In our latest UK Economic Outlook, we assess the damage that higher energy prices could wreak on the UK economy and what it means for interest rates and inflation. We also look ahead to how the use of weight loss drugs could transform UK consumer spending in the future.

UK Economic Outlook - March 2026

UK Economic Outlook - March 2026

In our latest UK Economic Outlook we look at the prospects for the UK economy in 2026 and 2027, including our analysis of growth prospects, energy prices, inflation, interest rates, consumer spending, wage growth, investment, the labour market and public finances.

Summary of KPMG’s latest forecasts for the UK

March 2026

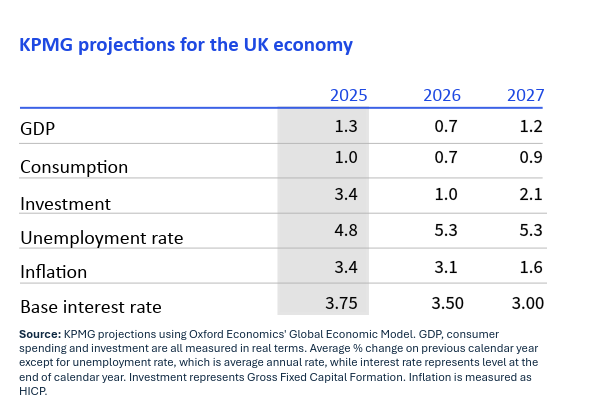

UK economic growth is expected to ease, as GDP is anticipated to grow by 0.7% in 2026. Meanwhile, rising energy prices push up on inflation, limiting Bank of England rate cuts.

Energy shock is set to see inflation rising this year

Headline inflation is expected to rise from the third quarter onwards as the spike in energy prices gradually feeds through. In the near term, inflation may ease slightly, with the Ofgem price cap, which was set ahead of the rise in gas prices, to see household energy bills fall by 7% in the second quarter this year. Last year’s sharp increases in utility prices are also unlikely to be repeated. However, the sharp increase in oil prices will feed through to higher petrol costs for households, potentially leaving inflation at 2.6% by June, above the Bank of England’s 2% target.

Inflation could continue to rise from July onwards as disruptions to oil and gas supplies in the Middle East have put upward pressure on energy prices. The impact of the increase in oil prices has quickly filtered through to higher prices at the pump for motorists, reversing the decline in fuel prices seen over the past year. However, the sharp increase in gas prices pose a larger upside risk for inflation and will likely see household energy bills rise from the third quarter.

If the disruption to energy supplies from the Middle East proves relatively short-lived, and both oil and gas prices decline before the summer, weaker prices could push down on inflation, and see it fall from a peak in September 2026, close to the Bank of England’s 2% target by Q2 in 2027.

Bank of England to keep interest rates on hold as it assesses outfall from the energy shock

With the balance of risks to the inflation outlook tilting firmly to the upside, the Bank of England (BoE) has been prompted into shifting to a more cautious stance. The BoE opted to keep interest rates unchanged in its March meeting, and signalled it is unlikely to cut interest rates in the near term.

A key concern for the BoE is the scale of the second-round effects from higher energy costs, and the possibility that businesses will accelerate price rises as they pass on the costs to customers.

Against this backdrop, the Bank will be hesitant to cut interest rates until it is confident that headline inflation is on a clear downward path. This will mean keeping interest rates higher for longer to ensure that underlying price pressures do not become entrenched over the medium term.

Overall, we believe the BoE will lower interest rates by more than markets currently expect. If the impact of energy supply disruptions fades, a cut later this year appears likely, paving the way for interest rates to fall to 3.5% by the end of 2026.

UK economy has underperformed its peers over the last decade

While the UK economy performed relatively well last year, expanding by 1.3%, UK’s growth trajectory over the past two decades has slowed, particularly in comparison to the US and, to a lesser extent, the Eurozone.

The UK economy has been hit both more frequently and more severely over the past two decades than many of its peers. These shocks range from global events, starting with the Global Financial Crisis and extending through the pandemic and the 2022 energy shock, to UK specific disruptions such as Brexit.

As a result, the gap in living standards between the UK and its peers has grown. In 2007, UK GDP per capita lagged the Eurozone by 3% and the US by 20%. By 2024, the gap with the Eurozone more than doubled to 7% and increased to 30% compared to the US.

Higher energy costs set to see consumer spending and GDP growth slow

The succession of shocks that have dented economic growth in recent years have also impacted households’ ability and willingness to spend, as household spending in the UK grew by just 1.4% since the pandemic, in stark contrast to nearly 20% growth in the US over the same period, and 5% in the Eurozone.

Our outlook for consumer spending in 2026 is relatively weak, with expected growth of just 0.7%, a slowdown from the 1% recorded in 2025. Cost pressures remain prevalent, with further increases set to come in particularly salient categories, such as energy and food. Consumer sentiment also remains weak by historical standards, and that is likely to keep savings rate elevated.

Given this weak backdrop, government spending is expected to be the main driver of growth, with more modest contributions coming from consumer spending and investment. Net trade is likely to remain weak, as recent changes in US tariff policy will, on balance, make UK exporters less competitive in the face of higher trade barriers.

Energy shock is set to see inflation rising this year

Headline inflation is expected to rise from the third quarter onwards as the spike in energy prices gradually feeds through. In the near term, inflation may ease slightly, with the Ofgem price cap, which was set ahead of the rise in gas prices, to see household energy bills fall by 7% in the second quarter this year. Last year’s sharp increases in utility prices are also unlikely to be repeated. However, the sharp increase in oil prices will feed through to higher petrol costs for households, potentially leaving inflation at 2.6% by June, above the Bank of England’s 2% target.

Inflation could continue to rise from July onwards as disruptions to oil and gas supplies in the Middle East have put upward pressure on energy prices. The impact of the increase in oil prices has quickly filtered through to higher prices at the pump for motorists, reversing the decline in fuel prices seen over the past year. However, the sharp increase in gas prices pose a larger upside risk for inflation and will likely see household energy bills rise from the third quarter.

If the disruption to energy supplies from the Middle East proves relatively short-lived, and both oil and gas prices decline before the summer, weaker prices could push down on inflation, and see it fall from a peak in September 2026, close to the Bank of England’s 2% target by Q2 in 2027.

Bank of England to keep interest rates on hold as it assesses outfall from the energy shock

With the balance of risks to the inflation outlook tilting firmly to the upside, the Bank of England (BoE) has been prompted into shifting to a more cautious stance. The BoE opted to keep interest rates unchanged in its March meeting, and signalled it is unlikely to cut interest rates in the near term.

A key concern for the BoE is the scale of the second-round effects from higher energy costs, and the possibility that businesses will accelerate price rises as they pass on the costs to customers.

Against this backdrop, the Bank will be hesitant to cut interest rates until it is confident that headline inflation is on a clear downward path. This will mean keeping interest rates higher for longer to ensure that underlying price pressures do not become entrenched over the medium term.

Overall, we believe the BoE will lower interest rates by more than markets currently expect. If the impact of energy supply disruptions fades, a cut later this year appears likely, paving the way for interest rates to fall to 3.5% by the end of 2026.

UK economy has underperformed its peers over the last decade

While the UK economy performed relatively well last year, expanding by 1.3%, UK’s growth trajectory over the past two decades has slowed, particularly in comparison to the US and, to a lesser extent, the Eurozone.

The UK economy has been hit both more frequently and more severely over the past two decades than many of its peers. These shocks range from global events, starting with the Global Financial Crisis and extending through the pandemic and the 2022 energy shock, to UK specific disruptions such as Brexit.

As a result, the gap in living standards between the UK and its peers has grown. In 2007, UK GDP per capita lagged the Eurozone by 3% and the US by 20%. By 2024, the gap with the Eurozone more than doubled to 7% and increased to 30% compared to the US.

Higher energy costs set to see consumer spending and GDP growth slow

The succession of shocks that have dented economic growth in recent years have also impacted households’ ability and willingness to spend, as household spending in the UK grew by just 1.4% since the pandemic, in stark contrast to nearly 20% growth in the US over the same period, and 5% in the Eurozone.

Our outlook for consumer spending in 2026 is relatively weak, with expected growth of just 0.7%, a slowdown from the 1% recorded in 2025. Cost pressures remain prevalent, with further increases set to come in particularly salient categories, such as energy and food. Consumer sentiment also remains weak by historical standards, and that is likely to keep savings rate elevated.

Given this weak backdrop, government spending is expected to be the main driver of growth, with more modest contributions coming from consumer spending and investment. Net trade is likely to remain weak, as recent changes in US tariff policy will, on balance, make UK exporters less competitive in the face of higher trade barriers.

Outlook for UK government policy: exploring the new government’s priorities for the UK economy

Yael Selfin, Vice Chair and Chief Economist, KPMG in the UK, was joined by David Smith, Economics Editor at the Sunday Times and Chris Hearld, Group Managing Partner, KPMG, to explore how households and businesses could be impacted and the challenge for the new government of delivering growth while managing public finances.