The Inland Revenue (Amendment) (Minimum Tax for Multinational Enterprise Groups) Bill 2024 (the Bill)1, together with over 100 government proposed amendments2 to the Bill, were passed by the Legislative Council on 28 May 2025. For more detailed discussions of the Bill and the amendments, please refer to our Hong Kong BEPS publication issued in December 2024 and Hong Kong BEPS publication issued in April 2025.

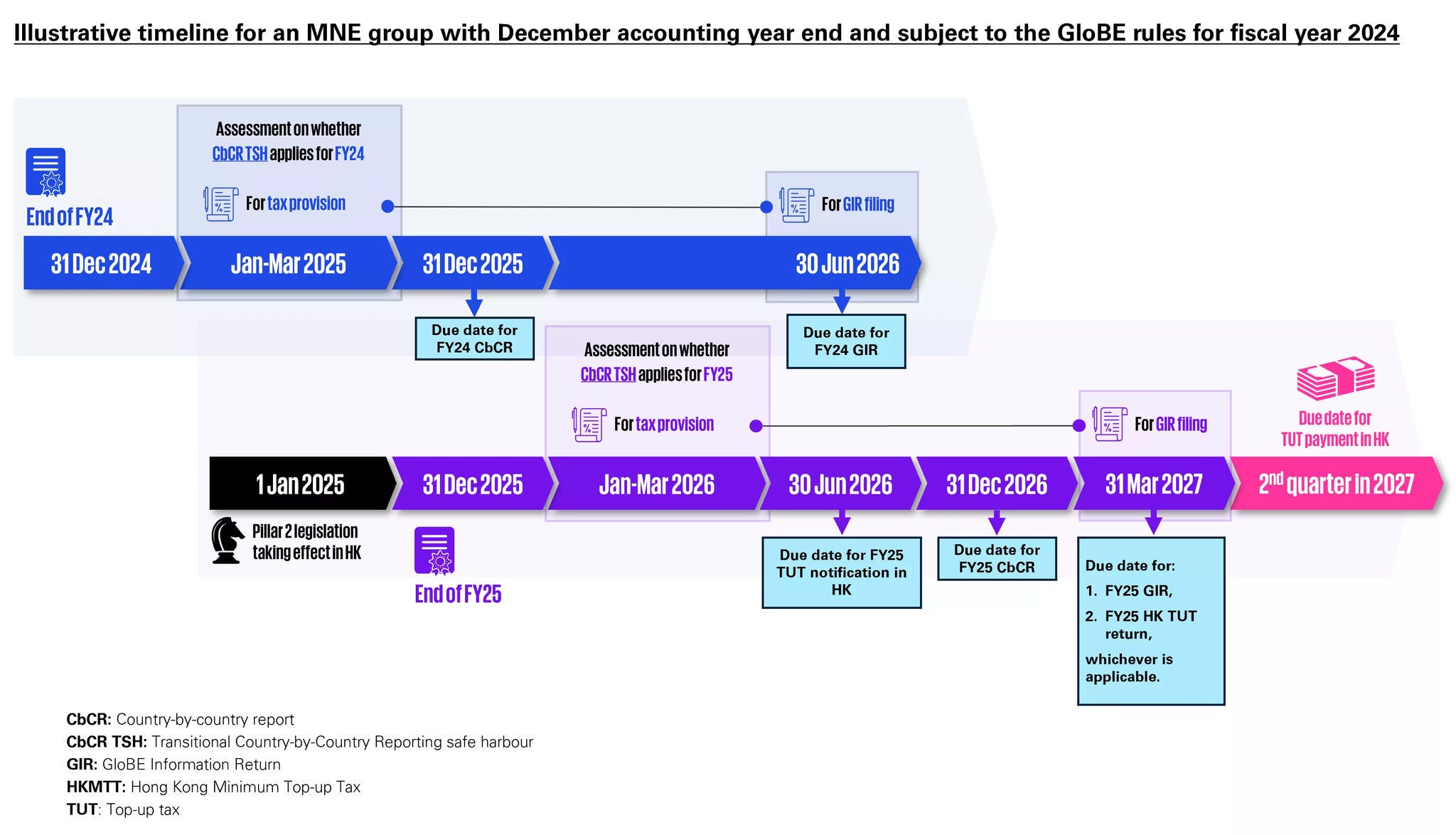

It is expected that the corresponding Ordinance will be gazetted on 6 June 2025 and become effective on the same date. Upon gazettal of the Ordinance, the Income Inclusion Rule (IIR) and Hong Kong Minimum Top-up Tax (HKMTT) will take effect retrospectively in the Hong Kong SAR (Hong Kong) for fiscal years beginning on or after 1 January 2025 whereas the Undertaxed Profits Rule will become effective from a date to be specified by the government at a later stage.

With the introduction of the global and domestic minimum top-up taxes, the Hong Kong tax system has ushered in a new era for large multinational enterprise (MNE) groups. This publication discusses key considerations and immediate actions that large MNE groups should address following the enactment of the Pillar 2 legislation in Hong Kong.