We are pleased to see that a number of refinements have been made to the Scheme in the Bill based on the comments received during the March consultation. This shows the government’s efforts in providing greater clarity and tax certainty to taxpayers in respect of non-taxation of onshore equity disposal gains and maintaining the competitiveness of Hong Kong's tax system.

In particular, when comparing the similar legislation implemented in Singapore8, the Scheme in Hong Kong is more competitive in various aspects – e.g. a lower ownership requirement, a wider scope covering different forms of investor/investee entities and equity interests, and the flexibility on measuring the 15% ownership threshold on a group basis, etc.

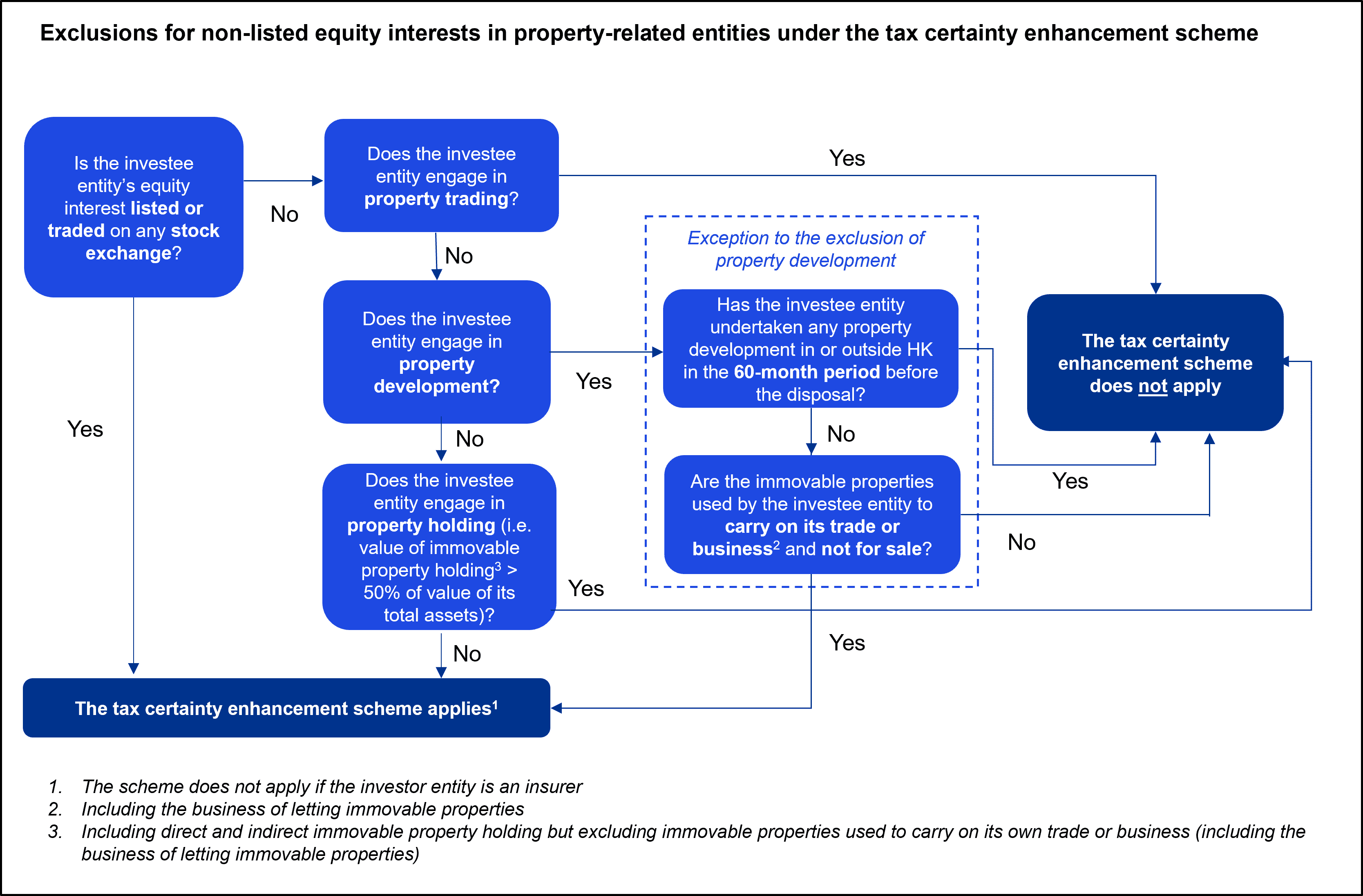

However, the exclusion for trading stock under the Scheme in Hong Kong (which is not found in the Singapore regime) creates some complexity and uncertainty for taxpayers. More guidance and examples from the IRD on the application of such exclusion would be welcomed.

The Scheme offers an alternative option (with a bright-line test) for taxpayers to make a non-taxable claim for onshore equity disposal gains. In cases where the gains do not qualify for the non-taxation treatment under the Scheme, taxpayers can still make a capital claim on their onshore equity disposal gains based on the “badges of trade” principles established by case law.

Business groups in Hong Kong that hold equity investments and plan to divest any of such investments should consider the different Hong Kong profits tax implications arising from the equity disposal gains when such gains are regarded as onshore and offshore sourced respectively. For onshore equity disposal gains, they should assess whether the specified conditions set out in the Scheme can be fulfilled for benefiting from the non-taxation treatment under the Scheme. For offshore equity disposal gains, they should assess whether the economic substance requirement or participation requirement can be fulfilled such that the gains would continue to be non-taxable in view of the foreign-sourced income exemption regime that became effective from 1 January 2023.