Highlights

– Who is affected and what will the impact be?

– Recognising regulatory assets and regulatory liabilities

– Effective date and transition

– Next steps – Read our detailed First Impressions publication

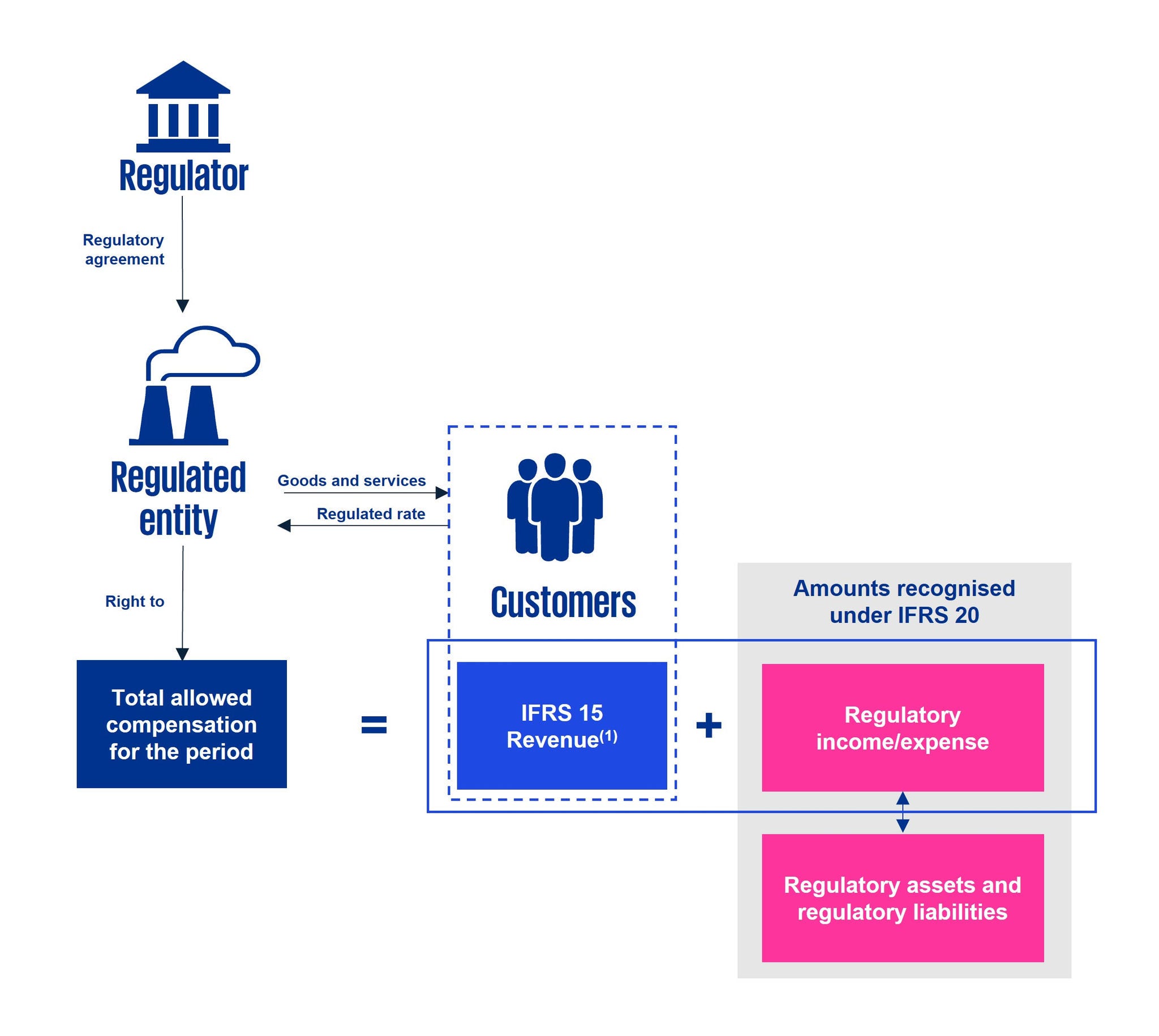

Rate regulation, common in the utility and transport sectors, can have a significant effect on a company’s long-term financial performance. However, until now, IFRS Accounting Standards – unlike some national GAAPs – have not included comprehensive guidance on the accounting impacts of rate regulation.

This gap is now addressed by IFRS 20 Regulatory Assets and Regulatory Liabilities, which replaces IFRS 14 Regulatory Deferral Accounts. IFRS 20 introduces a new accounting model under which a company subject to rate regulation that meets the scope criteria recognises regulatory assets and regulatory liabilities.

The new model aligns the total income recognised in a period under IFRS Accounting Standards with the total allowed compensation the company is entitled to earn for regulatory goods or services supplied in the period. As a result, the model is expected to provide users with more complete financial information about companies subject to rate regulation.

Our First Impressions publication provides detailed insights, using a step-by-step approach and illustrative examples to show how companies might apply IFRS 20.

Who is affected and what will the impact be?

A company applies IFRS 20 if:

- the company and a regulator are parties to an agreement which prescribes the regulated rate the company can charge customers; and

- part or all of the total allowed compensation for regulatory goods or services delivered in one period is charged to customers in a different period – i.e. the agreement creates timing differences.

IFRS 20 is not sector-specific and, unlike IFRS 14, is not optional. Therefore, any company that meets its scope criteria is required to apply it.

What will the impact be?

Companies will recognise new assets and liabilities, as well as new items of income and expense. Although the impact on financial performance will depend on the company’s facts and circumstances, common cases will include the following.

- If recognition of income under IFRS 15 Revenue from Contracts with Customers previously lagged total allowed compensation, then a company will see an increase in net assets on transition to IFRS 20 because it will recognise regulatory assets for those timing differences.

- If a company previously experienced material short-term timing differences between recognition of revenue under IFRS 15 and total allowed compensation for the period – e.g. because of cost or volume variances – then volatility in reported earnings from these differences will be reduced.

Recognising regulatory assets and regulatory liabilities

IFRS 20’s core principle is that a company recognises in its financial statements the total allowed compensation for regulatory goods or services in the same period that the company supplies those goods or services. It does this through an ‘overlay’ approach under which a company first applies the requirements of existing IFRS Accounting Standards (e.g. recognising and measuring revenue in accordance with IFRS 15) and then recognises:

- a regulatory asset: when it has an enforceable present right to add an amount in determining the regulated rate to charge customers in future periods; and

- a regulatory liability: when it has an enforceable present obligation to deduct an amount in determining the regulated rate to charge customers in future periods.

Movements in regulatory assets and regulatory liabilities give rise to regulatory income and regulatory expense.

Companies generally need to measure their regulatory assets and regulatory liabilities using a cash flow measurement technique which:

- estimates expected future cash flows; and

- discounts the cash flows using the regulatory interest rate.

Regulatory income minus regulatory expense is presented separately in the statement of financial performance, immediately below revenue, whereas regulatory assets and regulatory liabilities are presented separately from other assets and liabilities in the statement of financial position.

Effective date and transition

Companies are required to apply IFRS 20 for reporting periods beginning on or after 1 January 2029. Earlier application is permitted, subject to any local endorsement requirements.

A company can choose between applying IFRS 20 retrospectively or using a modified retrospective approach.

IFRS 20 supersedes IFRS 14. Companies that applied IFRS 14 will transition to the new requirements like any other company – there is no option to automatically carry forward existing IFRS 14 accounting.

Next steps

Now is the time to get ready to report using the new standard.

Consider whether you are required to apply IFRS 20 and, if so, assess the implications for your company, including:

- potential regulatory assets or regulatory liabilities to be recognised;

- possible changes to alternative performance measures; and

- the effects on systems, data, processes and controls.

Download our First Impressions publication, which sets out a step-by-step approach to applying the requirements of IFRS 20.

Speak to your local KPMG contact for further guidance.

1 Revenue recognised in accordance with IFRS 15 Revenue from Contracts with Customers.

© 2026 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.