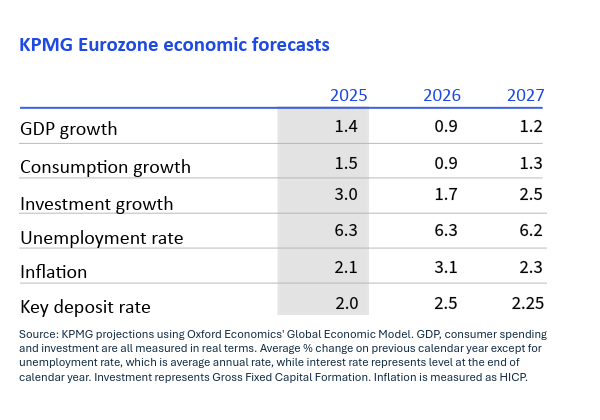

In our latest European Economic Outlook, we consider the potential implications of continued conflict in Iran on growth, inflation and interest rates, and the exposure to a more prolonged conflict.

Download the report for our full analysis. Or read on for a summary.