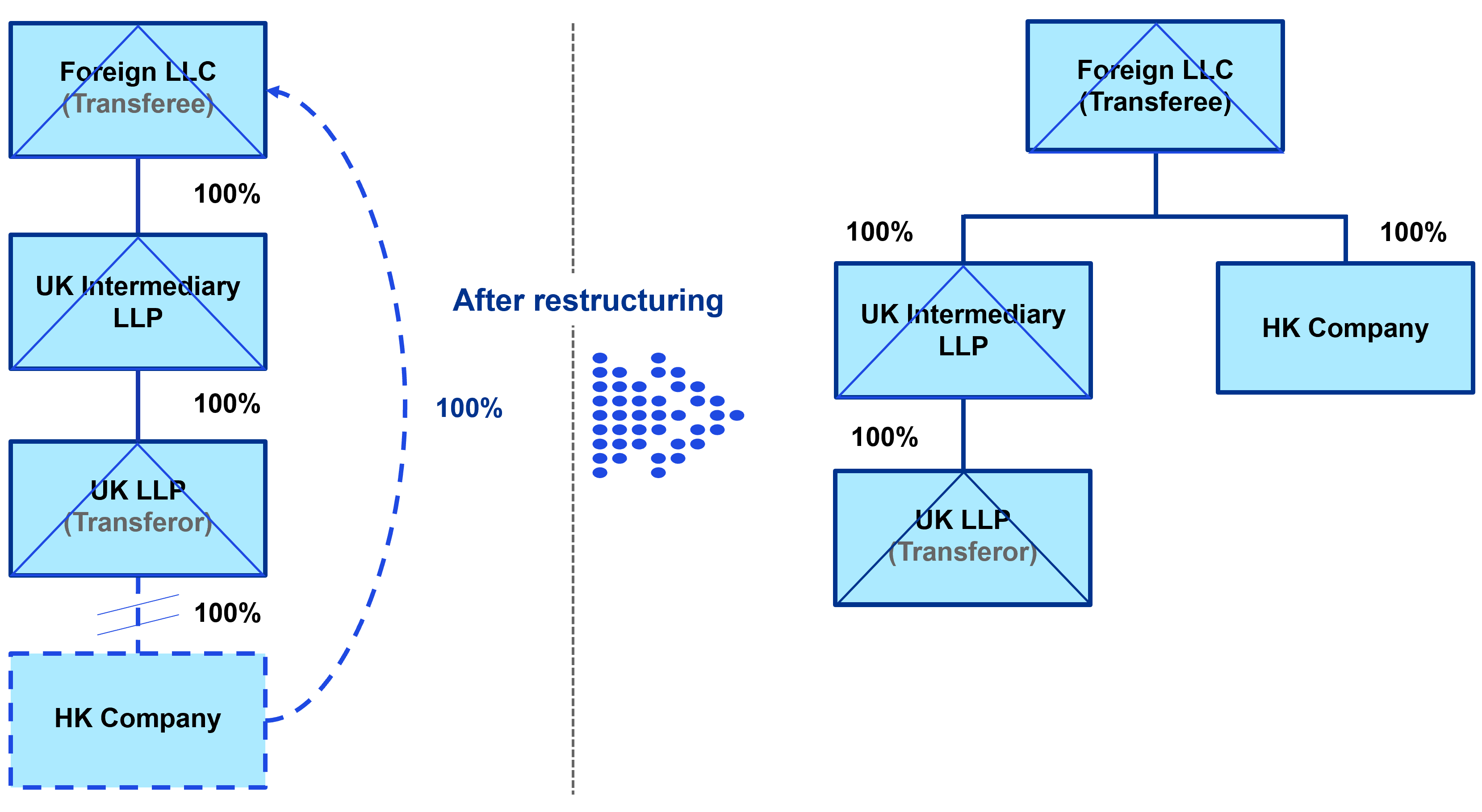

The District Court recently held in a case that a foreign limited liability company (LLC) and a UK limited liability partnership (LLP) were “associated” body corporates within the meaning of section 45 of the Stamp Duty Ordinance (SDO) although the latter did not have any “issued share capital” similar to that of a company limited by shares. Accordingly, the Court held that the intra-group transfer of the shares in a Hong Kong company from the UK LLP to the foreign LLC was entitled to the stamp duty relief under section 45 of the SDO.

In this news alert, we discuss the District Court’s judgment and analysis as well as some of our interesting observations from the case.