(This article was published on 28 June 2021 and updated on 27 January 2026)

Highlights

What’s the issue?

Climate-related risks, in particular those arising from transitioning to a lower-carbon economy, could significantly impact a company’s business and its strategic plans1. The useful lives and residual values of the company’s assets may change, as well as the depreciation or amortisation methods.

Climate-related risks may have a substantive financial or strategic impact on a company’s business, affecting the useful lives and residual values of its assets. In some cases, useful lives may need to be shortened and depreciation and amortisation accelerated.

Getting into more detail

Useful life of PP&E and intangibles

Factors to consider

An asset’s useful life is defined in terms of its expected utility to the company. It is the period of time over which the company expects to use it, or the number of production (or similar) units that it expects to obtain from it. [IAS 16.6, 38.8]

Because it is an estimate, management is required to review useful life at each annual reporting date as a minimum. [IAS 16.51, 57, 38.104]

Management considers all of the following factors when determining or reviewing the useful life of an item of property, plant and equipment (PP&E):

- expected use of the asset – many companies have an asset management policy that may involve disposing of the asset before the end of its economic life;

- expected wear and tear;

- technical obsolescence arising from changes or improvements in production. Expected future reductions in the selling prices of items produced using an asset could also be an indicator of that asset’s technical obsolescence;

- commercial obsolescence arising from a change in market demand for the product or service output of the asset. Expected future reductions in the selling prices of items produced using an asset could also be an indicator of that asset’s commercial obsolescence; and

- legal or similar limits on the use of the asset. [IAS 16.56–57]

When assessing the useful life of an intangible asset, management considers many internal and external factors similar to those for PP&E. [IAS 38.88, 90]

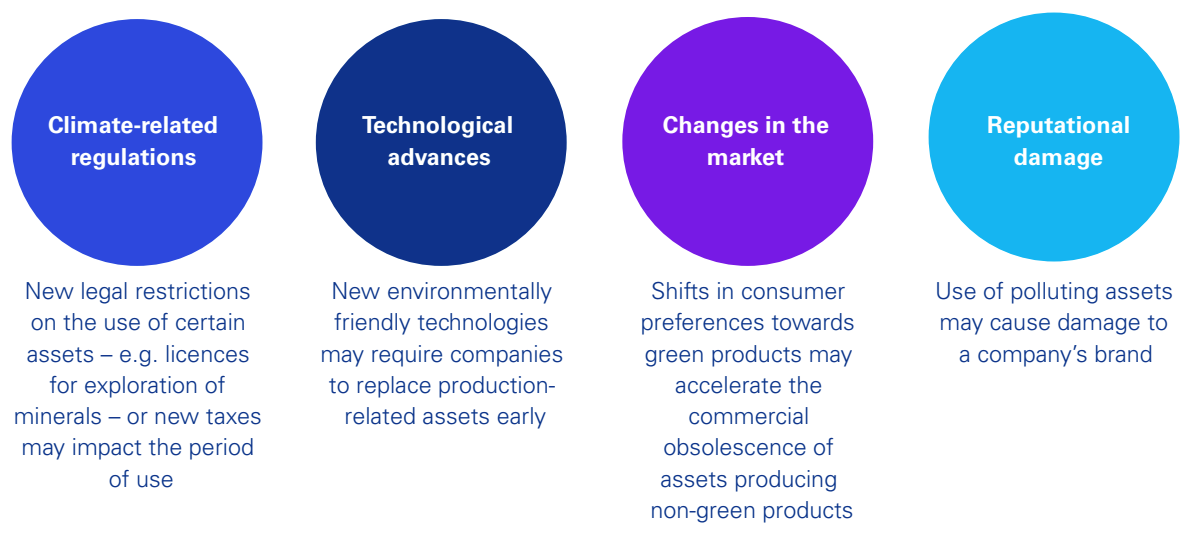

Impact of climate-related risks on these factors

Climate-related risks may impact the estimated useful lives of assets as well as the depreciation or amortisation method. For example, in considering the factors mentioned above, the impacts of transitioning to a lower-carbon economy need to be taken into account, such as the following.

The useful lives of assets will be impacted by the decisions that a company makes in its response to climate-related matters – e.g. management may decide to change the company’s strategy or asset management policies.

For example, a transport company with a fleet of diesel trucks is performing its annual review of the trucks’ useful lives. It considers how its future business may be impacted by climate-related risks and opportunities. There are newly introduced restrictions on the use of diesel vehicles in several large cities in its country of operation. Management expects that many more cities will introduce similar restrictions in the future, which will create significant difficulties for transporting goods using its current fleet. Consequently, it decides to dispose of all of its diesel trucks after three rather than 10 years of service, and revises the useful lives of its diesel trucks accordingly.

Other accounting implications of a decrease in an asset’s useful life

A decrease in the useful life of an asset may also indicate that:

- its carrying amount is impaired. For more information, see our article on the impact of climate change on asset impairment; and

- when applicable, the carrying amount of any related provision for decommissioning that asset could also be affected. For more information, see our article on the impact of climate change on provisions. [IAS 36.12(f)]

Reassessment of indefinite useful life of intangibles

Unlike PP&E, intangible assets can have an indefinite useful life2. Climate-related matters could affect management’s assessment of indefinite useful life – i.e. the useful life of an intangible asset (e.g. a brand) could become finite. [IAS 38.109, Insights 3.3.190.90]

Residual values of PP&E and intangibles

PP&E and intangible assets that have a finite useful life are depreciated to their residual values. ‘Residual value’ is the amount that could currently be received from disposal of the asset, after deducting the estimated costs of disposal, if the asset were already of the age and in the condition that it will be in at the end of its useful life. [IAS 16.6, 38.8]

Similar to useful life, because residual value is an estimate, management is required to review it at each annual reporting date as a minimum. Residual values are typically reviewed in conjunction with the review of useful lives. [IAS 16.51, 38.102]

A change in an asset’s residual value affects its depreciation expense. Continuing the example of the transport company above, management also reviews the residual values of its diesel trucks and finds that the market price for similar used diesel trucks have decreased significantly following the new restrictions. However, because the trucks' mileage in three years' time is expected to be lower under the new policy, the residual values have decreased by only 10 percent. Together, the decrease in the trucks’ estimated useful lives and residual values results in a significant increase in the depreciation expense.

Disclosures in the financial statements

Climate-related matters may significantly affect the useful lives and the residual values of PP&E and intangible assets. If a company re-estimates an asset’s useful life and/or residual value, and the change in the estimate affects the current period or is expected to affect future periods, then it discloses the nature and amount of the change. [IAS 8.39]

In cases of significant exposure to climate-related risks, management’s estimates of useful lives and residual values are likely to be subject to higher estimation uncertainty. If there is a significant risk of a material adjustment to the carrying amounts of PP&E and/or intangible assets within the next financial year, then a company also discloses information about:

- the assumptions that it has used to estimate the useful lives or residual values of those assets (and other major sources of estimation uncertainty at the reporting date); and

- the nature and carrying amount of those assets. [IAS 1.125]

Connectivity

Users need to be able to connect the information in the financial statements – e.g. about the key assumptions and judgements used in preparing the financial statements – with the information a company provides outside the financial statements (e.g. in the front part of the annual report or other general purpose financial reports). For example, they want to understand whether and how a company’s net-zero commitment or plan to transition to a lower-carbon economy affects the company’s assessment of the useful lives and residual values of its tangible and intangible assets.

If differences exist – e.g. the useful lives are unaffected – then disclosing the reasons may be necessary to help users understand and reconcile the information in the front part of the annual report with the financial statements.

Regulatory expectations

Climate-related information is a key area of focus for many regulators. For example, the European regulator ESMA3 has published a report on climate-related disclosures with examples of disclosures of the impact of climate-related matters on the useful lives of tangible and intangible assets together with explanations of why such disclosures may be useful to users of financial statements. ESMA expects companies to consider these examples when assessing and disclosing the degree to which climate-related matters play a role in the preparation of the financial statements.

For more guidance on disclosures and regulatory expectations, see Have you disclosed the impacts of climate-related matters clearly?

Actions for management to take now

Consider whether:

- the impact of climate-related matters is reflected in the useful lives and residual values of the company’s assets;

- the assessment of the indefinite useful life of an intangible asset is appropriate, considering the impact of climate change;

- the estimates of useful lives and residual values in the financial statements are consistent as appropriate with the information provided on climate-related risks and opportunities elsewhere in the annual report;

- you are providing clear and meaningful disclosures, considering also relevant regulatory guidance, about significant judgements and estimates made; and

- the useful life and residual value estimates are consistent, to the extent appropriate, with information related to climate-related matters discussed elsewhere in the annual report. Consider providing additional explanations in the annual report where differences arise.

References to ‘Insights’ mean our publication Insights into IFRS®

1 Read our article to find out more about how climate-related risks and opportunities may impact a company’s strategy, financial reporting and sustainability reporting.

2 An intangible asset has an indefinite useful life when there is no foreseeable limit to the period over which the asset is expected to generate net cash inflows for the company. [IAS 38.88]

3 European Securities and Markets Authority.

© 2026 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.