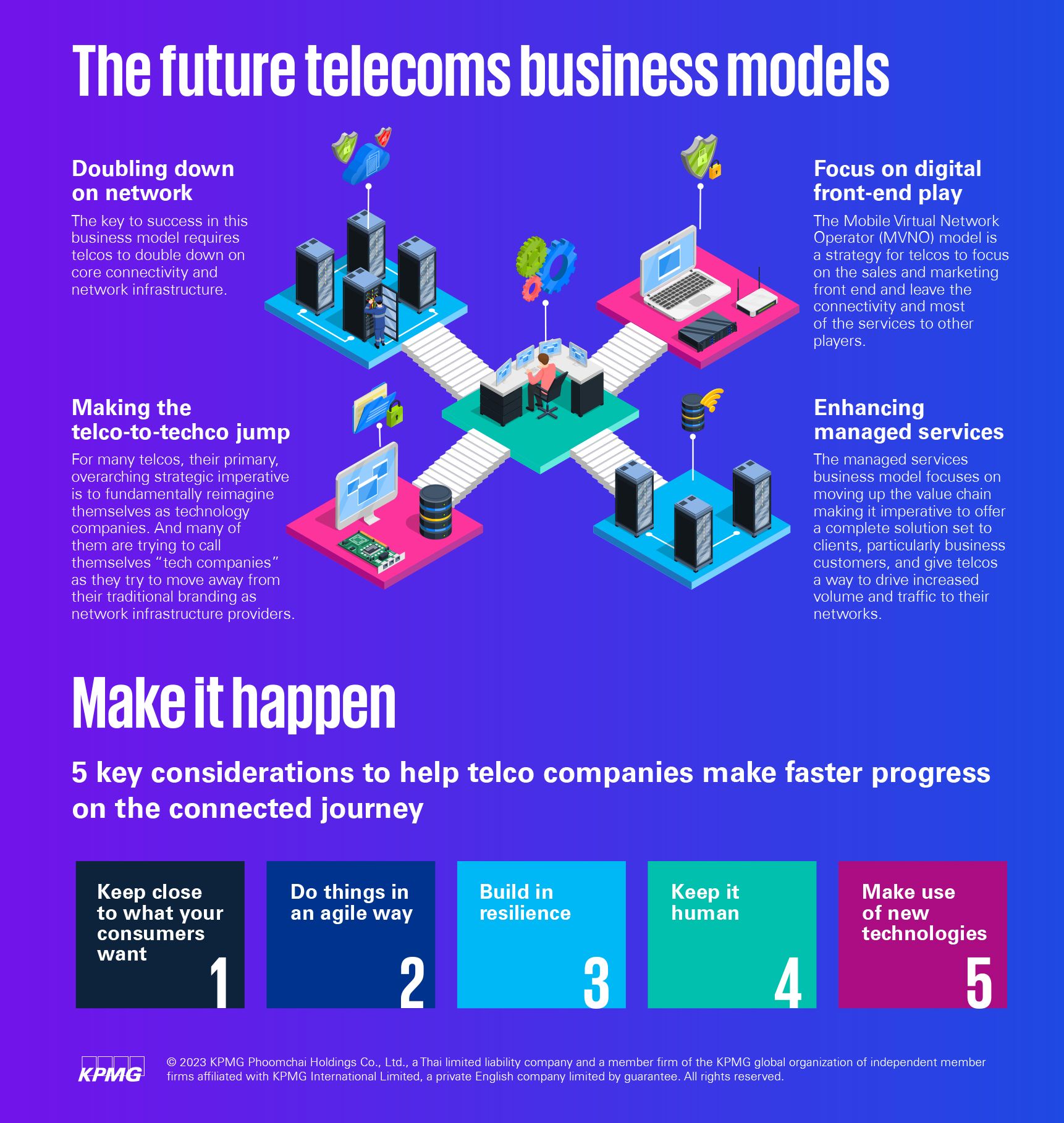

- Doubling down on network: The key to success in this business model requires telcos to double down on core connectivity and network infrastructure. This requires sticking to what made them great and focusing on delivering connectivity at scale, speed, and high availability. It leverages existing capital assets and infrastructure investments and requires little change in operating or business models. However, this model is likely doomed to commoditization and continuously squeezed margins without new growth in the network. To be sure, part of the allure of the connectivity play is hammering costs down through scale. Yet connectivity players should still find new paths to grow and increase network traffic if they hope to make the model sustainable.

- Focus on digital front-end play: The Mobile Virtual Network Operator (MVNO) model is a strategy for telcos to focus on the sales and marketing front end and leave the connectivity and most of the services to other players. MVNOs and additional "asset-light" models allow telcos to scale up or down as volumes and demand requirements evolve, thereby helping to improve overall margins, reducing costs, and driving simplicity. The challenge is maintaining subscriber numbers in a highly competitive yet increasingly commoditized sector. Success at the digital front-end play can require a significant partnership and alliance ecosystem. It can also require a greater focus on innovative products and improving the customer experience. And players should be much more responsive in their operations and supply chain to help ensure they meet customer expectations.

- Enhancing managed services: The managed services business model focuses on moving up the value chain making it imperative to offer a complete solution set to clients, particularly business customers, and give telcos a way to drive increased volume and traffic to their networks. This model could manifest in a range of innovative value propositions. On the business-to-business side, telcos already offer solutions like managed security services and managed network services, such as Network as a Service (NaaS). Some are now tailoring these services within specific verticals to create unique solution sets centered around connectivity for healthcare, banking, insurance, manufacturing, and retail. However, the organization’s ability to become more connected across the back, middle, and front offices can help drive the success and sustainability of this model. That will be the key to uncovering new services, building better ecosystems, creating insight-driven strategies, and delivering better experiences through more digitally-enabled technology architecture.

- Making the telco-to-techco jump: For many telcos, their primary, overarching strategic imperative is to fundamentally reimagine themselves as technology companies. And many of them are trying to call themselves “tech companies” as they try to move away from their traditional branding as network infrastructure providers. They are leaning into that claim by launching new products and services that help them move up the technology stack. But it is not likely they will accomplish this without partners like hyperscalers or other industry-based application solution providers. Essentially, telcos are bundling networks and applications/solutions from partners to help them get to that coveted tech company branding. This is causing the lines to become increasingly blurred as hyperscalers evolve their innovation strategies and advance their deep-pocket agendas. At the same time, legacy telcos embrace a too-big-to-fail mindset.

Making it happen

There are key considerations that can help telco companies make faster progress on the connected journey:

- Keep close to what your consumers want: The ability to think "outside-in" is key to building a customer-centric business. Keep continually looking up and outside the organization and industry to help ensure alignment with some of the best consumer experiences.

- Do things in an agile way: Break changes down into specific steps, sequences and then implement them. Keep standing back to assess whether the change has been successful in a "test-and-learn" approach.

- Build in resilience: Take on today's challenges with resilience and determination, and be prepared to expect the unexpected, fail fast, and learn along the way.

- Keep it human: While embedding new technologies, such as artificial intelligence (Al) and automation, is critical in developing more seamless consumer interactions, remember that you also need to keep the experience "real."

- Make use of new technologies: Experiment with the opportunities available through the cloud, machine learning, and advances in data science.

About KPMG International

KPMG is a global organization of independent professional services firms providing Audit, Tax, and Advisory services. We operate in 143 countries and territories and FY22 had close to 265,000 people working in member firms around the world. Each KPMG firm is a legally distinct and separate entity and describes itself as such.

About KPMG in Thailand

KPMG in Thailand, with more than 2,000 professionals offering Audit and Assurance, Legal, Tax, and Advisory services, is a member firm of the KPMG global organization of independent member firms affiliated with KPMG International Limited, a private English company limited by guarantee.

For media queries, please contact:

Kampanat Induang

E: kampanati@kpmg.co.th