The finance minister introduced the Income-tax Bill, 2025 (the Bill), in Parliament. Once enacted, it will replace the current Income-tax Act, 1961 (the 1961 Act), which has been in existence for over six decades. The Bill is slated to become effective on 1 April 2026.

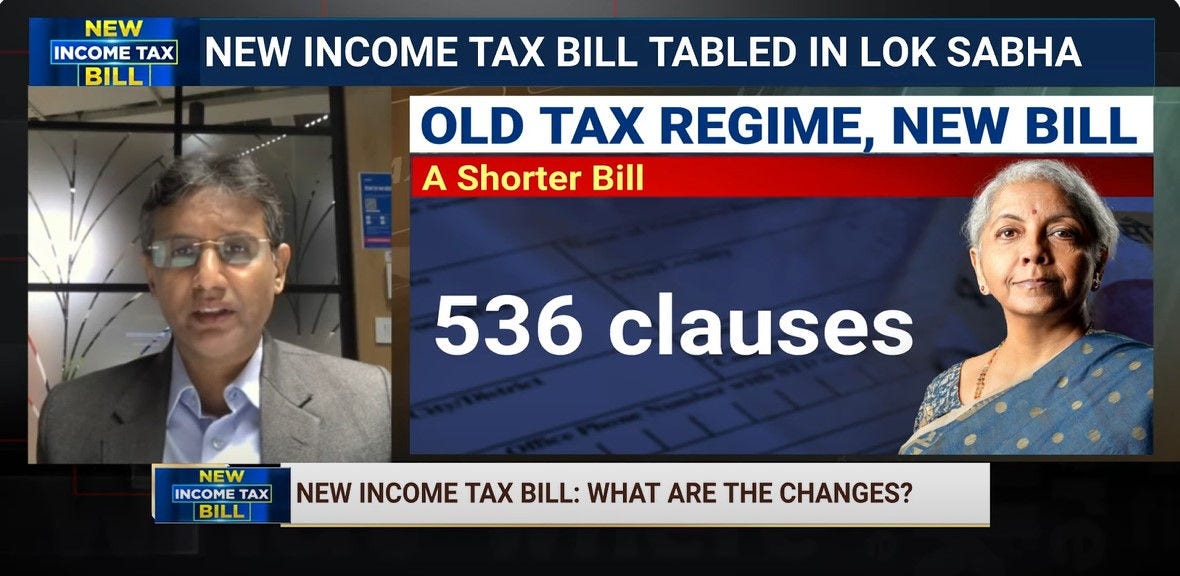

The Bill largely aligns with the existing provisions of the 1961 Act and seeks to simplify the legislation by consolidating similar provisions, eliminating obsolete sections, and presenting some information in a tabular format.

The Bill has removed the concept of assessment year and has reclassified previous year as a tax year. Further, the "explanations" and "provisions" in the 1961 Act have now been introduced as sub-sections.

With massive reduction in sections and chapters, the Bill aims to simplify the legislation, making it concise.