The Corporate Sustainability Reporting Directive (CSRD) is an EU regulation that significantly expands the scope and depth of sustainability reporting requirements for companies operating in the EU. It replaces the Non-Financial Reporting Directive (NFRD) and introduces more detailed disclosure standards under the European Sustainability Reporting Standards (ESRS). The CSRD mandates eventual assurance of the reported information, aiming to improve the reliability, comparability, and relevance of sustainability data. Part of CSRD reporting requirements also includes the EU Taxonomy, which you can read more about here.

The Omnibus package (Omnibus I) is an EU legislative proposal designed to refine and streamline the implementation of the CSRD and related sustainability frameworks. Its broad intention is to reduce complexity, improve consistency across EU regulations, and ease the reporting burden for companies. Importantly, the Omnibus also reduced the scope of organisations required to report under the CSRD and simplified the content of the ESRS. Changes to the CSRD have now been agreed by EU institutions, but simplification of the ESRS is still an ongoing process.

Navigating the CSRD requirements can be complex, but our team is here to help. We offer end-to-end tailored support across the suite of steps in the CSRD process: assessing your organisation’s readiness, conducting a double materiality assessment (DMA), performing a gap analysis against your current sustainability practices, interpreting the ESRS and the evolving implications of Omnibus proposals for your company, developing robust reporting strategies, and helping your business implement new practices to reach your desired sustainability ambitions.

The EU has recognised that inconsistent and incomplete sustainability disclosures hinder investors’ and stakeholders’ ability to assess companies’ environmental and social impacts, and how these relate to financial performance. The CSRD and related ESRSs address this by introducing a unified framework that ensures companies report on material sustainability topics in a consistent and comparable way. This shift is not only regulatory—it reflects a broader societal demand for transparency and responsible business practices.

Standardised reporting also supports the EU’s Green Deal and Sustainable Finance agenda, enabling investors to channel capital towards sustainable activities. By aligning sustainability disclosures with financial reporting standards, the CSRD helps integrate ESG considerations into mainstream decision-making. This benefits not only investors but also regulators, civil society, and the companies themselves, as they find a way to adapt their business models and strategies to meet the demands of a sustainable future.

Ultimately, the CSRD aims to create a level playing field across the EU, where sustainability performance is measured and communicated with the same rigour as financial results. This fosters trust, drives accountability, and supports the transition to a more sustainable economy.

What are the key requirements under the CSRD – and how are they evolving?

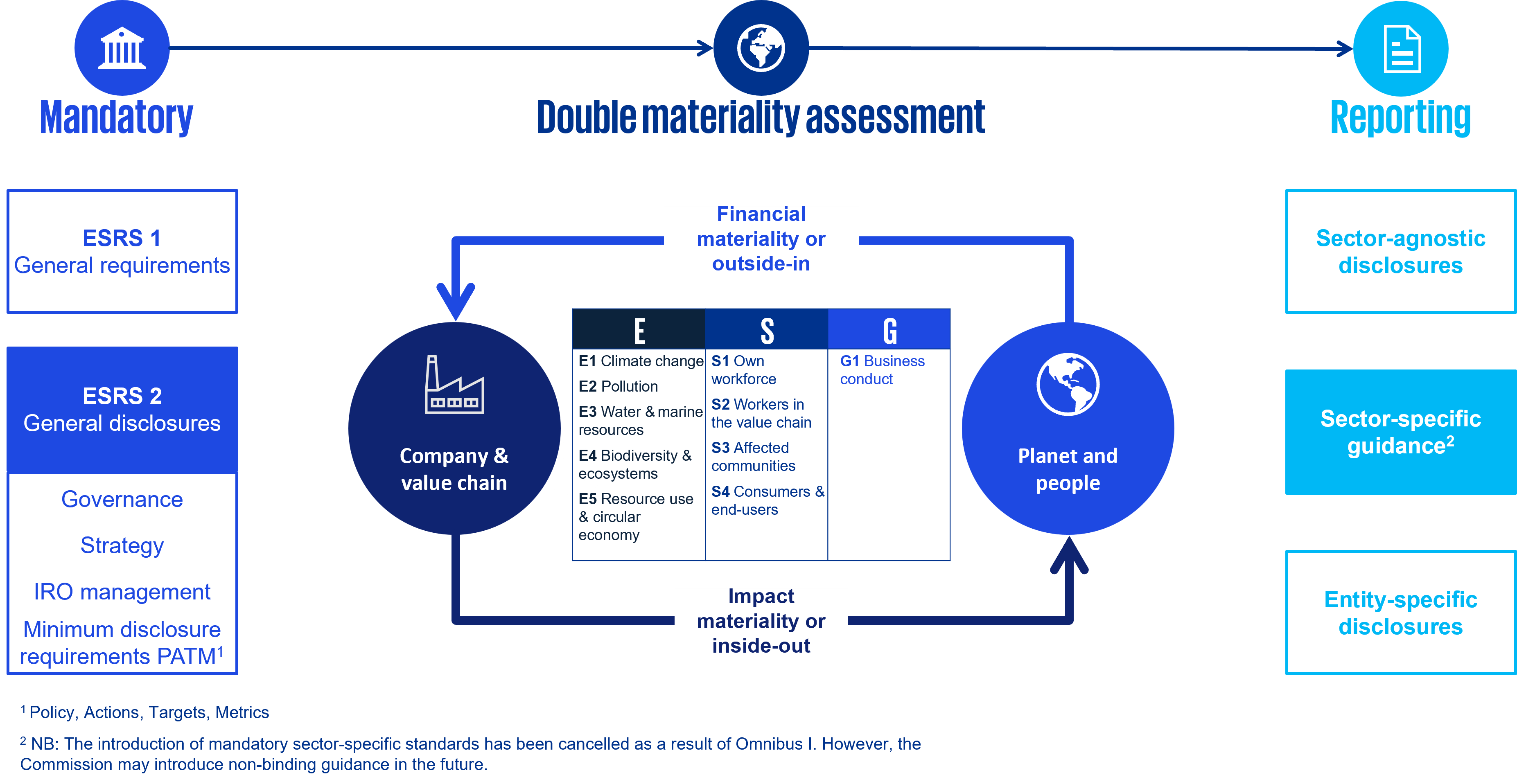

At the heart of the CSRD is the Double Materiality Assessment (DMA), which requires companies to evaluate both how their operations impact people and the environment (impact materiality) and how sustainability issues affect their financial performance (financial materiality).

Performing (and periodically updating) a DMA entails assessing how an organization both impacts, and depends on, a wide range of environmental, social and governance factors. Source. KPMG.

Performing (and periodically updating) a DMA entails assessing how an organization both impacts, and depends on, a wide range of environmental, social and governance factors. Source. KPMG.

This dual lens ensures that reporting reflects the full scope of a company’s sustainability risks and opportunities, and supports more informed decision-making by investors and other stakeholders. The DMA involves rating various pre-defined sustainability topics from a financial and materiality perspective using criteria prescribed in the CSRD. The outcome of the ratings for each topic determines whether that topic is considered ‘material’ for the company and thus whether it must report on that topic from a financial perspective, impact perspective, or both.

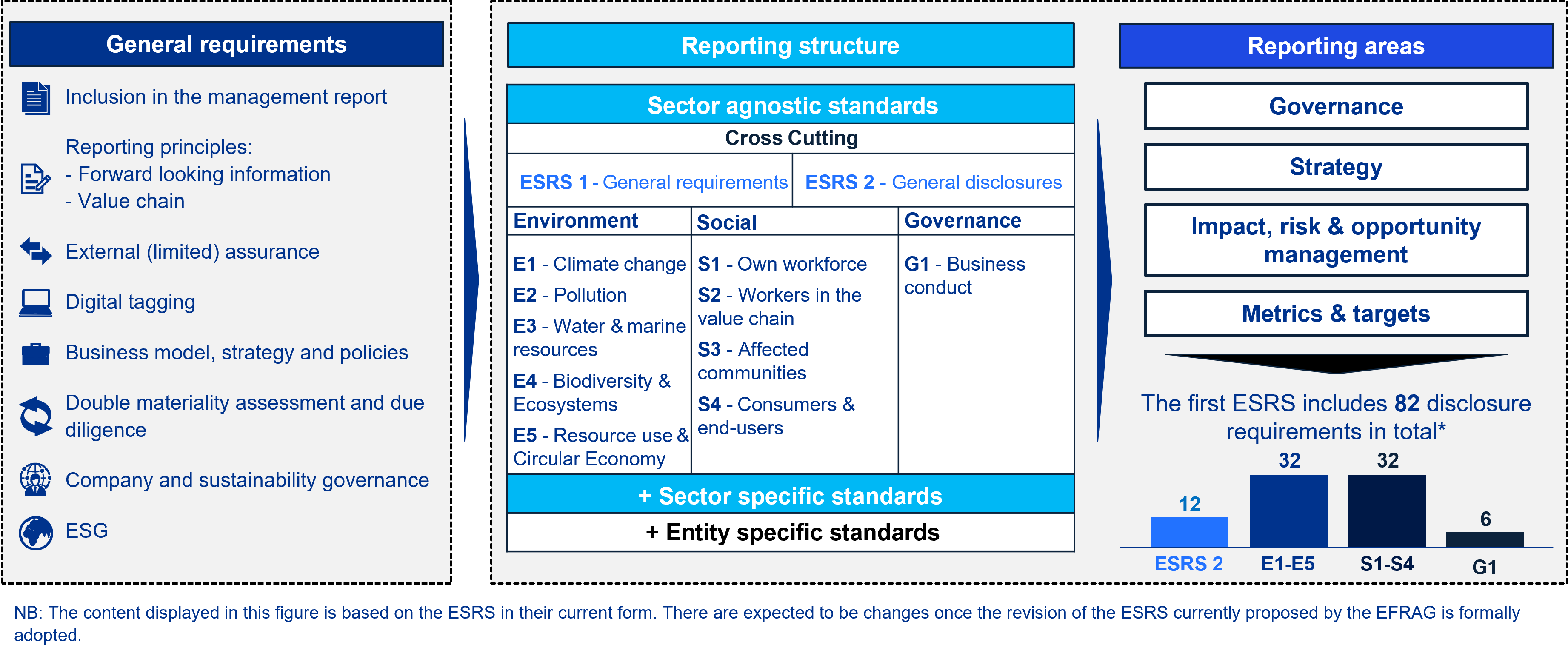

The CSRD is operationalised through the European Sustainability Reporting Standards (ESRS), which provide detailed guidance on what and how to report. The ESRS are structured into cross-cutting standards (covering general principles and disclosures) and topical standards (covering environmental, social, and governance matters). The requirement to introduce sector-specific standards following the agreement of the Omnibus amendments has been removed, however the Commission may still introduce non-binding sector-specific guidance at a later stage (see below for more on Omnibus I).

Under each topical standard, a company must generally report any policies, actions and targets the company has adopted for that material topic, as well as topic-specific disclosures (e.g. a climate transition plan for climate change). The full list of topics under each area, as well as the general and structural requirements of the ESRS, can be seen in the figure below. A voluntary reporting standard for non-listed micro, small and medium enterprises (known as the VSME Standard) has also been introduced for companies out of scope of the CSRD but who still want to demonstrate a commitment to sustainability.

Reporting against the ESRSs encompasses both general requirements and topic-specific disclosures. Source: KPMG.

Reporting against the ESRSs encompasses both general requirements and topic-specific disclosures. Source: KPMG.

Since the introduction of the first Omnibus package in February 2025, which postponed the application of reporting requirements for some companies by two years (large companies that are not public interest entities and have more than 500 employees, large companies with fewer than 500 employees, listed SMEs, small and non-complex credit institutions, captive insurance and reinsurance companies), there were discussions about the further simplification of the CSRD and ESRSs, which were finalised in December 2025. The main simplifications made under the Omnibus amendments include the following:

- A narrowing of the CSRD’s scope—reducing the number of companies required to report by a significant margin (approximately 90%)

- Changes to the structure and content of the ESRS with the intention of shortening and simplifying the standards for ease of understanding, better user friendliness and clarification of areas of confusion (this process is still ongoing)

- Removal of the intention to introduce sector-specific standards (however non-binding guidance may be released at a later stage)

The CSRD is more than just a compliance exercise

While the CSRD introduces mandatory reporting requirements, its impact goes beyond compliance. It encourages companies to embed sustainability into their core strategy, governance, risk management processes and business model. By identifying and disclosing sustainability-related material impacts, risks and opportunities, businesses can make more informed decisions, build long-term resilience, identify new revenue streams, and find ways to adapt their core business offering to incorporate a sustainable contribution to society.

The directive also promotes stakeholder engagement. Transparent reporting enables companies to communicate their sustainability journey to investors, suppliers, customers, employees, affected communities and regulators. This can enhance reputation, attract talent, and strengthen stakeholder relationships.

Moreover, the CSRD can act as a catalyst for innovation and creating new value. As companies assess their sustainability impacts and improve the availability and quality of the related data, they may uncover opportunities to improve operations, develop new products, or enter emerging markets. In this way, the CSRD supports not just compliance, but strategic transformation.

How KPMG can support you with your CSRD reporting

At KPMG, we understand the challenges and opportunities presented by the CSRD. Our multidisciplinary teams combine deep regulatory knowledge with practical experience to help you navigate the complexities of sustainability reporting. We offer a holistic suite of services which can assist you wherever you are on your CSRD journey, such as:

- Roadmap development to ensure your organisation is CSRD-ready

- Performing a DMA, including later revisits as required

- Stakeholder engagement

- Performing gap analyses of current sustainability practices against reporting requirements

- Interpretation of the ESRS

- Assistance with writing your CSRD-aligned sustainability reports

- Implementation of reporting systems and controls, helping you collect, validate, and disclose sustainability data in line with the ESRS

- Ongoing implementation of sustainability practices into broader business strategy to reach your desired sustainability ambitions

- Identifying transformation and value creation opportunities as part of the reporting process

- EU Taxonomy reporting (read more here)

- Independent assurance over sustainability disclosures, helping build trust and credibility with stakeholders

- Readiness assessments and pre-assurance reviews to support internal confidence ahead of formal assurance engagements

The reporting process is a multi-year journey which often involves revisits or revisions of various stages. New and better ways of reporting will be discovered year-on-year, and as a company’s understanding of and appreciation for its sustainability practices and opportunities improves, so does its appetite for revisiting its core strategy, business model and offerings to adapt to a more sustainable future. Whether you're preparing your first CSRD report or you’re well-versed in sustainability reporting, KPMG is your trusted partner at any stage of your sustainability journey.