The EU Taxonomy is a classification system that defines which economic activities can be considered environmentally sustainable under EU law. It sets out technical screening criteria across six environmental objectives, under which companies can report that their activities are certified as sustainable if these criteria are met. The Taxonomy aims to create clarity and consistency in sustainability disclosures, preventing greenwashing and helping stakeholders understand the environmental impact of business activities and supporting the EU’s broader climate and sustainability goals.

Reporting under the EU Taxonomy is mandatory for companies subject to the Corporate Sustainability Reporting Directive (CSRD), including large public-interest entities. Over time, the scope of the Taxonomy may expand and cover a broader range of organisations, depending on how the CSRD itself evolves. Recent changes to the CSRD under the Omnibus legislative amendments have reduced the scope of companies who must report under the Taxonomy (read more about the Omnibus changes here). Companies in scope must disclose the proportion of their activities that are Taxonomy-eligible and Taxonomy-aligned, based on the technical criteria set out in the regulation.

The taxonomy is a classification system that defines environmental and sustainable investments. It establishes an EU-wide, mutual understanding of what can be “classified as sustainable.” The taxonomy is an important component in helping investors and companies to direct capital towards solutions that support development and the transition to a climate-neutral and resilient society.

We help organisations interpret and apply the EU Taxonomy to their operations, ensuring accurate and meaningful disclosures, and using it as a framework to improve sustainability offerings. From assessing eligibility and alignment, to integrating reporting into broader sustainability strategies and transforming your business model to increase levels of Taxonomy alignment, our team provides tailored guidance and practical tools to support your compliance and strategic goals.

The EU Taxonomy was developed to address the lack of clarity and consistency in how ‘sustainability’ is actually defined and measured across industries. Without a common framework, investors and stakeholders struggled to assess which activities genuinely contribute to environmental objectives. The Taxonomy fills this gap by providing a science-based, transparent classification system that supports informed decision-making, drawing investor funds to companies that can demonstrate an objectively high degree of sustainable activities in their operations.

It also plays a critical role in combating greenwashing. By setting clear criteria for what qualifies as environmentally sustainable, the Taxonomy ensures that sustainability claims are credible and comparable. This builds trust among stakeholders and strengthens the integrity of the sustainable finance market.

Beyond regulation, the Taxonomy supports the EU’s climate targets and the transition to a net-zero economy. It helps channel investment into activities that make a real contribution to environmental goals, aligning financial flows with the EU Green Deal and broader sustainability ambitions.

How does a company report its activities under the Taxonomy?

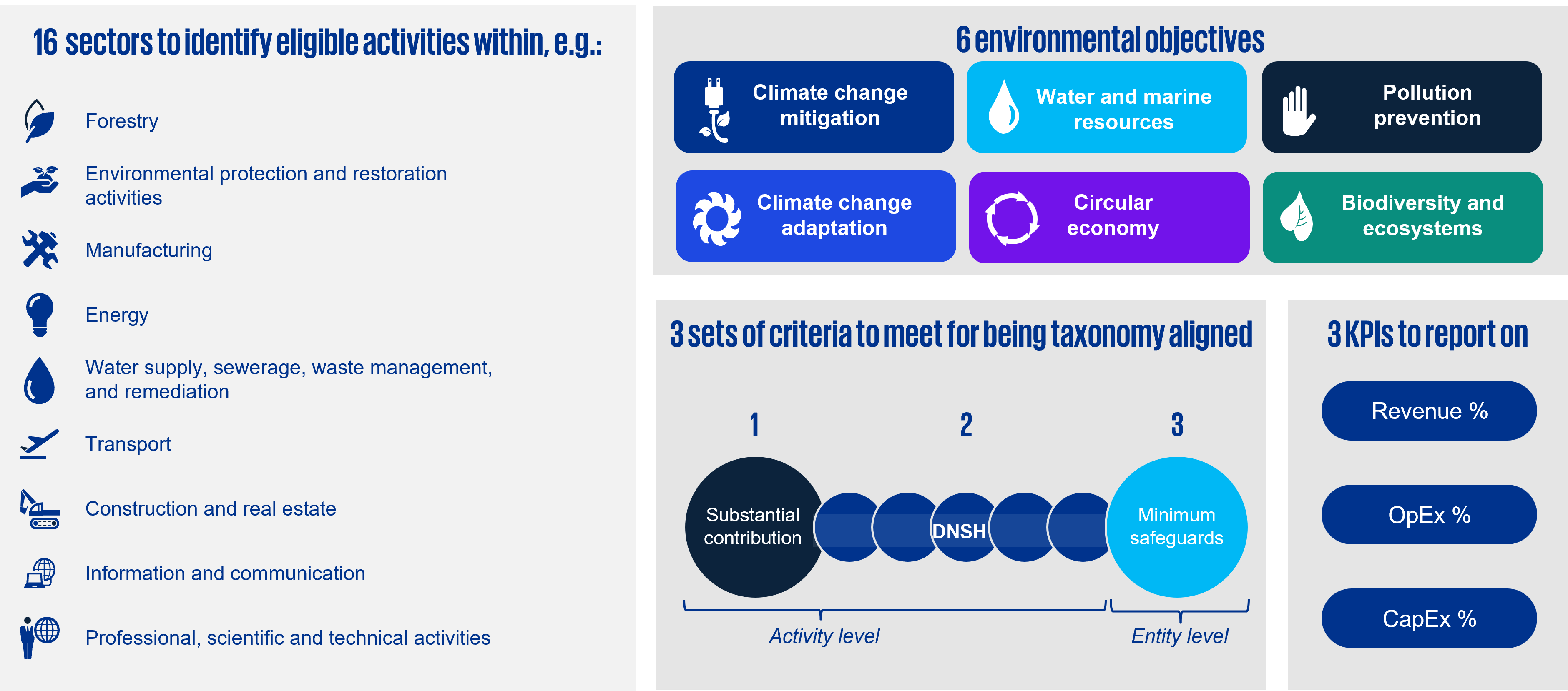

The basic structure of the EU Taxonomy. Source: KPMG.

The basic structure of the EU Taxonomy. Source: KPMG.

Reporting under the EU Taxonomy involves a structured process. First, companies must identify which of their economic activities are covered by the Taxonomy (which will be a list of activities falling under one of the 16 sectors identified in the figure above) — these are considered ‘Taxonomy-eligible’. Next, they assess whether these activities ‘substantially contribute’ to one of the following six environmental objectives by meeting the technical screening criteria (the scientific standards which determine whether the activities are sustainable):

- Climate change mitigation

- Climate change adaptation

- Water and marine resources

- Circular economy

- Pollution prevention

- Biodiversity and ecosystems

The activity must then also ‘do no significant harm’ to the other five environmental objectives by also adhering to certain criteria, and lastly comply with the minimum social safeguards:

- Human rights and labour rights

- Bribery and corruption prevention

- Taxation

- Fair competition

IIf an activity passes all of these tests, it is considered ‘Taxonomy-aligned’ and can be reported in annual reporting.

Companies are required to disclose the proportion of their turnover, capital expenditure (CapEx), and operating expenditure (OpEx) that is Taxonomy-eligible and aligned. These disclosures must be made annually and are subject to assurance under the CSRD. The process requires robust data collection, internal controls, and cross-functional collaboration across finance, sustainability, and various operative teams.

In January 2026, EU institutions formally adopted amendments to the Taxonomy introducing changes to the reporting requirements and thresholds for financial KPIs. The EU Commission is also expected to introduce simplifications to the technical screening criteria, specifically the ‘do no significant harm’ criteria, but it has not yet provided a timeline for doing so.

While the reporting requirements are technical, they also offer strategic value. By understanding how their activities align with the Taxonomy, companies can identify opportunities to improve sustainability performance, attract green investment, and enhance stakeholder trust.

How KPMG can support you with your Taxonomy reporting

KPMG offers end-to-end support to help you navigate the EU Taxonomy and integrate it into your sustainability reporting. Our experts can help you with the following aspects of your Taxonomy journey:

- Identifying Taxonomy-eligible and aligned activities (assessing alignment with technical criteria, whether activities do not significant harm to other environmental objectives and whether they meet minimum social safeguards)

- Developing robust reporting processes that meet regulatory and assurance expectations

- Integrating Taxonomy targets into broader sustainability strategies

- Aligning sustainable financing frameworks and regulations (i.e. Sustainable Finance Disclosure Regulation) with the EU Taxonomy requirements

- Developing processes to track and report investments and sustainability-related KPIs, for example green bond impact reports

- Developing strategies to increase levels of Taxonomy alignment through initiatives such as CapEx Plans (i.e. future investment plans), transition plans, and green financing frameworks

- Implementing data, systems and controls to support ongoing reporting and monitoring practices, ensuring that Taxonomy-related initiatives are tracking to meet reporting ambitions

Beyond compliance, we help you leverage the Taxonomy for strategic advantage. Whether you're seeking to attract sustainable finance, improve ESG ratings, or align with investor expectations, KPMG can support you in turning regulatory requirements into business opportunities. Reporting under the Taxonomy is the perfect exercise to identify areas for your business to become an industry leader in the transition to a sustainable economy, and we can help you identify those opportunities.