Corporate Sustainability Reporting Directive, CSRD, replaces the previous directive for sustainability reporting, the Non-Financial Reporting Directive (NFRD). Under the CSRD, which came into effect in the beginning of 2023, more companies will need to prepare comprehensive sustainability reports in accordance with specific standards, called the ESRS. Find out more about the CSRD here.

ESRS is short for the European Sustainability Reporting Standards, which is a new common reporting framework for sustainability disclosures. The new standards mean that dramatically more information related to environmental, social, and governance topics will need to be included in the sustainability report. The objective of the ESRS is to enhance transparency and comparability about how companies impact people and the environment, and about how companies are impacted by environmental issues.

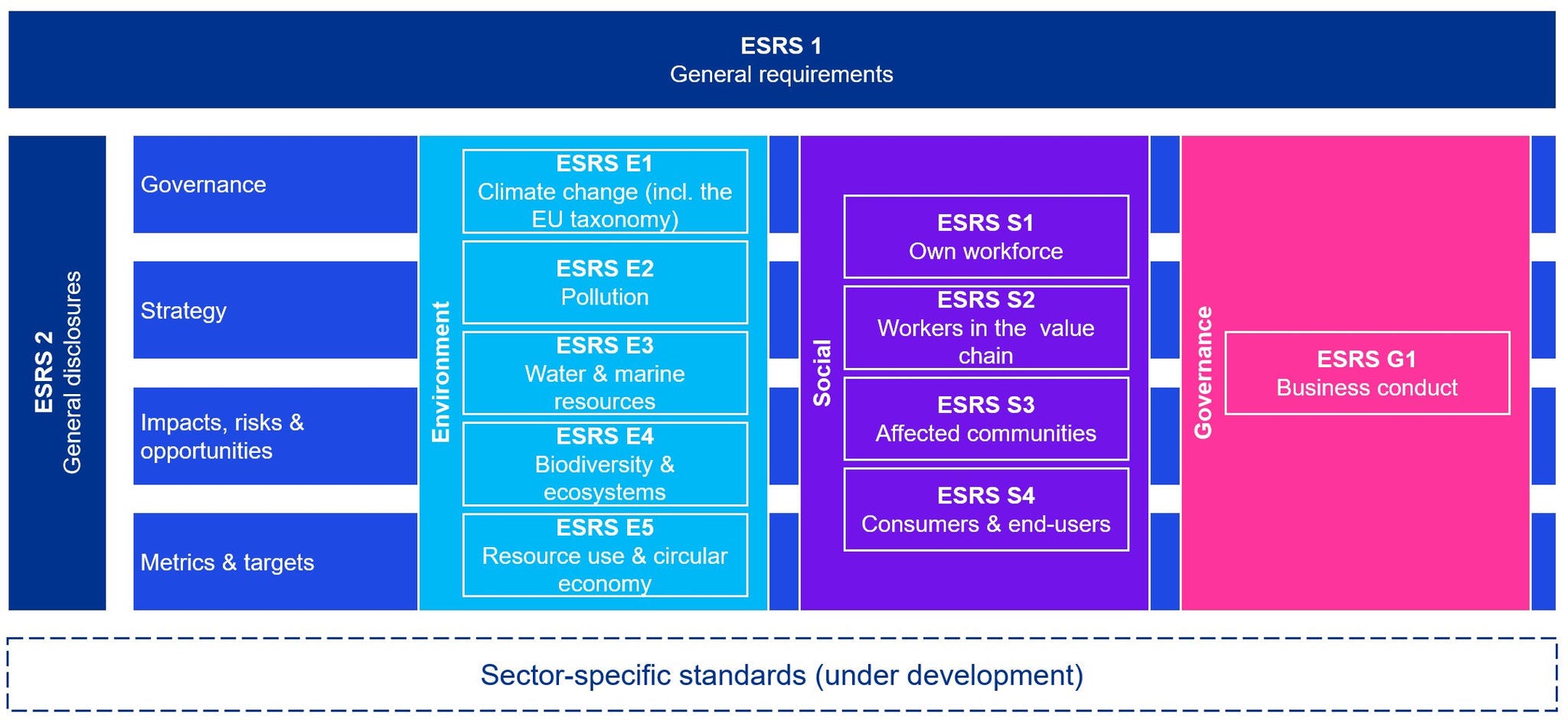

Twelve sector-agnostic standards

EFRAG (the European Financial Reporting Advisory Group) is in charge of drafting the ESRS. So far, twelve sector-agnostic standards have been adopted. Two of these are overarching standards and ten of them are thematic standards. The ESRS lays down details regarding the requirements within CSRD and encompasses:

- Reporting on key concepts such as: double materiality analysis (impact materiality and financial materiality), topic-specific information based on relevant ESG issues for the company, including ESG disclosures for strategy, targets, and progress, as well as the EU taxonomy.

- Inclusion of the sustainability report in the statutory management report, the digital reporting of the report, and that the report must be audited by an accredited third party.

The thematic standards are divided into three overarching categories:

- Environmental topics: Climate change, pollution, water and marine resources, biodiversity and ecosystems, and circular economy.

- Social topics: own workforce, workers in the value chain, affected communities, and consumers and end-users.

- Corporate governance: responsible business conduct

The diagram illustrates the 12 current standards (labelled as ESRS) and the common areas of reporting.

The diagram illustrates the 12 current standards (labelled as ESRS) and the common areas of reporting.

In addition to this, sector-specific standards, standards for listed small and medium companies, voluntary standards for non-listed small and medium companies, and standards for non-EU companies will also be developed and adopted. Currently, simplified standards for listed small and medium companies, and voluntary standards for non-listed small and medium companies are available in draft form.

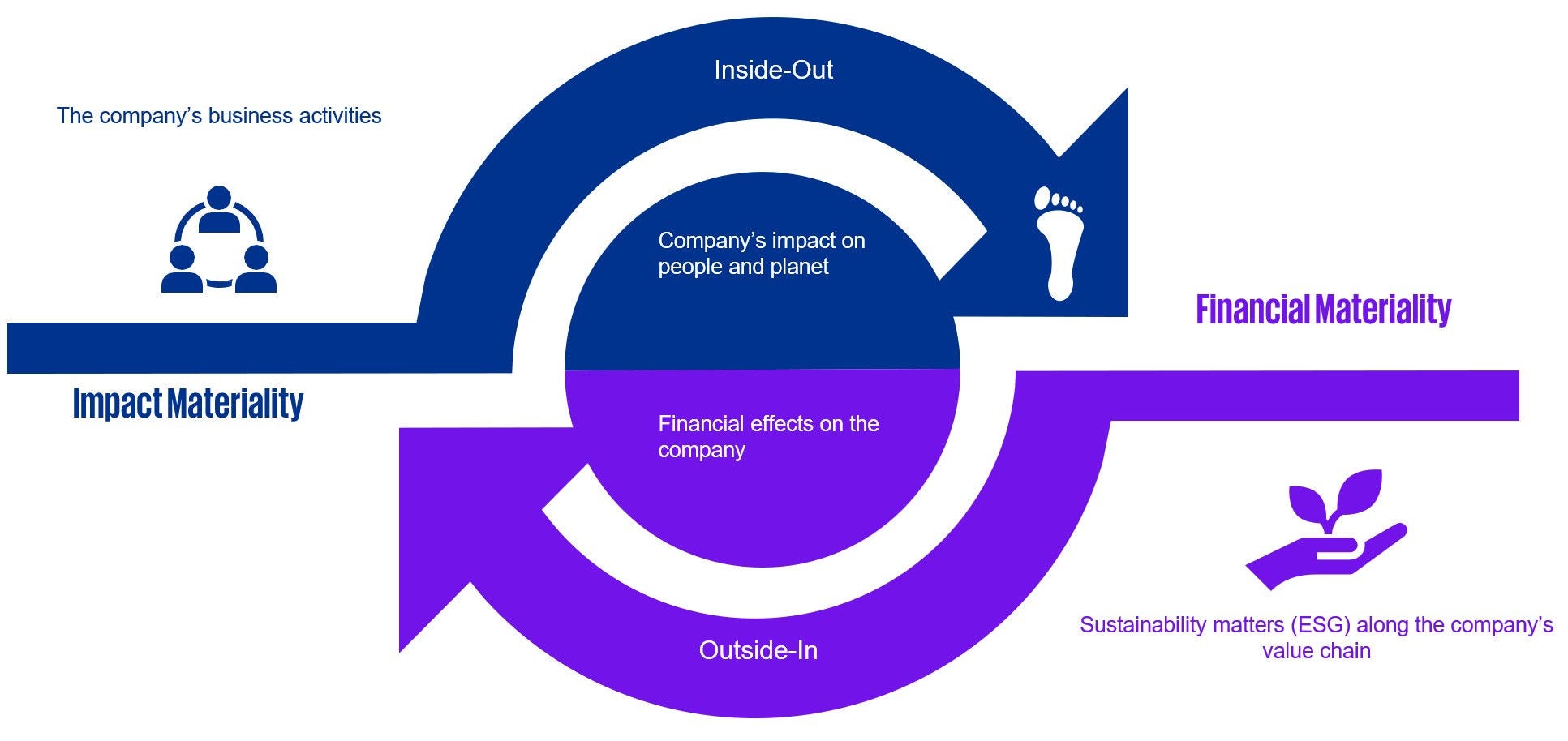

Double materiality analysis

In order to define the extent of a company’s reporting requirements, the ESRS stipulates that a Double Materiality Analysis (DMA) must be conducted encompassing the company’s value chain. A DMA is composed of two sections: the assessment of impact materiality (the company's impact on people and the environment) through which the company must identify material impacts; and the assessment of financial materiality (sustainability topics that may have a financial effect on the company) through which material risks and opportunities are to be identified. For those sustainability topics that are material, the company must report on four areas: governance, strategy, impacts, risk and opportunities, and measurements and targets. If a material impact, risk or opportunity is identified that is not covered by the ESRS, further topic-specific disclosures must be reported. The new reporting standards mean that substantial effort and cooperation will be required between the stakeholders of the entire company.

Double materiality analysis

Double materiality analysis

When do companies have to start reporting in accordance with the ESRS?

CSRD is already in force and the member states are now in the process of integrating it into their respective national legislation. While many of the companies affected by the CSRD already report on sustainability under the Swedish Annual Accounts Act, the CSRD and the detailed disclosure requirements of the ESRS will mean they need to substantially expand the scope of this reporting.

CSRD is planned for phased implementation based on company size, from financial year 2024. In Sweden, the first phase will encompass companies whose financial year starts on or after July 1. It is therefore important to prepare and educate your organization already now in what the new directive will entail.

- In 2025, EU PIEs with more than 500 employees (companies currently subject to the NFRD) will need to report on the 2024 financial year (in Sweden this applies to the financial year starting July 1, 2024).

- In 2026, large companies that fulfil two of the following three criteria will need to report on financial year 2025: more than 250 employees, EUR 40m in turnover, EUR 20m in assets (in Sweden the requirement is as follows: more than 250 employees, SEK 550m in turnover, SEK 280m in assets).

- In 2027 listed small and medium companies (not micro-enterprises), small and non-complex credit institutions, and captive insurance companies will need to report on the 2026 financial year (exemptions possible until 2028).

- In 2029, non-EU companies with a net turnover of more than EUR 150 million in the EU, and with at least one subsidiary or branch in the EU that exceeds certain threshold values, must report on the 2028 financial year.

ESRS implementation check list

How we can support you

Regardless of where your company is in the process, we can help you with preparing for and the implementation of CSRD.

Some of the areas we can assist you with include:

- Conducting a double materiality analysis (DMA) in accordance with the ESRS requirements, to define your organization's reporting needs.

- Conducting a gap analysis compared to the ESRS requirements, encompassing current reporting, availability of data and systems mapping.

- Developing strategies and priorities to close the gaps identified.

- Supporting you to close the gaps identified, for example through data gathering, and developing policies, actions and targets.

- Supporting with the EU taxonomy find out more here.

Connect with our experts

Christopher Larsson

Sustainability Advisor & Auditor, Assurance & Sustainability Services

KPMG in Sweden