The source rules for royalty income

Subject to any further appeal by the taxpayer to a higher court, this judgment adds to the existing case authorities in Hong Kong on the source of royalty income, namely the CIR v HK-TVB International Ltd and Lam Soon Trademark Ltd v CIR cases. Consistent with these two precedents and the Inland Revenue Department’s position in Departmental Interpretation and Practice Notes No. 22 on taxation of royalties, the CFI in this case held that the source of royalty income from licensing and sub-licensing of an intellectual property (IP) is the place(s) where the licensing and sub-licensing agreements are effected rather than the place of use of the IP. This is different from the international norm under tax treaties where the place of residence of the royalty payer (which generally is also the place of use of the IP) is regarded as the source state of the royalties.

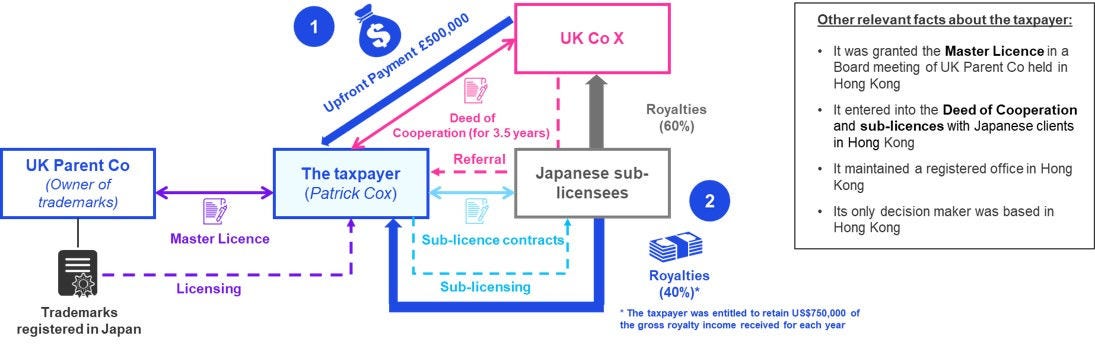

Apportionment between onshore and offshore royalty income

In the present case, it appears that the taxpayer only pursued an offshore claim on the 40% royalties (but not the minimum royalty retained under the same sub-licensing arrangement). It is not clear from what was disclosed in the court judgement whether the minimum royalty was treated as onshore and taxable and if yes, the taxpayer’s basis of adopting differential tax treatments for the two amounts which were both derived under the same sub-licensing arrangement.

DIPN 22 is silent on whether there could be an apportionment of royalty income between onshore and offshore sourced. Also, there have not been any precedent cases specifically dealing with this issue so far. In cases where the activities for producing the royalty income are performed both in and outside Hong Kong, apportionment of the royalty income should be considered.

Capital vs revenue nature of income receipts

While there are relatively more precedent cases in Hong Kong dealing with the issue of whether an expense item is capital or revenue in nature, this case discussed the principles for determining the nature of an income item. In particular, the court pointed out that an item that is a revenue expenditure in the hands of the payer does not necessarily mean the same item is a revenue receipt from the payee’s perspective. In fact, the upfront payment in this case is more akin to a capital expenditure in the hands of UK Co X as it was a one-off payment giving rise to a right that generated a long-term benefit.

Impact of the FSIE regime on foreign-sourced IP-related income

Whatever the final outcome of this case, under the existing foreign-sourced income exemption (FSIE) in Hong Kong, a similar non-taxable claim on offshore royalty income received in Hong Kong by a Hong Kong entity within a multinational group will be available for royalties derived from a patent, or an IP similar to patent only, and subject to the fulfilment of the newly introduced nexus requirement. In addition, under the expanded FSIE regime (i.e. expanded to cover foreign-sourced gains from disposal of all types of assets), effective from 1 January 2024, an upfront payment received under a licensing or sub-licensing arrangement, even if being foreign-sourced and capital in nature, may nevertheless be taxable if it represents an income from sale of a covered asset (which is widely defined to include any movable property and immovable property, and effectively means all assets in the laws of Hong Kong).