Swiss SMEs are increasingly asked to provide structured sustainability and ESG information – whether by large customers subject to CSRD, by banks assessing ESG risks, or by business partners and investors with growing transparency expectations.

While many SMEs are not legally required to report under CSRD or Swiss Code of Obligations thresholds, sustainability reporting is becoming a de‑facto market expectation.

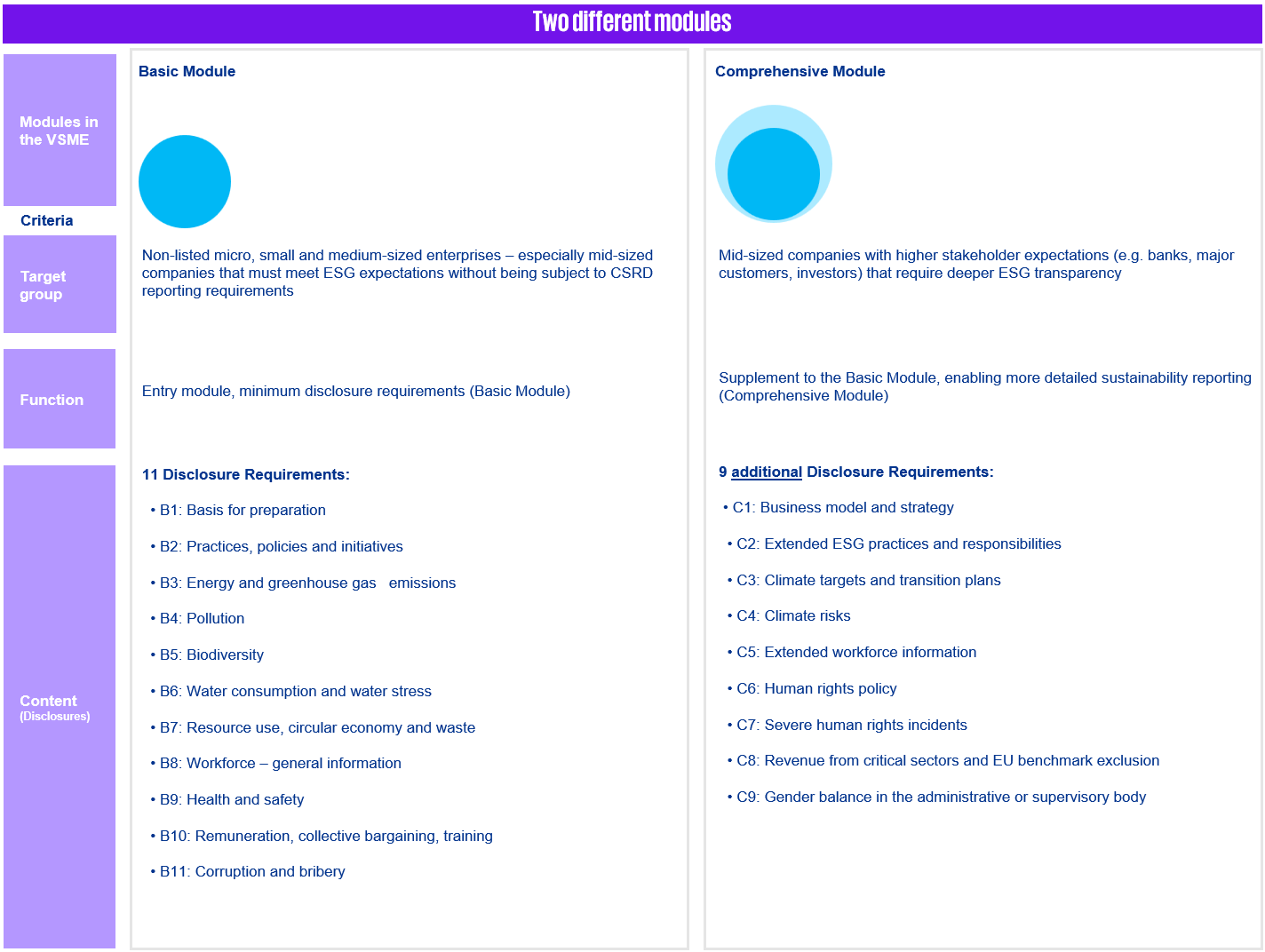

The Voluntary Sustainability Reporting Standard for non‑listed SMEs (VSME) offers a practical, proportionate response. Developed by EFRAG and recommended by the European Commission, the VSME provides a standardized and internationally recognized framework tailored to SME realities. It focuses on the most relevant environmental, social and governance topics, without excessive complexity or cost. For Swiss SMEs, the VSME enables consistent responses to ESG data requests, strengthens stakeholder communication and supports future‑ready sustainability management.