Direct ownership or real estate company?

Tax considerations

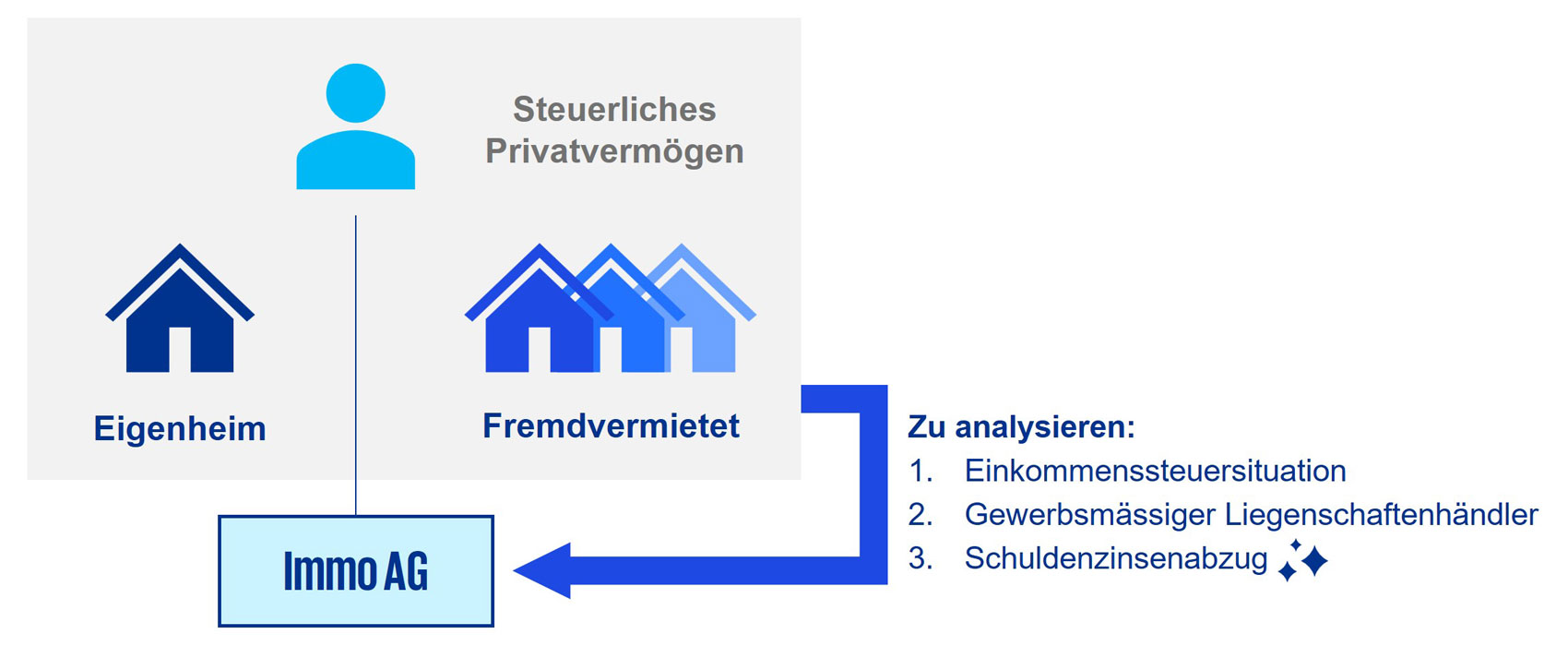

Individuals who own multiple properties have long faced the question of whether to continue holding their real estate directly (in German) or to transfer it into a real estate company. The reasons for doing so are diverse (for example, estate planning).

From a tax perspective, two topics have traditionally been at the core:

- optimizing income tax exposure, and

- avoiding a potential classification as a professional real estate dealer.

Now that the imputed rental value has been eliminated, another tax-driven consideration comes into play that supports transferring properties into a personally held real estate company: to maintain full deductibility of interest expenses.