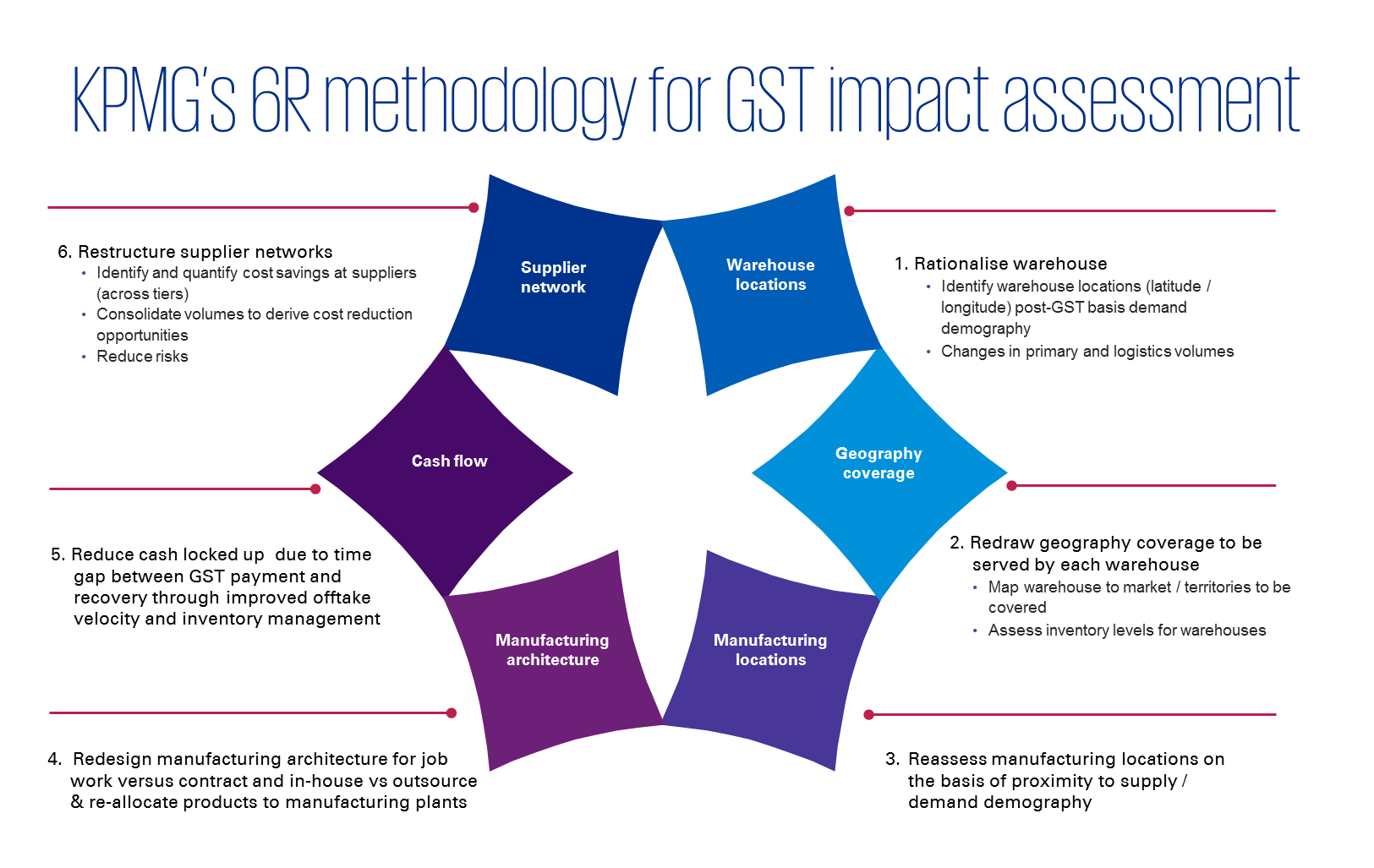

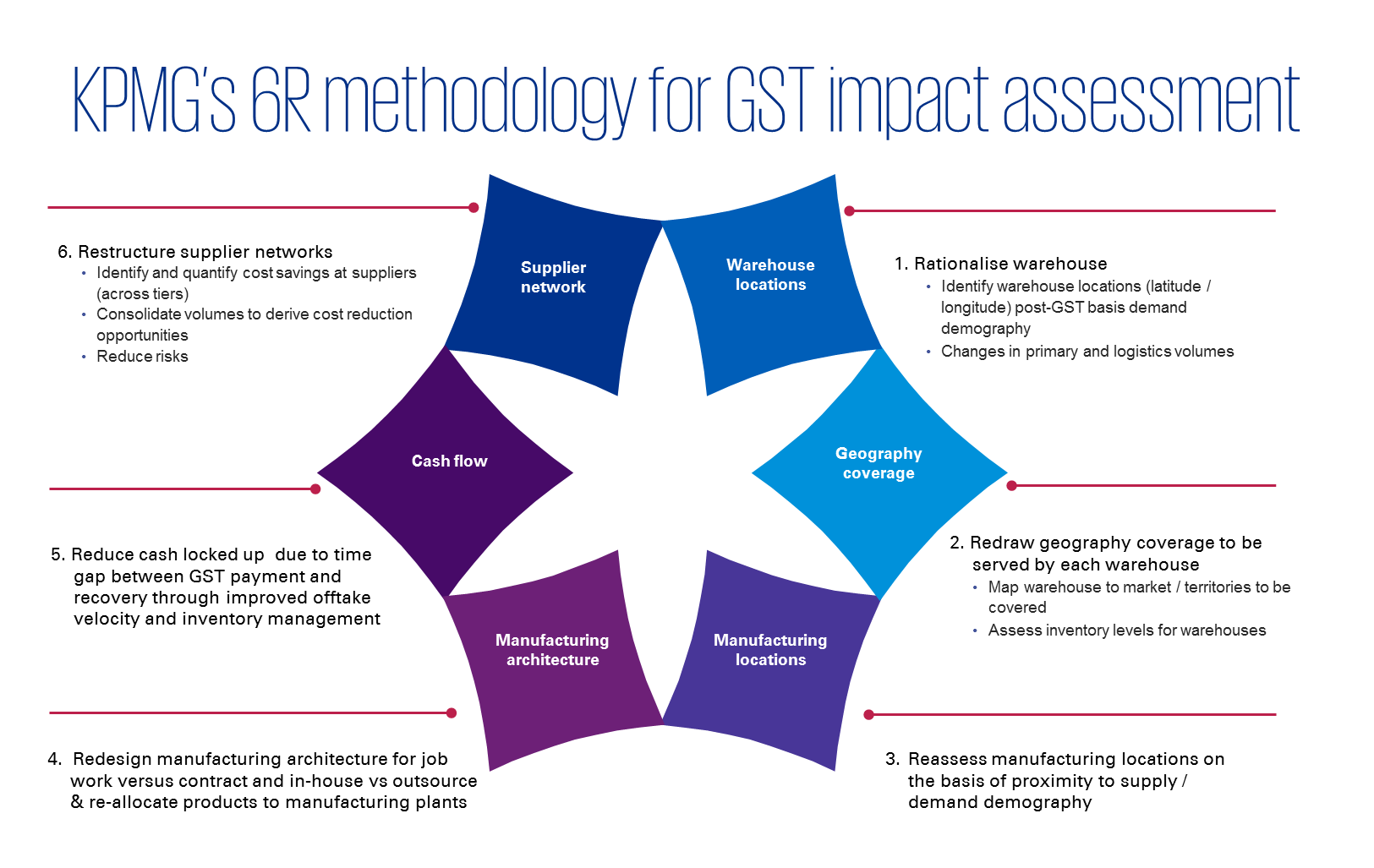

- Supply chain costs consist of fiscal costs (central and state taxes) and physical supply chain costs (transportation, warehousing costs, inventory, etc.). Traditionally, the fiscal costs have predominantly determined the supply chain configuration. Hence, organisations tend to have a supply chain structure that is more distributed and fragmented – a warehouse in each state, suppliers in same state as the manufacturing plant, multiple but smaller manufacturing facilities. However, this is expected to change under GST as locations will become tax neutral.

- Under GST, largely the supply chain costs and efficiencies are set to drive companies’ supply chain configuration.

- Existing supply chains may no longer be efficient or optimal post GST and therefore they can adversely impact cash flows and operation costs if not addressed.

To view Infographics

{kind=link}

{kind=link}

{kind=link}

{kind=link}