On 14 March 2022, the OECD/G20 Inclusive Framework on BEPS (IF) published the Commentary on the GloBE Model Rules and Illustrative Examples to provide comprehensive technical guidance on the interpretation and application of the GloBE Model Rules released in December last year. For our update on the release of the Commentary and Illustrative Examples with a highlight of some of the key issues discussed or clarified in the documents, please refer to this link.

Release of the GloBE Rules Commentary and Illustrative Examples under Pillar 2 of BEPS 2.0

Updated analysis of the GloBE Rules

Hong Kong business considerations

In addition to the key issues highlighted in our update and the global publications mentioned above, we discuss below some other issues arising from the GloBE Model Rules that are more commonly encountered by the businesses in Hong Kong, taking into account the guidance provided in the Commentary and Illustrative Examples.

1. Treatment of losses

The following are common issues that business groups with losses need to consider:

- Treatment of losses in general – current year GloBE losses of a constituent entity (CE) in a jurisdiction can be used to set off against the current year GloBE income of other CEs in the same jurisdiction in computing the effective tax rate (ETR) of the jurisdiction. Unutilised prior year losses and pre-regime losses cannot be used to reduce the GloBE income in the current year but will be taken into account by means of the adjusted deferred tax approach - i.e. the associated deferred tax expenses will increase the Covered Taxes amount in the year when the losses are utilised and the related deferred tax asset (DTA) is reversed.

- Deemed DTA for losses - Under the GloBE Rules, a deemed DTA for current year losses will be generated at 15% rate even if no such DTA is recognised for financial accounting purposes because the recognition criteria are not met (i.e. no forecast of future profits). Any subsequent valuation adjustments or accounting recognition adjustments with respect to the DTA will be disregarded. For the purposes of computing the jurisdictional ETR, this means there will be (1) a reduction in deferred tax expenses (and Covered Taxes amount) in the year of loss and (2) an increase in deferred tax expenses (and Covered Taxes amount) in the year the loss is utilised for tax purposes. The Commentary on Article 4.4.2 contains an example to illustrate the above.

- Pre-regime losses – while the Commentary on Article 9.1.1 includes an example to make it clear that the deferred tax benefit associated with the pre-regime losses can be taken into account when computing the jurisdictional ETR, one should be mindful that (1) the pre-regime loss DTA is subject to recast at the lower of 15% and the applicable domestic corporate income tax (CIT) rate, (2) utilisation of such deferred tax benefit is subject to the availability of profits in future years for offsetting the pre-regime losses and (3) a pre-existing DTA is available for use for GloBE Rules purposes when it is used for financial reporting purposes in a fiscal year in which the GloBE Rules apply.

- GloBE additional top-up tax in a year with GloBE loss – GloBE top-up tax will generally not arise in a year with an overall GloBE loss in a jurisdiction but there is an exception i.e. when there are (1) an overall GloBE loss and (2) book-to-tax permanent difference(s) in a jurisdiction – please refer to the following example that illustrates this.

Example 1:

GloBE income / loss for Hong Kong | Tax base for Hong Kong | ||

Income Capital gain from disposal of long term immovable property in HK Expenditure | 100 40 (220) | Income Expenditure (20 related to the capital gain is disallowed) | 100 (200) |

GloBE income (loss) | (80) | Total tax profit (loss) | (100) |

Expected Adjusted Covered Taxes | (12) | Adjusted Covered Taxes | (15) |

In the above example, there will be a top-up tax of 3 (i.e. 15 - 12) for Hong Kong even though there is a GloBE loss, effectively taxing the excess benefit of 20 (i.e. 40 – 20) resulting from the permanent difference on non-taxable capital gains in the year it is created at 15%. In Hong Kong, other permanent differences that may result in GloBE additional top-up tax in a loss year include: non-taxable offshore income, tax-exempt interest income and super R&D tax deduction.

Key takeaway: Treatment of losses is a complicated area under the GloBE Rules. MNE groups with loss-making entities should identify which losses are available for reducing their top-up taxes, assess whether any work can be done to ensure those losses are used effectively, and understand the impact of the losses on their overall tax position.

2.Use of deferred tax attributes in computing the ETR

While it is clear from the GloBE Rules and Commentary that the adjusted deferred tax accounting approach is adopted to deal with temporary differences and losses in computing the ETR of a jurisdiction, the exact amount of deferred tax attributes that can be taken into account in the ETR computation may be different from the amount used for financial reporting purposes because of the various adjustments required, including but not limited to:

- the deferred tax expenses accrued in the financial accounts may need to be recast at 15%;

- deferred tax expenses related to items excluded from the computation of the GloBE income or loss and uncertain tax positions have to be excluded;

- the impact of any valuation adjustment or accounting recognition adjustment with respect to a DTA is to be disregarded; and

- deferred tax attributes “disclosed” as opposed to “recognized” in the financial accounts at the beginning of a Transition Year will be taken into account.

Key takeaway: The above suggests that a separate computation as well as tracking and tracing mechanism for GloBE deferred tax attributes is likely to be required in addition to those for financial reporting purposes. Moreover, a detailed analysis of the different components of the deferred tax attributes may be necessary to correctly determine the various adjustments required. MNE groups need to review their existing accounting system and reporting resources and evaluate whether they will be sufficient to generate the necessary information for future GloBE Rules compliance. The Commentary states that the GloBE Implementation Framework will consider providing Agreed Administrative Guidance related to the measurement and treatment of DTA and deferred tax liability (DTL) items in the Transition Year and subsequent years.

3.Withholding taxes treated as Covered Taxes

The Commentary confirms that withholding taxes (WHT) on interest, royalties, rent and insurance premiums, etc. that are imposed in lieu of a generally applicable CIT are Covered Taxes. Instead of recording the gross amount received as income and the associated WHT as expenses in separate lines in the financial accounts, some business groups may net off the gross income with the WHT expenses and recorded the net amount in the financial accounts if the amounts involved are immaterial.

Key takeaway: Going forward, business groups should consider recognising the gross amount of passive income and the related WHT expenses separately to ensure the correct quantum of WHT with respect to their passive income is reflected in the financial accounts and included as Covered Taxes in the ETR computation.

4.Impact of post-filing adjustments

The GloBE Rules require an increase in Covered Taxes for a previous fiscal year as a result of a post-filing adjustment be treated as an increase in Covered Taxes in the current year (i.e. the year in which the post-filing adjustment is made). In contrast, a decrease in Covered Taxes for a previous year due to a post-filing adjustment generally requires a re-computation of the ETR and top-up tax for that previous year. However, if the decrease is immaterial (i.e. less than EUR 1 million) and the taxpayer has made an election, the decrease can be dealt with in the current year. The Commentary explains that this approach is adopted for simplicity reason on one hand and for effective recapture of any avoided top-up tax in previous years on the other hand.

For Hong Kong which does not allow for loss carry-back, post-filing adjustments may arise due to (1) an error in the computation of the CE’s accounting income or taxable income or (2) a subsequent adjustment to the profits tax liability of a given tax year made by the Inland Revenue Department (IRD) (e.g. by issuing an additional assessment) to subject certain income to tax or disallow the deduction of certain expenses. The simplified example below illustrates the impact of a post-filing adjustment resulting from additional profits taxes charged by the IRD subsequently.

Example 2:

- Assuming the Income Inclusion Rule (IIR) becomes effective in Hong Kong from 1 January 2023

- HK Co with a December year end files the 2023/24 profits tax return with an offshore claim on its interest income in August 2024 and the GloBE information return in June 2025

- The IRD issues a tax assessment for 2023/24 based on the tax return filed initially but disallows the offshore claim on interest income after 2 years (i.e. in 2025/26) after certain rounds of enquiries

The table below shows HK Co’s GloBE Rules positions in 2023/24 (i.e. the year to which the post-filing adjustment is related) and 2025/26 (the year in which the post-filing adjustment is made):

GloBE Rules position for year ended 31 December 2023 | GloBE Rules position for year ended 31 December 2025 | ||

Interest income (offshore) Other income (onshore) Expenditure (30 related to the onshore other income and deductible) | 200 50 (50) | Interest income (onshore) Other income (onshore) Expenditure | 300 100 (150)

|

GloBE income (loss) | 200 | GloBE income (loss) | 250 |

Taxable profit (loss): 50 - 30 | 20 | Taxable profit (loss) | 250 |

Profits tax liability for 2023/24: 20 x 16.5% | 3.3 | Profits tax liability for 2025/26: 250 x 16.5% | 41.25 |

Change to Covered Taxes due to post-filing adjustment | 0 | Change to Covered Taxes due to post-filing adjustment (for 2023/24): (200 – 20) x 16.5% | 29.7 |

ETR: 3.3 / 200 | 1.65% | ETR: (41.25 + 29.7) / 250 | 28.4% |

GloBE top-up tax: 200 x (15% - 1.65%) | 26.7 | GloBE top-up tax | 0 |

As shown in the above table, since the increase in Covered Taxes resulting from the post-filing adjustment for 2023/24 (i.e. disallowance of the offshore claim on interest income) has to be included as Covered Taxes for the year 2025 rather than year 2023, HK Co ends up in an undesirable position of paying GloBE top-up tax in year 2023 whereas its ETR for year 2025 is well above 15%.

The same issue will arise if Hong Kong is going to introduce a domestic minimum tax (DMT) regime. That is, a top-up tax of 26.7 will be imposed under the DMT regime (instead of the GloBE Rules) in the year the return is filed and when the IRD subsequently disallows the offshore claim on the interest income, there will be additional profits tax of 29.7, leading to a double taxation in Hong Kong unless the DMT paid will be refunded or can be used to credit against the additional profits tax liability arising from the post-filing adjustment.

Key takeaway: The impact of any post-filing adjustments on a CE will depend on the CE’s ETR in previous as well as future fiscal years. Similarly, as accrued current or deferred tax expenses relating to an uncertain tax position (UTP) need to be excluded from the Covered Taxes amount in the year of accrual and can only be included as Covered Taxes in the year the taxes are actually paid, an undesirable consequence similar to the one in the above example may be resulted for a CE with a UTP. Business groups with uncertain tax issues or issues pending settlement with the IRD should consider the potential impact of such issues on the group’s GloBE Rules positions and evaluate whether any potential adverse impact can be mitigated by an early settlement of the outstanding tax issues with the IRD.

5. Special rule for intra-group financing arrangements

The GLoBE Rules contain special anti-mismatch rule for intra-group financing arrangements. Under this rule, the intra-group financing expense of a CE in a low tax jurisdiction (i.e. ETR < 15%) will need to be added back when computing the CE’s GloBE income or loss if there is not a commensurate increase of taxable income of another CE in a “not a low tax jurisdiction” (i.e. a high tax jurisdiction) with respect to that amount – please refer to the following example that illustrates this rule.

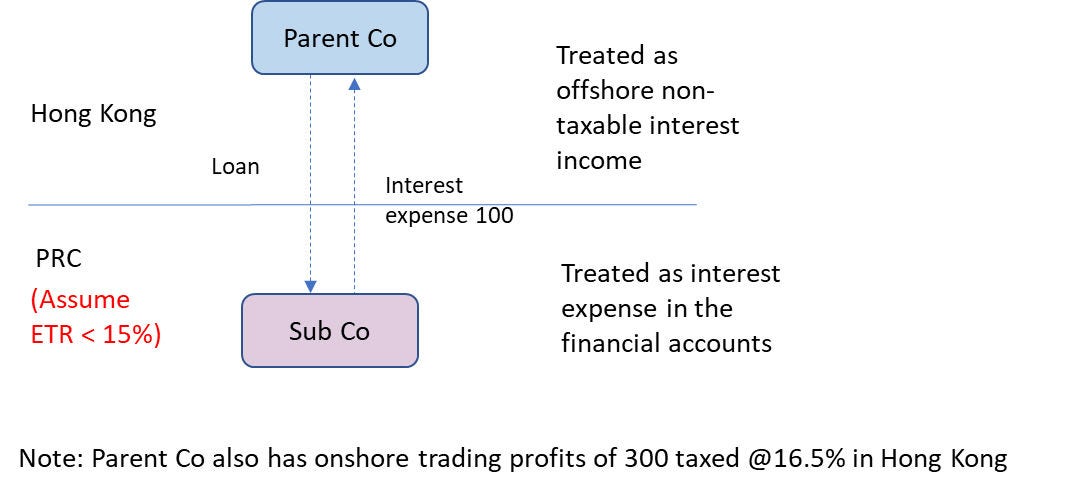

Example 3:

In the above example, Sub Co is located in a low tax jurisdiction and incurred interest expense of 100 under an intra-group financing arrangement with Parent Co. To determine if the anti-mismatch rule will apply, Parent Co needs to determine whether Hong Kong is a high tax jurisdiction with ETR ≥ 15% under the following two scenarios:

| Scenario 1: Is Hong Kong not a low tax jurisdiction under normal ETR calculation? | Scenarios 2: Is Hong Kong not a low tax jurisdiction under ETR calculation disregarding the interest income? | |

| Trading profits 300 @16.5% | ETR for Hong Kong = 49.5/400 = 12.375% | ETR for Hong Kong = 49.5/300 = 16.5% |

| Interest income 100 @0% | ||

| Conclusion | No, since the ETR < 15% | Yes, since the ETR ≥ 15% |

If Hong Kong is a high tax jurisdiction in either Scenario 1 or Scenario 2 (which is the case in the above example), the anti-mismatch rule will apply and the interest expense of 100 of Sub Co will need to be added back in computing Sub Co’s GloBE income or loss.

Key takeaway: The above example illustrates that the mix of different types of income (both in terms of the amounts and their respective ETR) of Parent Co (i.e. taxable trading income and non-taxable interest income) will affect the ETR computation for Hong Kong and whether the Parent Co is located in a high tax jurisdiction for the purposes of the anti-mismatch rule. The same applies to determining whether Sub Co is located in a low tax jurisdiction. If there are other CEs in the payor’s or the recipient’s jurisdiction, the analysis will become more complicated. Business groups with an intra-group financing arrangement need to perform a detailed analysis on the potential impact of the anti-mismatch rule and consider whether any change in the composition of income derived by the relevant CEs in the jurisdictions concerned is desirable to mitigate any potential adverse impact of the rule.

6. Group structures with minority-owned entities

Special rules for applying the GloBE Rules may apply to a group structure with minority-owned CE(s). The Commentary includes further details and numerical examples on how these special rules are applied. Please refer to the following examples for illustration of the special rules.

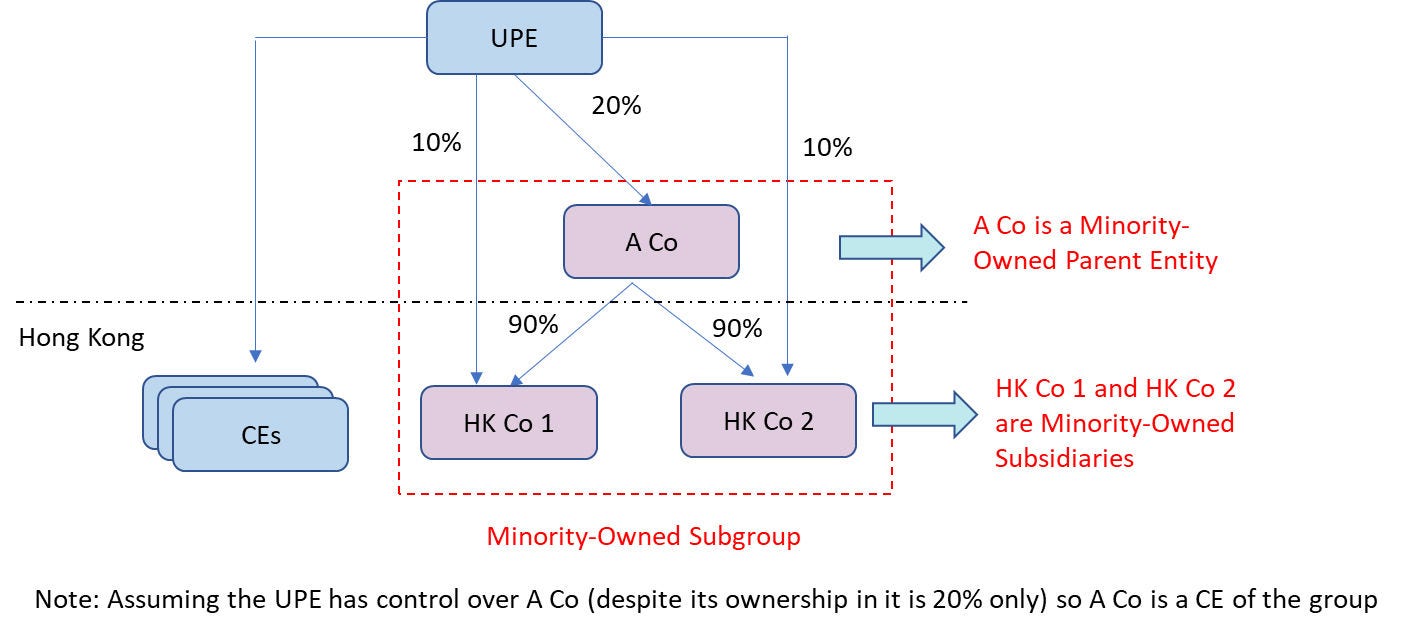

Example 4:

- In this example, A Co is a Minority-Owned Parent Entity (MOPE) as the UPE’s direct or indirect ownership interest in it is 30% or less (i.e. 20%) whereas HK Co 1 and HK Co 2 are its Minority-Owned Subsidiaries because their controlling interests are held by A Co which is a MOPE and the UPE’s ownership interest in them is 30% or less.

- A Co, HK Co 1 and HK Co 2 together form a Minority-Owned Subgroup.

- In this situation, the MNE Group will need to perform two separate ETR computations for Hong Kong, one is the blended ETR in respect to HK Co 1 and HK Co 2 and the other is the blended ETR for the other CEs of the group located in Hong Kong.

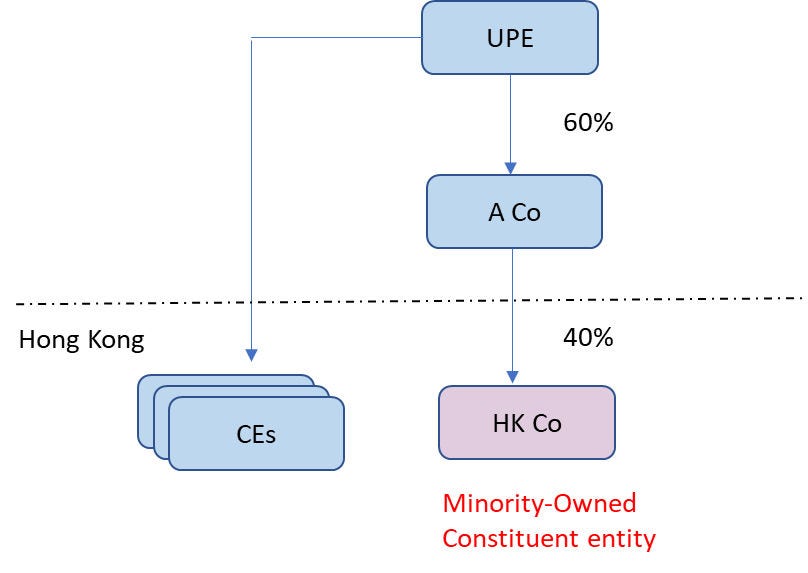

- In this example, HK Co is a Minority-Owned Constituent Entity as the UPE’s direct or indirect ownership interest in it is 30% or less (i.e. 60% x 40% = 24%) and it is not a member of a Minority-Owned Subgroup.

- In this situation, the MNE Group will need to perform two separate ETR computations for Hong Kong, one for HK Co on an entity basis and the other is the blended one for all the other CEs of the MNE group located in Hong Kong.

Key takeaway: Business groups with minority-owned entities within the group structure need to take note of the above special rules for ETR computation, ensure they have access to the information necessary for computing the ETR of the Minority-Owned Subgroup(s) and/or Minority-Owned CE(s) on a separate basis, and consider whether any group structuring is desirable and feasible.

7. Group structures with minority interests

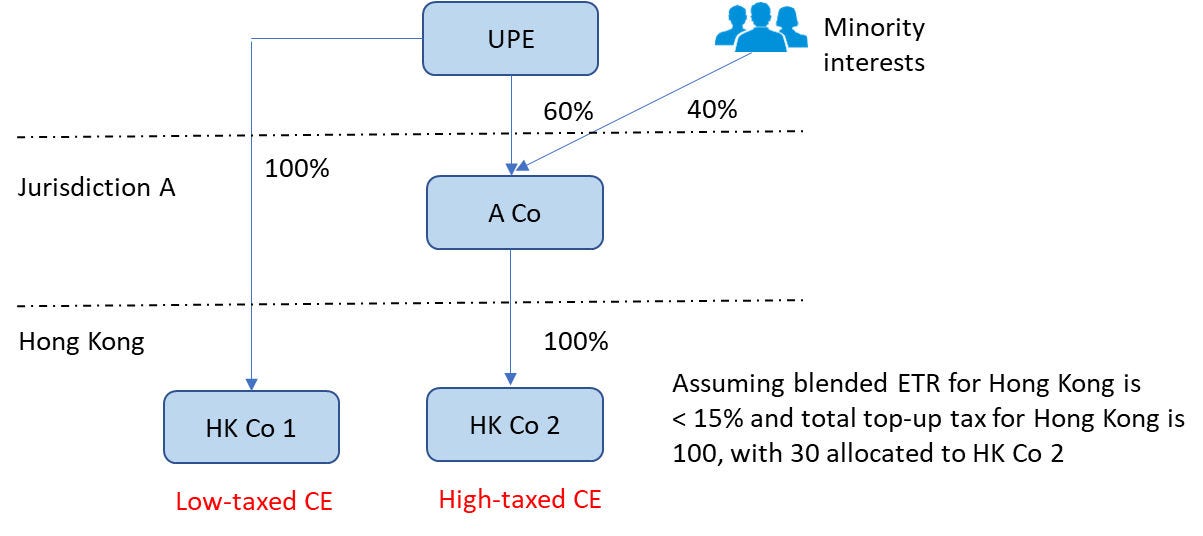

Example 6:

- In this example, A Co is a Partially-Owned Parent Entity as more than 20% of its ownership interests are held directly or indirectly by persons that are not CEs of the group (i.e. the minority interests).

- In this situation, the split ownership rule will apply and Jurisdiction A instead of the UPE jurisdiction will has the priority to apply the IIR in respect of the low-taxed profits in Hong Kong (i.e. A Co has to pay its share of top-up tax of 30).

- Implications to the minority interests – Although the minority interests only have ownership interests in the high-taxed HK Co 2, 12 out of the 30 top-up tax (i.e. 30 x 40%) of HK Co 2 will be attributed to them.

Key takeaway: Business groups with minority interests within the group structure need to take note of the above implications of low-taxed CEs within the group to the minority interests. Proper and advance communication with the minority interests on any potential impact of the GloBE Rules on them is recommended.

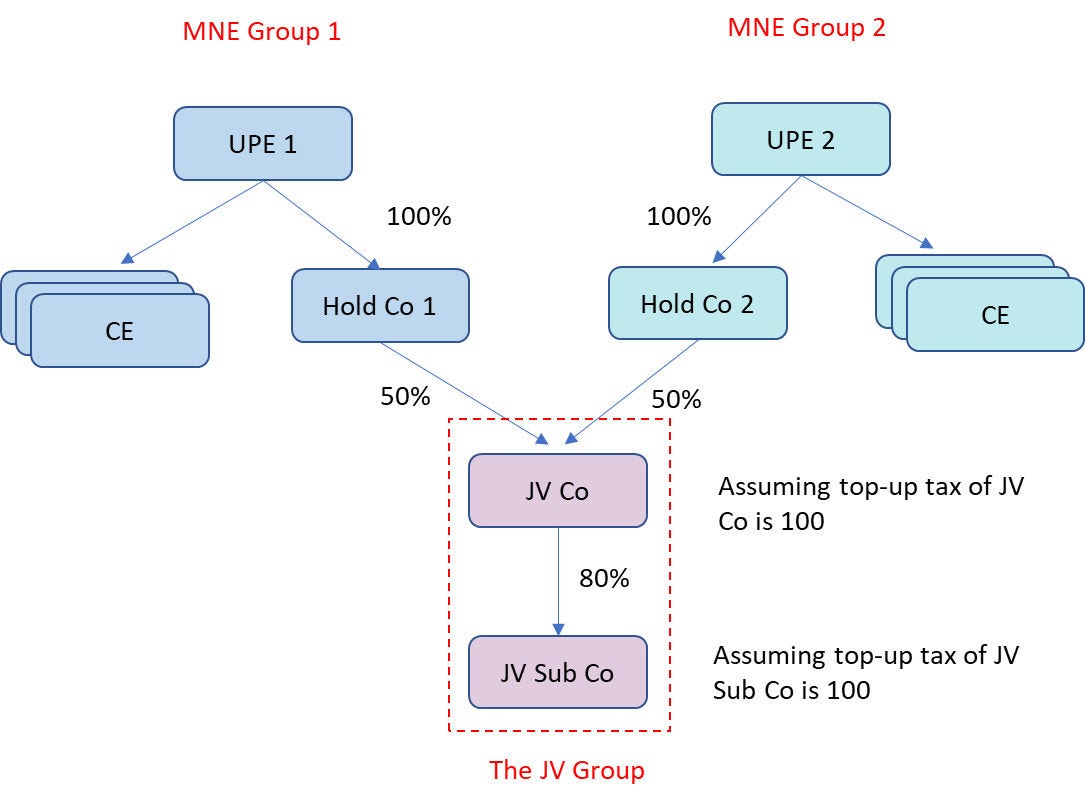

8.Application of the GloBE Rules to joint venture structures

There are special rules for applying the GloBE Rules to a structure with a joint venture (JV) entity. Under the GloBE Rules, the term “joint venture” is defined as “an entity whose financial results are reported under the equity method in the consolidated financial statements of the UPE provided that the UPE holds directly or indirectly at least 50% of its ownership interests”. Accordingly, the special rules do not apply to an entity which may be regarded as a JV under an acceptable accounting standard (because the joint venturers have joint control over it) but where the joint venturers hold less than 50% of the entity’s equity interests.

The Commentary includes further details and numerical examples on how these special rules are applied. Please refer to the following example for illustration of the special rules.

Example 7:

- The top-up tax of a JV Group (i.e. the JV Co and JV Sub Co) is computed as if the members of the JV Group were CEs of a separate MNE group and as if JV Co was the UPE of that group.

- The GloBE income or loss and Covered Taxes of JV Co and JV Sub Co are not blended with the CEs of the wider MNE Groups 1 and 2 for computing the jurisdictional ETRs of MNE Groups 1 and 2 as well as the JV Group.

- Each of UPE 1 and UPE 2 will apply the IIR to determine its share of top-up tax in respect of the low-taxed JV Co (i.e. 100) and JV Sub Co (i.e. 100) and allocate the top-up tax to the CEs within MNE Group 1 and MNE Group 2 respectively.

- Each of UPE 1’s and UPE 2’s share of top-up taxes of (1) JV Co is 50 (100 x 50%) and (2) JV Sub Co is 40 (100 x 50% x 80%) respectively.

Key takeaway: Business groups with a JV entity within the group structure need to take note of the above special rules for ETR computation and ensure they have access to the information necessary for computing the ETR of the JV Group on a separate basis.

9. Issues specific to investment funds and fund managers

Although funds that qualify as an “investment fund” as defined in the GloBE Rules and that are the UPE of an MNE group are excluded entities and therefore not subject to the GloBE Rules, there are a number of issues that funds and fund managers may need to consider:

- Although the interpretation and application of the deeming provision in the definition of “consolidated financial statements” (i.e. in the case where the UPE does not prepare consolidated financial statements, one would refer to the consolidated financial statements that would have been prepared if the UPE were required to prepare such statements in accordance with an authorised financial accounting standard) is not entirely clear, Example 2.4.3 of the Pillar Two Blueprint published by the IF in October 2020 indicates that where an investment fund is (1) an UPE of two MNE groups (each with consolidated revenue of EUR 500 million) and (2) is not required to prepare consolidated financial statements in respect of its investment in the two MNE groups under IFRS 10, the two MNE groups are considered two separate MNE groups and both are out of the scope of the GloBE Rules.

- Although investment funds that are an UPE are an excluded entity, investment fund managers may be subject to the GloBE Rules if they are part of an MNE group of which the annual consolidated revenue is EUR 750 million or more. In-scope investment fund managers deriving carried interest that is either tax exempt or taxed at a preferential rate will need to consider any potential impact of the GloBE Rules, including whether the carried interest can qualify as excluded dividends.

- In addition, investment fund managers need to consider any potential impact of the GloBE Rules on the investee groups of the funds managed by them as any GloBE top-up tax liability on such investee groups will likely affect the expected investment return generated for the funds.

Concluding remarks

The lengthy Commentary and the Illustrative Examples on the GloBE Model Rules demonstrate the complexity in interpreting and applying the rules, which will no doubt present many implementation challenges to both in-scope MNE groups and tax administrations around the globe in the coming years. As a next step, the IF has launched a public consultation on the GloBE Implementation Framework, with an aim to finalise it by the end of this year.

Tax leaders of MNE groups should consider performing a more detailed assessment of the impact of the GloBE Rules on their groups in light of the more detailed explanations and guidance provided in the Commentary. Consideration should also be given to whether there are any system issues in collecting the data or breakdown of items in the financial accounts necessary for performing such detailed assessment and the ongoing GloBE Rules compliance in future.

As far as the GloBE Rules implementation timeline is concerned, the European Union (EU) has came up with a revised proposal for the EU Minimum Tax Directive (the Revised Proposal) in which the following deferred timelines of implementing the GloBE Rules within the EU are proposed:

- the IIR to apply for fiscal years beginning on or after 31 December 2023 (instead of 1 January 2023); and

- an option for EU Member States to defer the application of the IIR and the Undertaxed Payment Rule (UTPR) up to 31 December 2029, if no more than 12 UPEs of in-scope MNE groups are located in those EU Member States.

The EU Member States failed to reach a unanimous agreement on the Revised Proposal in the meeting held on 5 April 2022. It has yet to see whether the EU Member States can reach such agreement on the deferred implementation timelines of the GloBE Rules in the next meeting to be held on 24 May 2022.

It will be interesting to see whether the above EU deferral on implementing the GloBE Rules will have any impact on the implementation timeline of the other jurisdictions, including Hong Kong. For business groups with operations in Hong Kong, they should also keep in mind the impact of any potential changes to the Hong Kong tax system to be effective from 1 January 2023 as a response to the EU’s grey list for tax purposes as this could affect the calculated ETR of the operations in Hong Kong.

Inclusive Framework BEPS Agreement

Update on Pillar 2 following Commentary Release – April 2022