As the Amendment Ordinance was enacted in June 2022, entities in Hong Kong are required to take into consideration the effect of the Amendment Ordinance when accounting for the LSP provision from the financial year that includes June 2022 (e.g. the financial year ended 31 December 2022 for a December accounting year-end entity).

The guidance3 issued by the HKICPA on 4 July 2023 discusses the acceptable approaches to accounting for the offsetting mechanism, the accounting issues resulting from the Abolition, and the accounting for the impact of the Abolition, etc. The guidance also contains examples that illustrate the related accounting entries.

According to the HKICPA guidance, employers can choose one of the following two acceptable accounting approaches to account for the provision for LSP (including the offset mechanism) and the impact of the Abolition:

Under Approach 1:

- The accrued benefits arising from an employer’s MPF contributions that have been vested with the employee and which would be used to offset the employee’s LSP benefits (offsetable accrued benefits) are treated as a deemed contribution by the employee towards the LSP and a reduction in service cost (i.e. a negative service cost).

- The LSP obligation is measured on a “net” basis after deducting the negative service cost arising from the offsetable accrued benefits.

- The Abolition results in a reduction in expected offsetable accrued benefits. As such, there is a one-off catch-up adjustment recognised as an additional past service cost in the profit or loss and a corresponding increase in the LSP obligation in the year of enactment of the Amendment Ordinance.

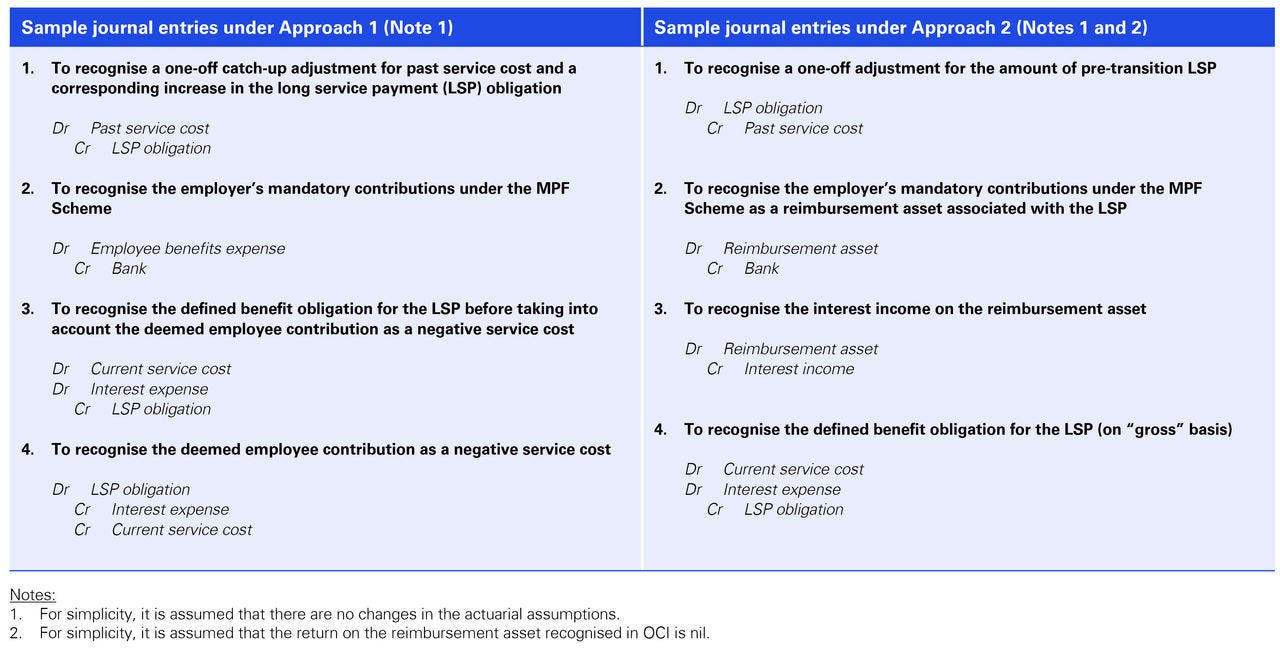

Please refer to Appendix 1 for the sample accounting entries under Approach 1.

Under Approach 2:

- The LSP obligation is measured on a “gross” basis without being reduced by the offsetable accrued benefits.

- Employer’s mandatory MPF contribution is recognised as a separate asset (the Reimbursement Asset) in the balance sheet4 and measured at fair value until the fair value reaches the amount of LSP in respect of the employment period before the Transition Date (i.e. the pre-transition portion of LSP that is offsetable).

- A one-off adjustment is made to the LSP obligation to reflect the change in reference date used for determining the last month’s salary for the purposes of calculating the pre-transition portion of LSP5.

Please refer to Appendix 1 for the sample accounting entries under Approach 2.

In addition, any changes in actuarial assumptions will affect the LSP liability (under both approaches) and the reimbursement asset (under Approach 2) with a corresponding adjustment to Other Comprehensive Income (OCI) as a remeasurement gain or loss.