As the energy transition progresses, the importance of green hydrogen is also increasing. It is becoming a key element of decarbonisation. This affects the energy industry, but also the steel, chemical and cement industries as well as heavy goods transport, so-called hard-to-abate sectors in which greenhouse gas emissions are difficult to reduce. But there are also uncertainties: Essential prerequisites for a functioning hydrogen market are still lacking.

Germany currently mainly produces grey hydrogen with high CO2 emissions

Around 60 terawatt hours (TWh) of hydrogen are currently produced in Germany every year. However, only four TWh of this is green hydrogen, which is produced CO2-free using water or chlor-alkali electrolysis. The majority is still grey hydrogen. This is produced by so-called natural gas vapour reforming or is a by-product of chemical processes - and leads to substantial emissions.

Illustration of the international value chain for blue and green hydrogen and ammonia

Producer of hydrogen Eigentümer / Operator of renewable power generation and electrolyser or natural gas reforming plant Standort im Ausland

Transporteur Ausland (netz-/ nicht netzgebunden) Eigentümer / Betreiber der Transportinfrastruktur Leitungsnetz: natürliches Monopol

Transporteur Ausland (netz-/ nicht netzgebunden) Eigentümer / Betreiber der Transportinfrastruktur Leitungsnetz: natürliches Monopol

Produzent von Ammoniak Eigentümer / Betreiber einer Ammoniaksyntheseanlage mit vorgeschalteter Luftzerlegung Standort im Ausland

Betreiber eines Exportterminals Eigentümer / Betreiber von Anlagen zur Verflüssigung von Wasserstoff bzw. Ammoniak und Lagertanks im Hafen Standort im Ausland

Betreiber eines Exportterminals Eigentümer / Betreiber von Anlagen zur Verflüssigung von Wasserstoff bzw. Ammoniak und Lagertanks im Hafen Standort im Ausland

Schifffahrtsgesellschaft Eigentümer / Betreiber von Schiffen zum Transport von Ammoniak bzw. flüssigem Wasserstoff Kann überall angesiedelt sein (Hauptsitz)

Schifffahrtsgesellschaft Eigentümer / Betreiber von Schiffen zum Transport von Ammoniak bzw. flüssigem Wasserstoff Kann überall angesiedelt sein (Hauptsitz)

Betreiber eines Importterminals Betreiber einer Terminalanlage Standort in Nordwesteuropa

Betreiber eines Importterminals Betreiber einer Terminalanlage Standort in Nordwesteuropa

Betreiber von Speicheranlagen Betreiber eines Speichers für gasförmigen oder flüssigen Wasserstoff bzw. Ammoniak Netzgebunden: natürliches Monopol Standort in Nordwesteuropa bzw. in der Nähe des Verbrauchs

Betreiber von Speicheranlagen Betreiber eines Speichers für gasförmigen oder flüssigen Wasserstoff bzw. Ammoniak Netzgebunden: natürliches Monopol Standort in Nordwesteuropa bzw. in der Nähe des Verbrauchs

Betreiber von Speicheranlagen Betreiber eines Speichers für gasförmigen oder flüssigen Wasserstoff bzw. Ammoniak Netzgebunden: natürliches Monopol Standort in Nordwesteuropa bzw. in der Nähe des Verbrauchs

Transportunternehmen (letzte Meile) Eigentümer / Betreiber der Transportinfrastruktur / eines Transportsystems (für Wasserstoff oder Ammoniak) Netzgebunden: natürliches Monopol Nicht netzgebunden: offen für Wettbewerb

Transportunternehmen (letzte Meile) Eigentümer / Betreiber der Transportinfrastruktur / eines Transportsystems (für Wasserstoff oder Ammoniak) Netzgebunden: natürliches Monopol Nicht netzgebunden: offen für Wettbewerb

Transportunternehmen (letzte Meile) Eigentümer / Betreiber der Transportinfrastruktur / eines Transportsystems (für Wasserstoff oder Ammoniak) Netzgebunden: natürliches Monopol Nicht netzgebunden: offen für Wettbewerb

Betreiber Cracker Eigentümer / Betreiber einer Ammoniak-Cracking-Anlage

Betreiber Cracker Eigentümer / Betreiber einer Ammoniak-Cracking-Anlage

Betreiber Verdampfer Eigentümer/Betreiber einer Anlage zur Verdampfung von flüssigem Wasserstoff

Betreiber Verdampfer Eigentümer/Betreiber einer Anlage zur Verdampfung von flüssigem Wasserstoff

Transporteur Inland (netzgebunden) Eigentümer / Betreiber eines Wasserstoffnetzes Natürliches Monopol

Transporteur Inland (netzgebunden) Eigentümer / Betreiber eines Wasserstoffnetzes Natürliches Monopol

NH3-Direktverbraucher Industrie

H2-Nutzer Industrie: Energie oder Grundstoff Mobilität, Strom: Energie

| Producer of hydrogen |

|---|

| Eigentümer / Operator of renewable power generation and electrolyser or natural gas reforming plant |

| Standort im Ausland |

| Transporteur Ausland (netz-/ nicht netzgebunden) |

|---|

| Eigentümer / Betreiber der Transportinfrastruktur |

| Leitungsnetz: natürliches Monopol |

| Transporteur Ausland (netz-/ nicht netzgebunden) |

|---|

| Eigentümer / Betreiber der Transportinfrastruktur |

| Leitungsnetz: natürliches Monopol |

| Produzent von Ammoniak |

|---|

| Eigentümer / Betreiber einer Ammoniaksyntheseanlage mit vorgeschalteter Luftzerlegung |

| Standort im Ausland |

| Betreiber eines Exportterminals |

|---|

| Eigentümer / Betreiber von Anlagen zur Verflüssigung von Wasserstoff bzw. Ammoniak und Lagertanks im Hafen |

| Standort im Ausland |

| Betreiber eines Exportterminals |

|---|

| Eigentümer / Betreiber von Anlagen zur Verflüssigung von Wasserstoff bzw. Ammoniak und Lagertanks im Hafen |

| Standort im Ausland |

| Schifffahrtsgesellschaft |

|---|

| Eigentümer / Betreiber von Schiffen zum Transport von Ammoniak bzw. flüssigem Wasserstoff |

| Kann überall angesiedelt sein (Hauptsitz) |

| Schifffahrtsgesellschaft |

|---|

| Eigentümer / Betreiber von Schiffen zum Transport von Ammoniak bzw. flüssigem Wasserstoff |

| Kann überall angesiedelt sein (Hauptsitz) |

| Betreiber eines Importterminals |

|---|

| Betreiber einer Terminalanlage |

| Standort in Nordwesteuropa |

| Betreiber eines Importterminals |

|---|

| Betreiber einer Terminalanlage |

| Standort in Nordwesteuropa |

| Betreiber von Speicheranlagen |

|---|

| Betreiber eines Speichers für gasförmigen oder flüssigen Wasserstoff bzw. Ammoniak |

| Netzgebunden: natürliches Monopol |

| Standort in Nordwesteuropa bzw. in der Nähe des Verbrauchs |

| Betreiber von Speicheranlagen |

|---|

| Betreiber eines Speichers für gasförmigen oder flüssigen Wasserstoff bzw. Ammoniak |

| Netzgebunden: natürliches Monopol |

| Standort in Nordwesteuropa bzw. in der Nähe des Verbrauchs |

| Betreiber von Speicheranlagen |

|---|

| Betreiber eines Speichers für gasförmigen oder flüssigen Wasserstoff bzw. Ammoniak |

| Netzgebunden: natürliches Monopol |

| Standort in Nordwesteuropa bzw. in der Nähe des Verbrauchs |

| Transportunternehmen (letzte Meile) |

|---|

| Eigentümer / Betreiber der Transportinfrastruktur / eines Transportsystems (für Wasserstoff oder Ammoniak) |

| Netzgebunden: natürliches Monopol |

| Nicht netzgebunden: offen für Wettbewerb |

| Transportunternehmen (letzte Meile) |

|---|

| Eigentümer / Betreiber der Transportinfrastruktur / eines Transportsystems (für Wasserstoff oder Ammoniak) |

| Netzgebunden: natürliches Monopol |

| Nicht netzgebunden: offen für Wettbewerb |

| Transportunternehmen (letzte Meile) |

|---|

| Eigentümer / Betreiber der Transportinfrastruktur / eines Transportsystems (für Wasserstoff oder Ammoniak) |

| Netzgebunden: natürliches Monopol |

| Nicht netzgebunden: offen für Wettbewerb |

| Betreiber Cracker |

|---|

| Eigentümer / Betreiber einer Ammoniak-Cracking-Anlage |

| Betreiber Cracker |

|---|

| Eigentümer / Betreiber einer Ammoniak-Cracking-Anlage |

| Betreiber Verdampfer |

|---|

| Eigentümer/Betreiber einer Anlage zur Verdampfung von flüssigem Wasserstoff |

| Betreiber Verdampfer |

|---|

| Eigentümer/Betreiber einer Anlage zur Verdampfung von flüssigem Wasserstoff |

| Transporteur Inland (netzgebunden) |

|---|

| Eigentümer / Betreiber eines Wasserstoffnetzes |

| Natürliches Monopol |

| Transporteur Inland (netzgebunden) |

|---|

| Eigentümer / Betreiber eines Wasserstoffnetzes |

| Natürliches Monopol |

| NH3-Direktverbraucher |

|---|

| Industrie |

| H2-Nutzer |

|---|

| Industrie: Energie oder Grundstoff |

| Mobilität, Strom: Energie |

Source: Energy systems of the future, 2022

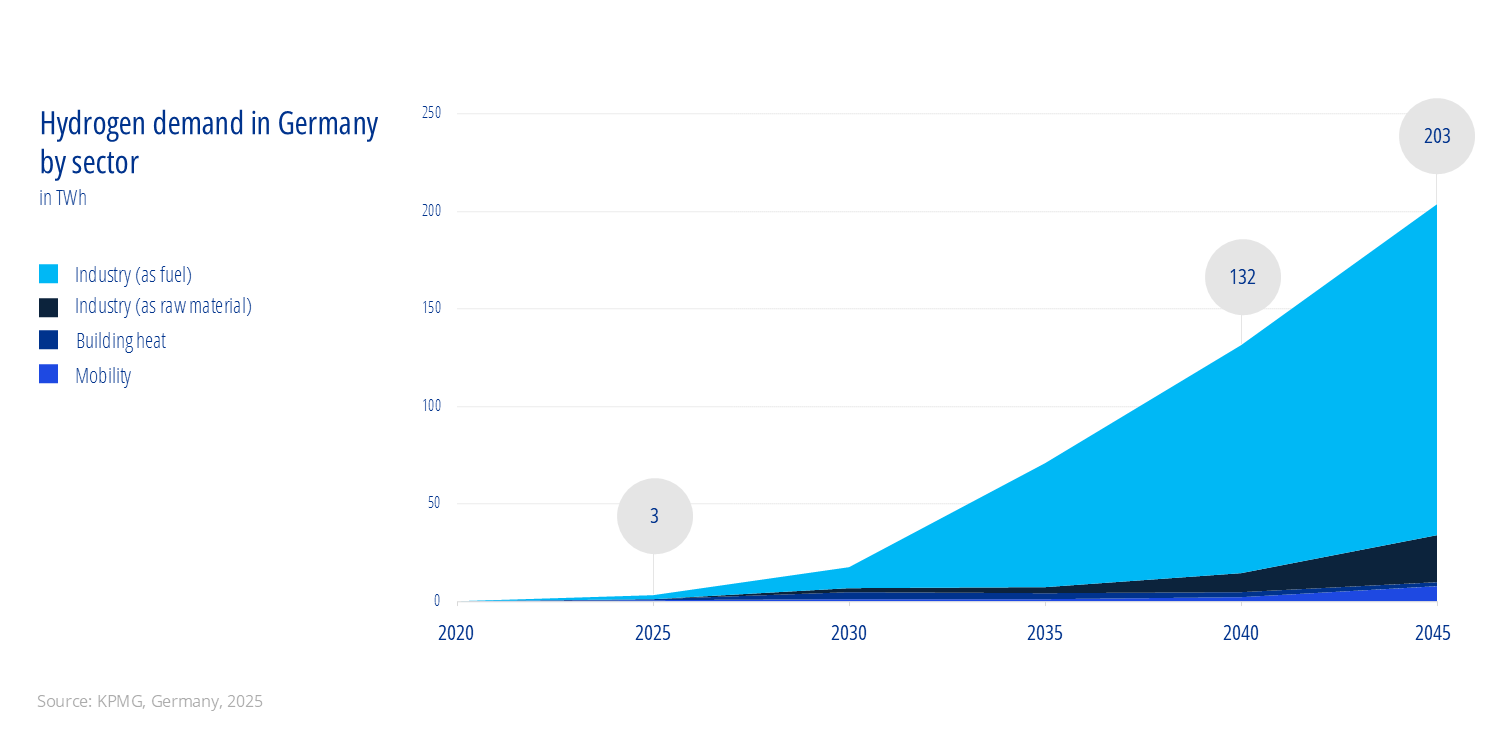

Demand for green hydrogen will increase significantly

We expect the demand for green hydrogen, including the resulting downstream products, to increase moderately until 2030 and dynamically from 2030 to 2050. This means that hydrogen and its derivatives are expected to play a decisive role in the transformation of industry. They will also play a supporting role in the energy sector and mobility.

Germany will not be able to meet this demand despite currently planned production plants with a total output of more than ten gigawatts. Instead, we will be dependent on imports - and these will require functioning global supply chains and international partnerships.

This is why Germany wants to invest more than five billion euros in the import of green hydrogen in the coming years. The first tenders for hydrogen imports by the H2Global Foundation - a funding instrument of the German government - are already underway.

Possible applications: How the individual sectors use green hydrogen

Green hydrogen can be an important lever for decarbonisation. Companies could make a significant contribution to climate protection. Here we have broken down for you what this could look like in the individual sectors.

Green hydrogen can be used for various chemical processes, such as the production of fertilisers, green steel or petroleum products. It can also be used to generate the high temperatures required in industry. One example of this is industrial processes that require large amounts of heat. In many cases, gas is the most sensible option for providing the high temperatures required. By using green hydrogen instead of fossil fuels, companies can reduce their CO2 emissions and thus make an important contribution to climate protection.

Green hydrogen will play a role in the transport sector of the future in various ways. Above all, hydrogen derivatives can be used in aviation and shipping to achieve decarbonisation targets and quotas from RED III. In addition, hydrogen can be used to produce ammonia or synthetic fuels (renewable fuels of non-biological origin, RFNBO), which are then used as fuels for combustion engines designed for this purpose. In some cases, fuel cells could also be used in the transport and traffic sector. These convert hydrogen into electricity, which in turn drives an electric motor. Compared to battery electric vehicles, hydrogen technology offers a more compact drive system, faster refuelling and a greater range. This will also make hydrogen attractive for heavy goods or freight transport in the future.

Hydrogen can also be used to heat buildings. Buildings can benefit from the centralised use of heat from H2-ready gas-fired power plants that are transported through existing local and district heating networks. Existing systems can be used and CO2 emissions can also be reduced on a decentralised basis by adding hydrogen to the natural gas network. Studies have shown that even the addition of 20 per cent hydrogen by volume has no safety-relevant effects - neither on the infrastructure nor on the operation of the gas supply.

Electricity generation from PV and wind energy plants fluctuates considerably in some cases and is intermittent - a challenge for the operation of electricity grids. Here too, hydrogen can provide the necessary flexibility. If there is a surplus of renewable energy, plants do not have to be curtailed; the surplus can be used to provide additional hydrogen through electrolysis, stored temporarily and transported to the customer in existing gas infrastructures.

If required, stored hydrogen can also be converted back into electricity in H2-ready gas-fired power plants. So-called innovation power plants are already increasingly being planned today. These combine renewable energies and hydrogen and are therefore able to cover peak demand. Electrolysis opens up opportunities to provide green base load electricity or flexible peak load. Hydrogen can thus contribute to system stability in the electricity grid.

Challenge: establishing a functioning H2 market

Hydrogen projects can only be realised on the basis of a functioning hydrogen economy - and this is a challenge. While the demand for hydrogen is currently growing, there is also a lack of electrolysis capacities in the long term. A functioning market can only emerge if both supply and demand are established at a stable level. In order to overcome these hurdles, incentives must be put in place, firstly for hydrogen production and secondly for its utilisation.

Do you also want to rely on hydrogen in the future? We accompany you

KPMG supports clients with the challenges of the emerging hydrogen economy. This relates to the areas of strategy, financing, growth or transactions and sustainability. In doing so, we draw on in-depth industry expertise and methodological competence.

This includes, for example, identifying and utilising the best possible funding opportunities for your projects in conjunction with a hydrogen strategy in order to grow organically or inorganically through acquisition in this developing market.

We also support you in decisions to utilise hydrogen and its derivatives in your company with the aim of replacing fossil fuels. We help you to review your sustainability strategy, analyse material flows or initiate new partnerships.

Contact our team to find out how your company can benefit from the rapidly growing market in the future.

We look forward to exchanging ideas with you.

More KPMG Insights

Your contacts

Michael Salcher

Regional Head East, Head of Energy & Natural Resources

KPMG AG Wirtschaftsprüfungsgesellschaft

Robert Schwarz

Senior Manager, Performance & Strategy, Enterprise Performance

KPMG AG Wirtschaftsprüfungsgesellschaft

- 1

- 2

- 3