Highlights

Proposals to introduce a new Risk Mitigation Accounting (RMA) model in IFRS 9 Financial Instruments aim to better align the financial statements with risk management activities. The RMA model would allow entities that apply a holistic and dynamic approach in managing their interest rate repricing risk to:

- better reflect dynamic risk management activities that arise from an open portfolio of changing assets and liabilities in the financial statements; and

- reduce operational complexities with the current macro hedge accounting requirements.

This would be a significant change for banks and insurers that manage their exposure to repricing risk that arises from financial assets and financial liabilities that change continually.

The new model1 would be optional. However, entities would no longer be able to hedge account under IAS 39 Financial Instruments: Recognition and Measurement, because these requirements would be withdrawn once the proposals are finalised. Instead, entities could apply the RMA model and/or the general hedge accounting requirements under IFRS 9 or cease hedge accounting altogether.

What's the issue?

Banks and insurers are subject to interest rate risk, specifically repricing risk, as their financial assets and financial liabilities in a portfolio reprice to market interest rates at different times or amounts. For banks, repricing risk causes volatility in their net interest income (NII) and their economic value of equity (EVE).

To manage this risk, banks enter into interest rate derivatives to protect their NII and/or EVE. However, their underlying assets and liabilities are dynamic – i.e. they change as and when banks grant new loans, accept new deposits and borrow funds.

Current hedge accounting models are not designed for risk management strategies for dynamic portfolios of financial assets and financial liabilities. Consequently, many banks face operational complexities when performing either:

- proxy hedging (i.e. designating a derivative against a single asset or liability even though the risk may be managed at a portfolio level); or

- macro hedging (i.e. designating derivatives against a portfolio of prepayable instruments as a fair value hedge). For example, banks need to frequently stop and restart, or rebalance, hedging relationships as the assets and liabilities change in the portfolio.

More importantly, current hedge accounting models limit banks’ ability to reflect how they manage repricing risk in their financial statements and how effective they are at doing so.

What’s proposed

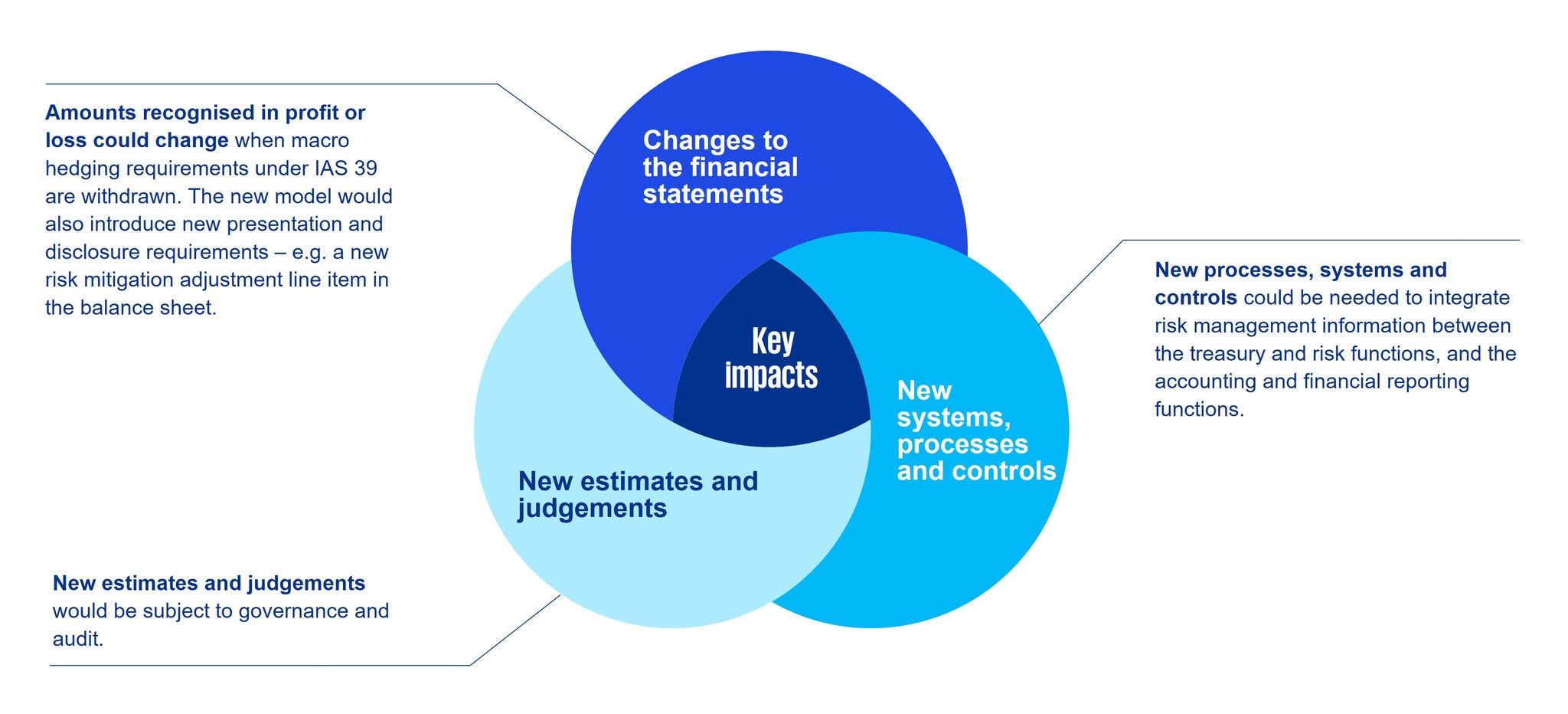

The new model is designed specifically for dynamic portfolios of financial assets and financial liabilities that are managed on a net basis. Under the new model, an entity would recognise the repricing risk successfully mitigated through its risk management activities in a separate ‘risk mitigation adjustment’ line item in the balance sheet. This would provide investors with information on the extent to which the entity is achieving its risk management objectives. Entities would also provide new disclosures, including information on their risk management strategy and how that strategy is used to manage exposure to repricing risk.

What are the potential impacts?

The RMA model could have significant impacts for entities that manage interest rate risk dynamically. Key impacts could include the following.

Next steps – Have your say by 30 November 2026

- Act now to understand the proposals and assess their potential impacts for your portfolio and risk management activities.

- Get involved with field testing the proposals and take this opportunity to respond to the International Accounting Standards Board (IASB) by 30 November 2026. Have a look at the IASB’s Request for Fieldwork that accompanies the proposals.

- Read our detailed guide.

1 Previously known as the Dynamic Risk Management model.

© 2026 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.