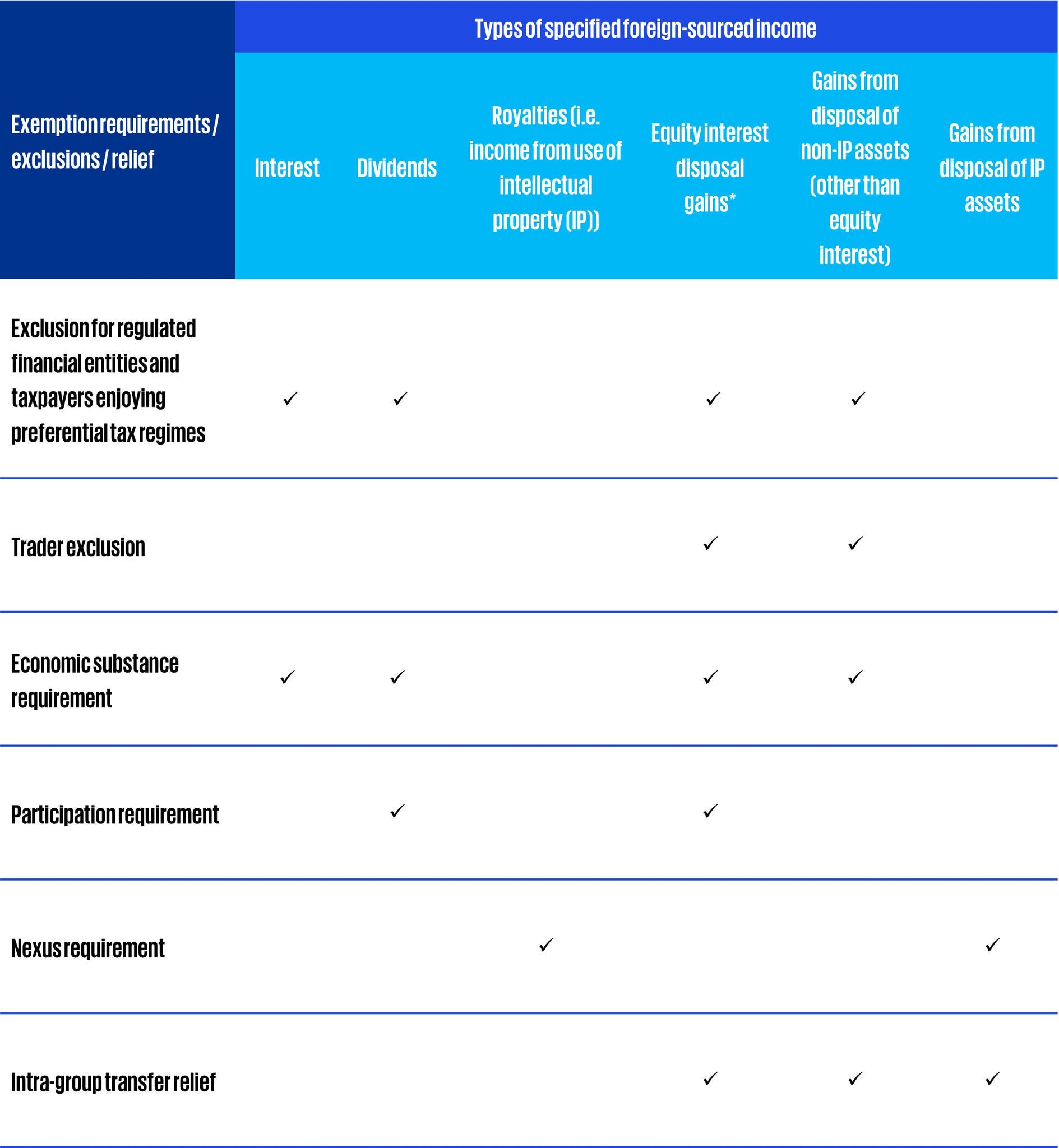

Given the effective date of the expanded FSIE regime is fast approaching, business groups in Hong Kong should assess whether they would be impacted by the expanded FSIE regime and explore possible options (e.g. applying the trader exclusion or building up the necessary economic substance in Hong Kong, etc.) to mitigate the potential impact. Please refer to the table in the Appendix for a summary of the exemption requirements / exclusions / relief for different types of specified foreign-sourced income under the expanded FSIE regime.

Impacted business groups should also stay tuned for the Departmental Interpretation and Practice Notes to be issued by the IRD for additional guidance and examples on how the expanded FSIE regime will be applied in practice.

Referring to Advance Ruling Case No. 72, we have handled a similar advance ruling application and obtained a favourable ruling from the IRD. One particular point to note is for some foreign jurisdictions, the “substantive activities requirement” for a tax incentive is not explicitly mentioned in their domestic tax law. To substantiate that the headline corporate income tax rate instead of the reduced rate under the tax incentive should be referred to as the applicable rate for the purpose of the “subject to tax” condition, it is important for taxpayers to be able to provide other documentary evidence to demonstrate that the tax incentive is actually granted subject to a substance requirement in the relevant foreign jurisdiction and that as a matter of fact, there is adequate economic substance in that jurisdiction.