The latest KPMG study explores this question in depth and also highlights key issues that, in light of the current economic and political climate, should be a focus for boards of directors and executive management.

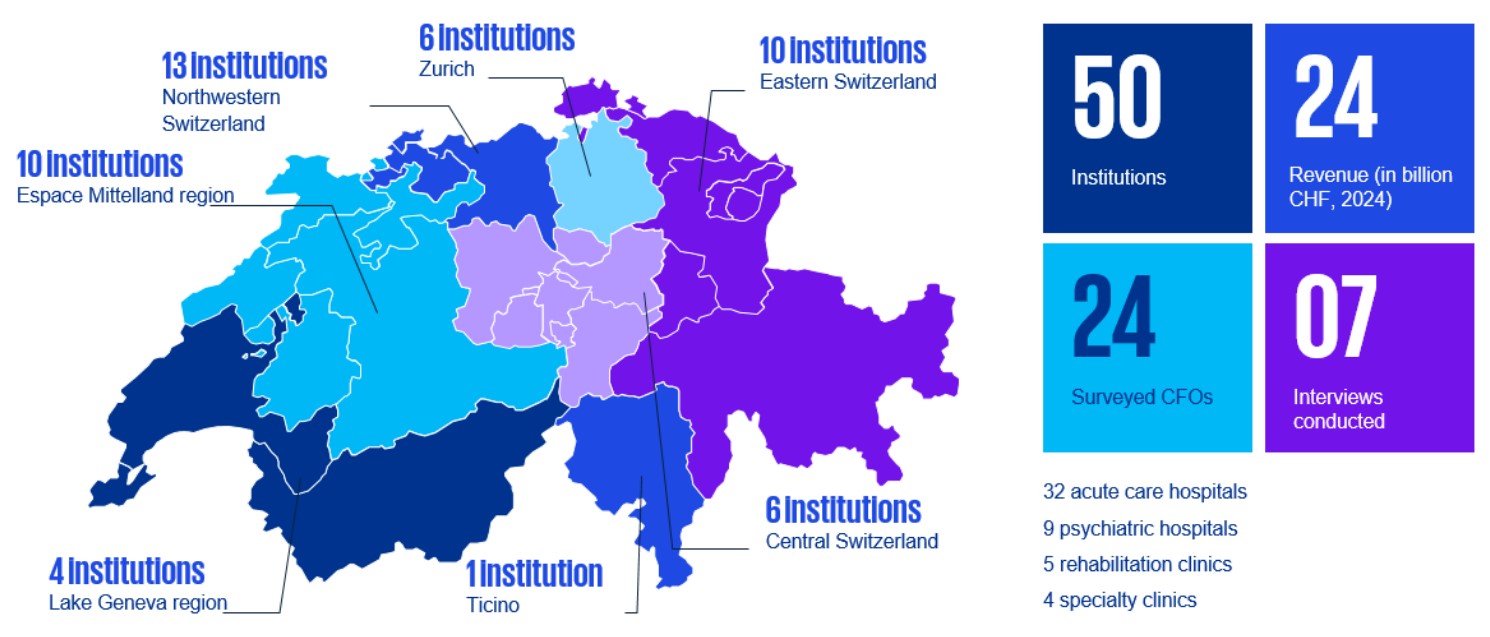

The study is based on an analysis of the annual reports of 50 Swiss hospitals, rehabilitation centers, and psychiatric clinics for the 2024 financial year. This evaluation is complemented by a quantitative survey of CFOs and qualitative interviews with CEOs, providing deeper insights into the industry's expectations for the future.

On this page, you will find a concise overview of the key findings from the study. For in-depth analyses, detailed figures, and further insights, the full PDF document is available for download.