What is IFRS 18?

IFRS 18 "Presentation and disclosure in Financial Statements" is the new standard that will replace IAS 1 "Presentation of Financial Statements" (IAS 1), marking a major shift in how companies present their financial statements under IFRS Accounting Standards. Designed to improve the clarity and financial statement disclosure, IFRS 18 focuses particularly on income statement classification.

It introduces new requirements that enhance the IFRS 18 disclosure requirements and the structure and clarity of financial reports in accounting, especially the income statement. These changes will allow investors and other stakeholders to more easily analyze and compare accounting financial statements from different companies.

Although IFRS 18 introduces significant updates, many of the core elements of IAS 1 will remain. The new standard will either retain these elements with minor changes or integrate them into other IFRS.

IFRS 18 will become mandatory for annual reporting periods starting on or after 1 January 2027, although companies may opt to implement it earlier than that.

Why is IFRS 18 important for companies?

IFRS 18 affects companies in all industries that prepare their financial statements in accordance with IFRS. This includes listed companies, private enterprises and non-profit organizations.

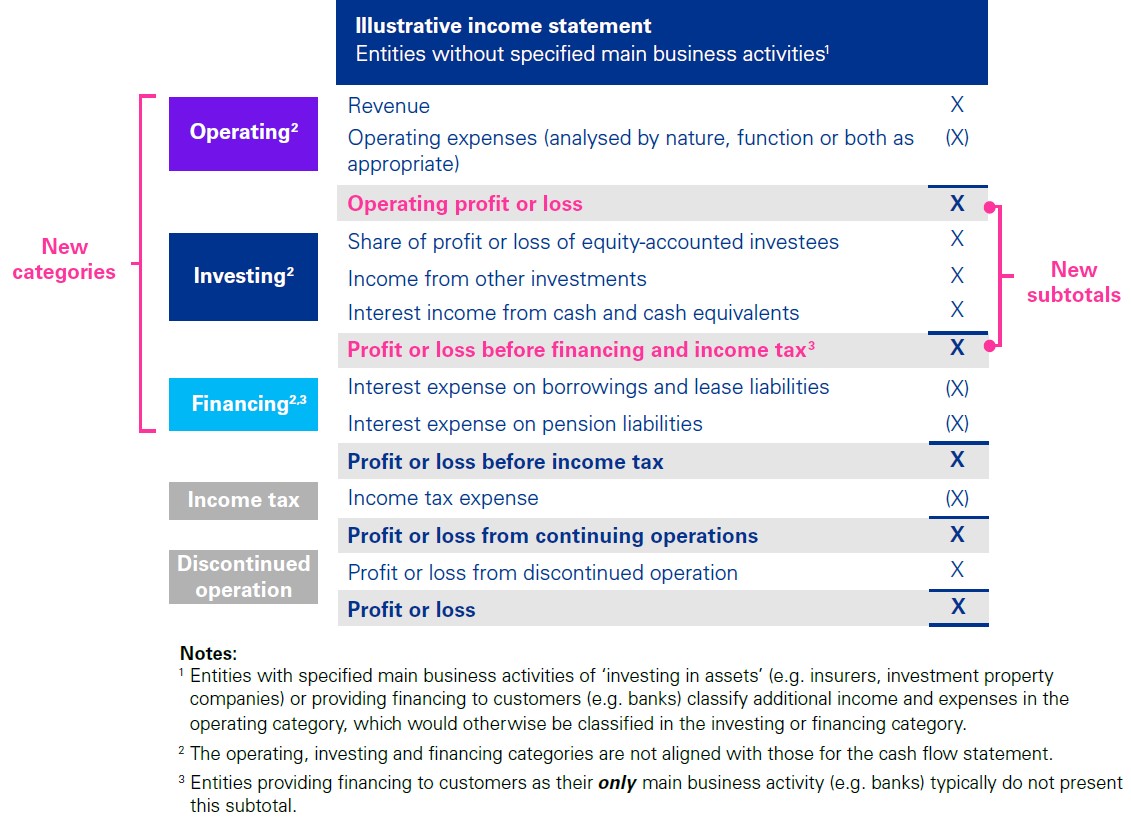

While IFRS 18 does not change how companies recognize or measure assets and liabilities, it will greatly change how they present and disclose financial information. This includes adjustments to the structure of the income statement and cash flow statement, as well as the disclosures provided in the notes.